BlackRock TCP Capital: Non-Accruals Down, Losses Up

How a BDC ran out of accounting offsets (and NAV fell 19% in a single quarter)

On November 6, 2025, BlackRock TCP Capital Corp. put out its third-quarter earnings press release. The headline: "non-accruals declined to 3.5% of the portfolio's fair market value, down from a peak of 5.6% in Q4 2024."

CEO Phil Tseng called it "continued progress in repositioning our portfolio."

Seven weeks later, the floor fell out. TCPC’s Net Asset Value (NAV) per share went down from $8.71 to $7.07 (an 18.8% decline in a single quarter).

How does a fund destroy nearly a fifth of its book value in ninety days?

The answer is buried in the Schedule of Investments and the accounting mechanics that govern how BDC loan losses actually flow through the books (I hate GAAP accounting with a passion, but what’s a gal to do?)

Today’s story started in 2022, and worked its way through the books for a few years, before running out of road in Q4 2025. Let’s get into it.

(I’ll include a prompt at the end you can use in your own LLM to pull this data from any BDC’s quarterly filings)

👉 I want two things from you: 1. subscribe, - but even more importantly, 2. start reading the footnotes.

The Metric and Its Blind Spots

Non-accrual percentage is the standard BDC credit quality indicator. When a loan stops paying interest, it goes on non-accrual. The percentage tells you what share of the portfolio’s stated value sits in distressed loans. Lower is better.

Here’s the problem with that metric: it’s denominated in fair value (which management marks). As impaired loans (numerator above) get written down toward zero, their weight in the percentage shrinks.

A loan marked at $128K contributes almost nothing to a $1.7B portfolio’s non-accrual percentage, even if $10.6M of original cost basis remains on the books (this, folks, is why you want to compare non-accruals on cost basis, which, for the record, TCP provided along with the FMV).

The metric (as measured by FV) gets better as the damage accumulates and loans get written down further.

Don’t sleep through the next bit, it’s important!

The mechanics work like this:

1️⃣ When a loan goes on non-accrual, the cost basis generally doesn't change (though it can decrease if the borrower is still making payments, or any deferred income like origination discounts gets applied). The Board marks fair value down, and NAV takes the hit from unrealized depreciation.

2️⃣ Cost resets when a restructuring or formal write-off occurs. At that point, the realized loss is recognized on the income statement. But there is no new impact to NAV, because fair value already reflected the loss (in step 1 above).

The unrealized depreciation simply converts into a realized loss, which is why it shows up as simultaneous unrealized gains and realized losses in the same quarter.

Hold this two-step process in your head, we’ll come back to it shortly.

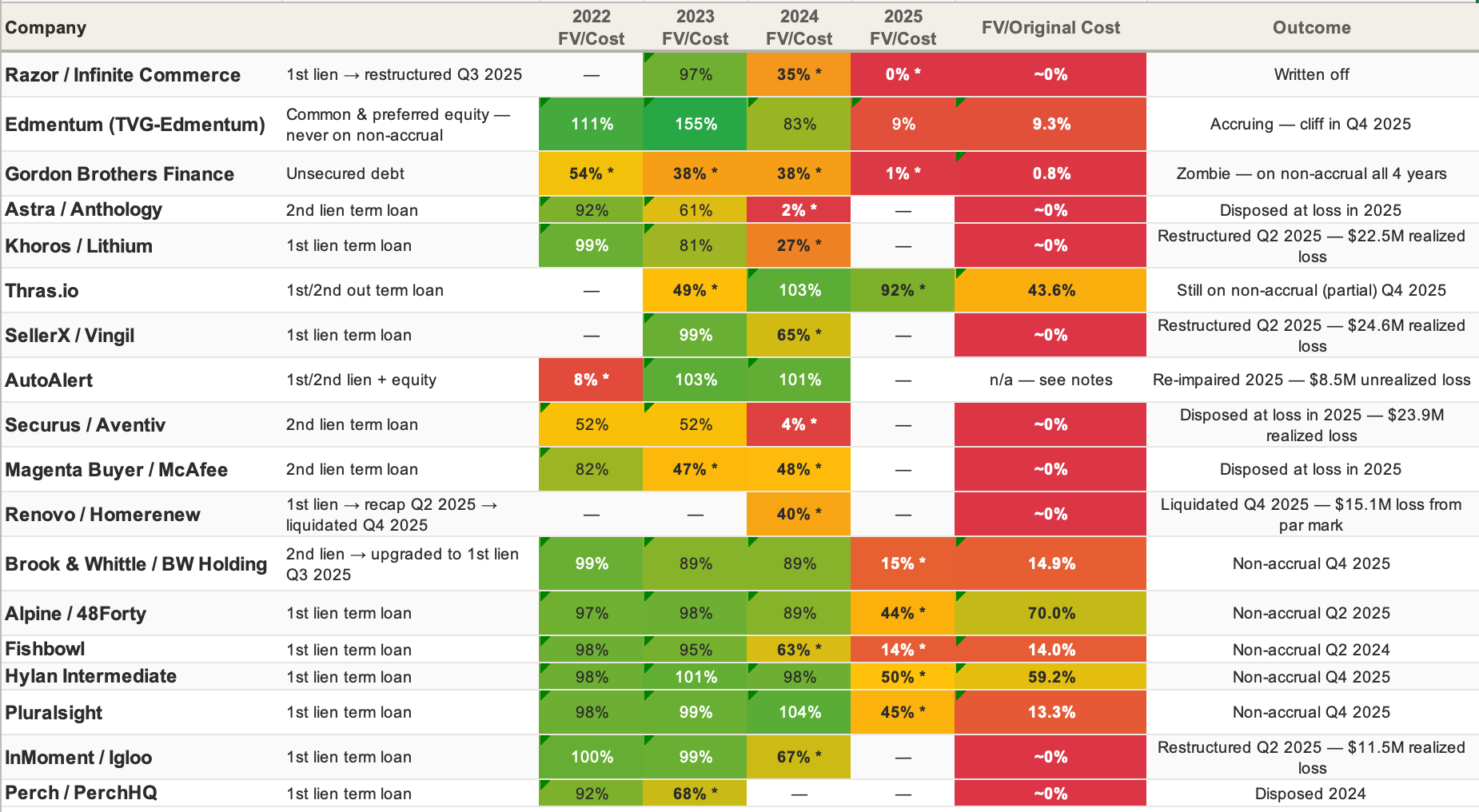

A Story Three Years in the Making

The loans that drove Q4’s collapse had been deteriorating since 2022 and 2023, through multiple markdowns and restructurings.

Management’s own Q4 earnings commentary acknowledged that ~91% of the quarter’s NAV reduction stemmed from investments underwritten in 2021 or earlier.

TCPC’s non-accrual picture during Q4 2024 through Q4 2025 looked like this: