Blue Owl's OCIC vs Oaktree Strategic Credit Fund: A Tale of Two Redemption Queues

A look at portfolio composition, leverage, and income quality

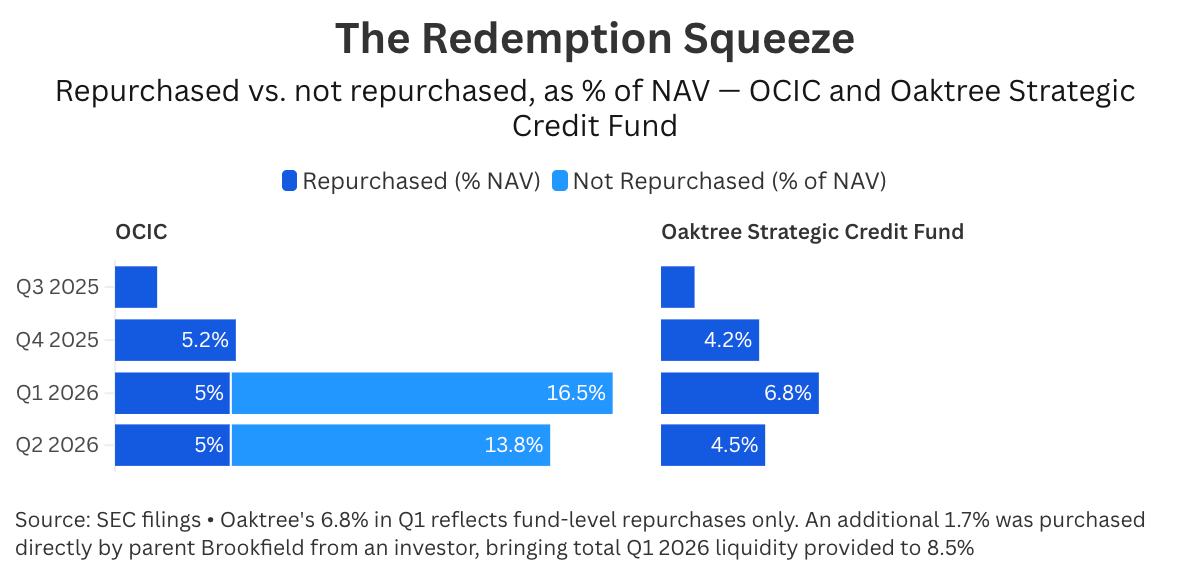

Two private credit funds. On first look, similar portfolios. One had a modest increase in redemption requests (and met them all). The other saw nearly one-fifth of the fund ask for the exits, and had to cap redemptions at 5% of NAV.

So what happened?

Let’s pop the hood and see if we can reverse-engineer the answer.

Here’s what we’ll cover today:

Compare the portfolios

Compare the balance sheets

Compare income quality

Here’s another Blue Owl fund:

Disclosure: This case study is provided for educational and informational purposes only and should not be construed as investment, legal, tax, or financial advice. The views expressed are solely those of the author. All examples are illustrative in nature and not guarantees of future outcomes. Readers should conduct their own independent research and consult with qualified professionals before making any investment or financial decisions.

It’s probably not the loan book

👨🏻🔬 Remember your high school science class (tbh, I blocked mine out, but maybe you were less traumatized)? You start with the simplest hypothesis and try to disprove it. In this case, the obvious explanation is that one fund simply owns worse loans.

Whelp, based on publicly available information, that doesn’t appear to be the case:

If you stopped your diligence here, you’d probably conclude these funds should behave similarly under stress. Many of the portfolio metrics are remarkably close.

Even software exposure (the one thing everyone is panicking about right now) isn’t nearly as different as the headlines suggest. Oaktree actually discloses more software exposure: 18% vs 14% in OCIC (more on that later).

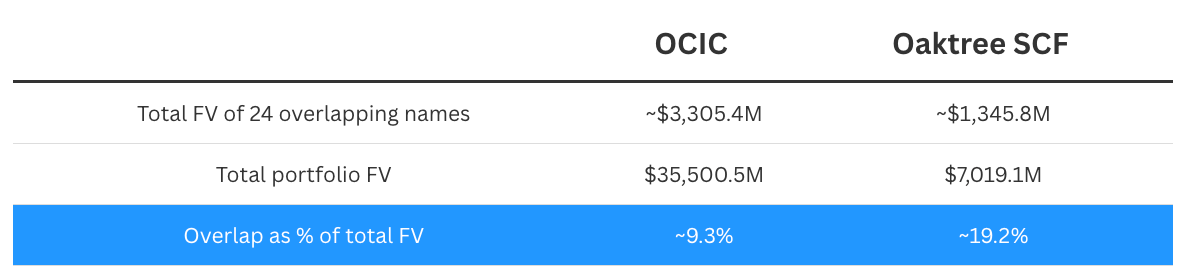

I was apparently single-handedly responsible for datacenter demand on July 4th (the day I’m writing this), because I compared the holdings of both funds for your enjoyment.

Both funds even own the same problem child: Pluralsight. (That one's still lingering on the books. I should probably do another write-up) - I first wrote about it here, then here:

Even fundraising tells the same story. The two funds expanded almost in lockstep through Q4 2025:

If this were only about the loans, we’d probably stop here. But that’s where the story gets interesting: