Evergreen Funds, Part 1

Everything you wanted to know, but were too afraid to ask

Evergreen funds have become the vehicle of choice for “democratized” access to alternative assets. So today, I’m going to democratize something far more valuable: your understanding of these vehicles.

Yes, we’ll cover what evergreen funds actually are (along with the finer points of interval and tender-offer structures), but these three concepts is what I really need you to walk away with:

1️⃣ Incentives: how evergreen structures and fee models shape GP behavior

2️⃣ Performance drivers: unrealized gains meet performance fees

3️⃣ Liquidity: the mechanics of redemptions

“Leyla, what are unrealized gains?”

I’ve written deep dives on a number of evergreen vehicles:

KKR Private Equity Conglomerate (K-PEC) (private equity),

Bluerock Total Income + (real estate),

Carlyle Credit Solutions (private credit), and

Today’s piece puts all of that into context.

⏳ A Brief History of the Private Markets Universe

First (back when dinosaurs roamed the earth, in the 1970s and 1980s), a handful of enterprising finance guys started buying private companies, fixing them up, and selling them for more money. They delivered great returns and, naturally, needed OPM (other people’s money) to scale. Eventually, they had enough willing backers to start raising funds.

In those early days, if you wanted to invest in such funds, you had to be mega-wealthy (and well-connected) to even be allowed past the velvet rope. Minimum checks were large, the circles were small, and returns were eye-popping.

As institutional investors, spurred in part by the Yale endowment’s success under David Swensen, began piling in, they became the primary source of capital for the next two decades.

Fast-forward to today. Democratization has entered the chat. Funds now need to be accessible to the masses (read: lower minimums) and offer at least some liquidity (because retail investors may actually be less patient with their capital than their institutional brethren).

Enter evergreen vehicles:

These funds are designed to solve multiple problems all at once:

• access to illiquid assets (private equity, CRE, private credit, secondaries, etc)

• offer some degree of liquidity

• investment minimums that make them accessible.

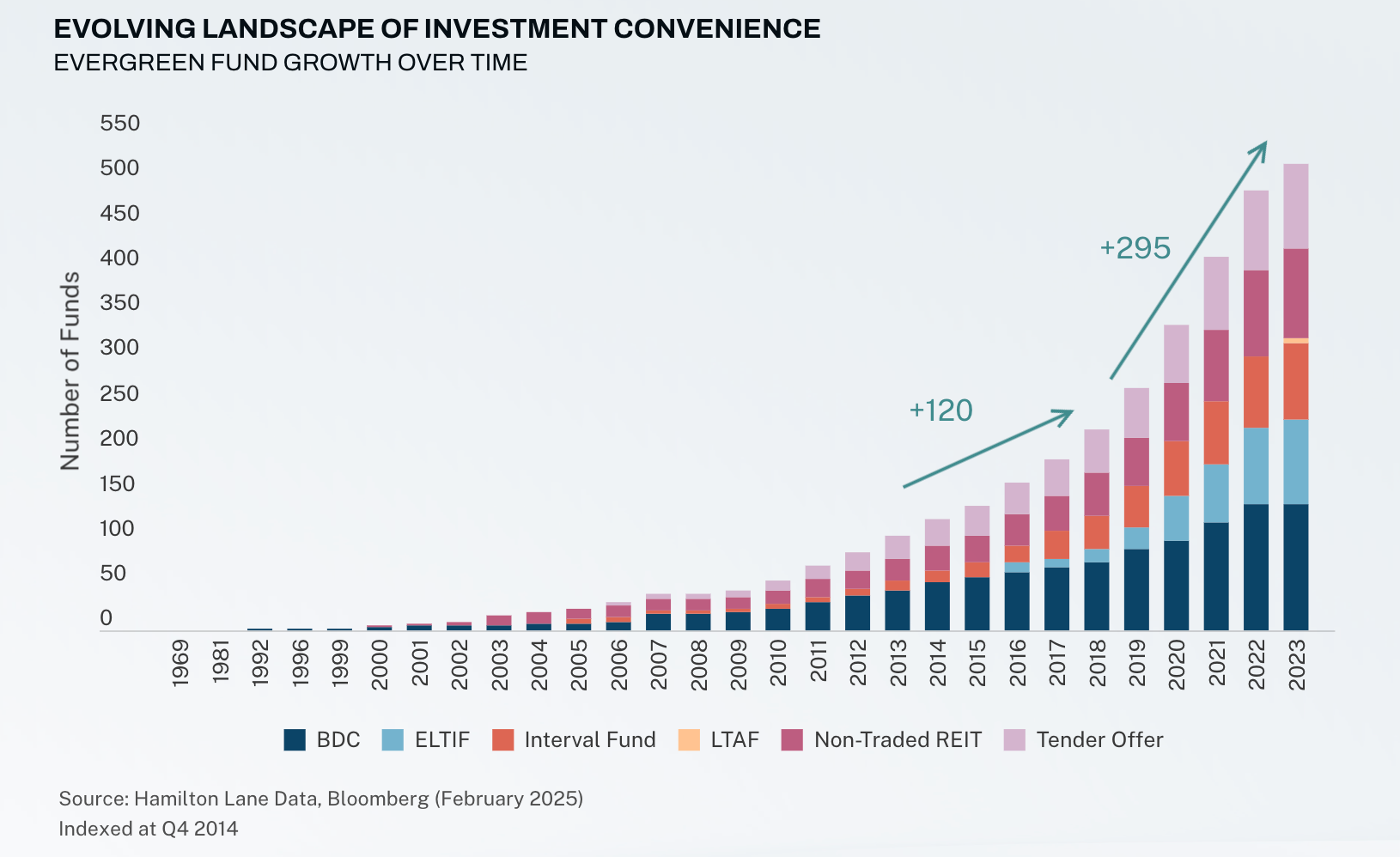

🌲 Evergreen Funds

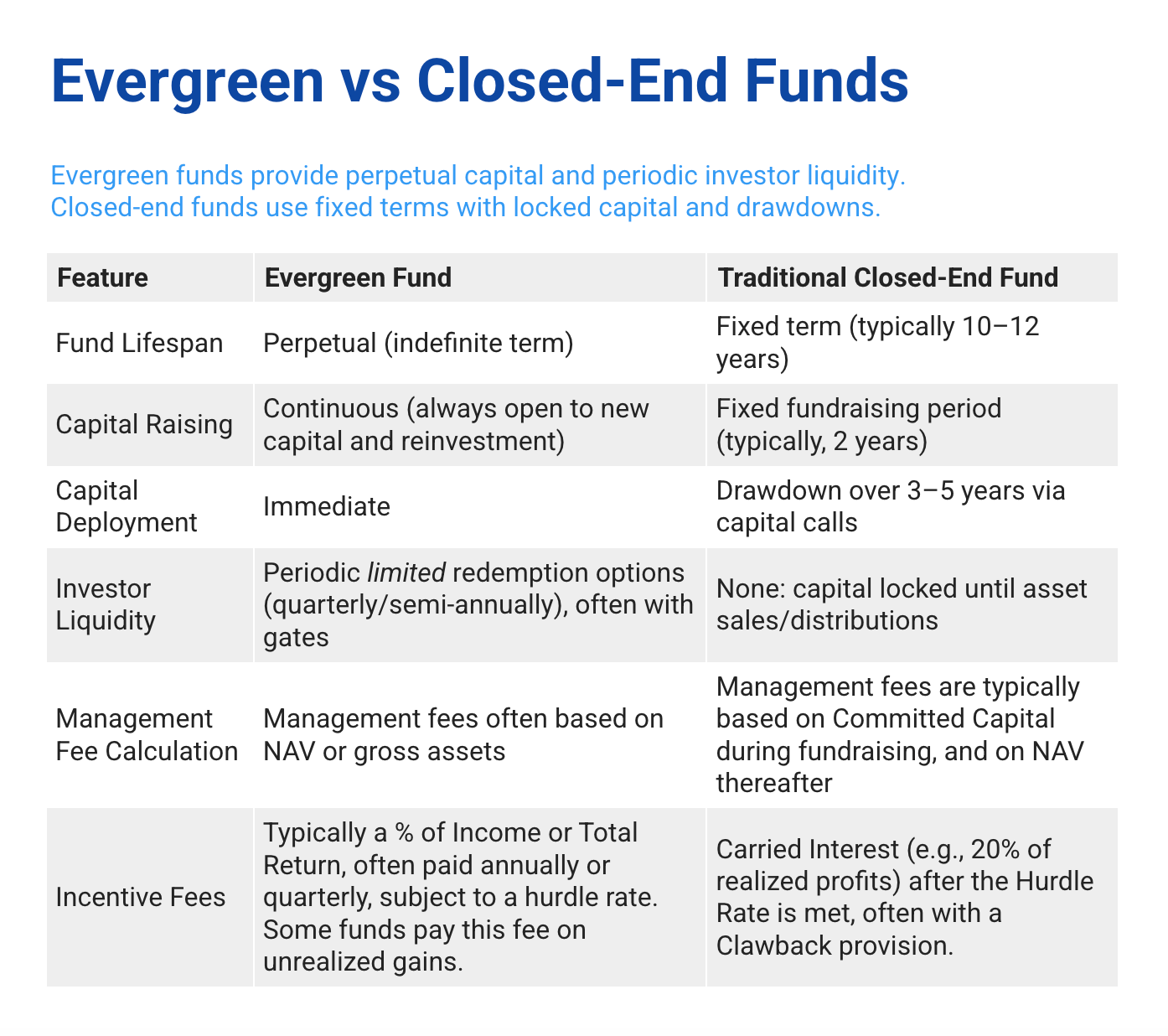

Evergreen funds (AKA open-ended, semi-liquid, or perpetual-capital funds) differ from traditional private equity or credit funds in their structure, term, and liquidity. They’re built to operate indefinitely and accept new capital continuously while offering periodic redemptions.

Before we get to the nuts and bolts of different structures, let’s address the elephant in the room: what behaviors does this evergreen structure encourage?

1. Let’s Talk About Incentives

Perpetual Fee Base

Management fees are charged on a continuously growing NAV. Indefinitely. This creates a powerful incentive to grow AUM, not necessarily to maximize underlying asset quality. And speaking of fees, they are not immaterial*: