Inside the Sale of Kayne Anderson Real Estate

Funds, managed accounts, pitch decks, a back-of-the-envelope M&A model (and Whole Foods).

Most LPs spend their time valuing assets. We rarely think about what the investment manager itself is worth.

That’s what makes this case study by CRE Analyst so interesting.

Bridgepoint’s acquisition of Kayne Anderson Real Estate offers a rare window into how alternative asset managers are valued, what buyers are actually paying for, and why recurring management fees can be worth far more than carried interest. This is an inside look into alignment, fundraising, operating leverage, and what it takes to build a platform that’s valuable beyond the underlying real estate.

👉 Browse our full library of commercial real estate analysis, deep dives, and case studies here (link). And here’s a recent fund write up:

About the author

CRE Analyst is the research brand behind FastTrack, the commercial real estate training program now in its seventh year with 2,000+ alumni. Founded by an institutional fund manager and a regional developer, it draws on 35 years of commercial real estate experience across acquisitions, development, asset management, research, and fund management. Reach CRE Analyst at admin@creanalyst.com, or on LinkedIn.

Al Rabil started Kayne Anderson Real Estate from scratch in 2007 and built it into an emerging juggernaut. He and David Selznick built a cash machine, and it shows off everything that makes real estate investment platforms attractive:

Differentiation. Run out of Boca Raton, Kayne made its name in medical office, senior housing, and student housing. A different path than the coastal office crowd.

Growth. The first fund raised $136 million. The latest, KAREP VII, closed at $5.12 billion in May 2026, oversubscribed against a $3 billion target and 86% larger than the fund before it.

Big margins. EBITDA margins run around 50-60% today, on a path to 65-70%.

Five weeks after that record close, Kayne sold. In an uncertain market, Rabil and Selznick had two options:

Option 1: Clip ~$100 million a year in profits as a medium-sized platform, let a billion-dollar net worth ride on the paper value of the firm, and pray for continued outperformance.

Option 2: Take a $759 million cash payday today, clip strong comp going forward, potentially earn another ~$344 million in earnouts, and still pray for continued outperformance.

They chose Option 2.

This article explains why they, unlike most real estate investment managers, had the ability to sell at a big number, and what the sale means for the rest of the space. This deal is more complicated (and more interesting) than the headlines suggest, with buried signals for every other investment manager.

Deal Points: Bridgepoint + Kayne Anderson Real Estate

Deal:

Bridgepoint is acquiring Kayne Anderson Real Estate, a $22 billion alternative-sector real estate platform, from Kayne Anderson.

The business will be rebranded Kayne Bridgepoint and is expected to close by year-end 2026.

Price:

$1.393 billion upfront EV, split 55% cash / 45% stock: $759 million cash plus $634 million in Bridgepoint shares. Potential 2030 earnout of up to 102.5 million additional shares tied to management-fee hurdles.

Strategic impact:

Bridgepoint AUM rises from ~$95 billion to ~$117 billion, adding real estate as a fifth vertical alongside PE, credit, infrastructure and secondaries.

Real assets rise to ~45% of AUM and US-domiciled management fees increase from 28% to 42%.

Economics:

Bridgepoint acquires 100% of KARE’s FRE, 15% of carry in certain historic funds and up to 35% of carry in future funds.

The deal is expected to be mid-single-digit EPS accretive in 2027 and >20% accretive in 2028.

Next steps:

Al Rabil and David Selznick will continue leading the platform with ~100 professionals.

Closing is subject to shareholder approval, regulatory clearances, fund consents and separation of KARE from the wider Kayne Anderson business.

Inside the Kayne fee machine

If you were building a real estate investment manager, what would you rather have: a big perpetual fund or a series of closed-end funds? Kayne Real Estate has both.

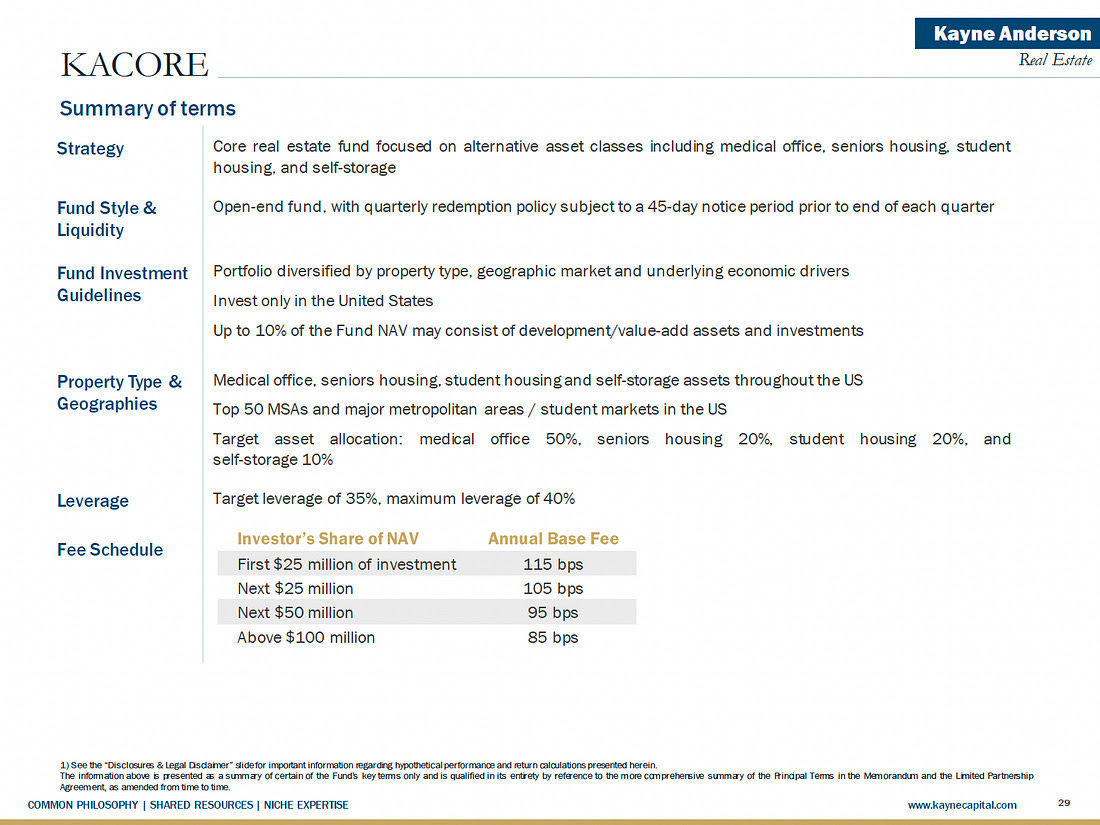

Kayne Anderson Core Fund (KACORE)

KACORE is Kayne Anderson Real Estate’s ~$4 billion open-end, perpetual core fund, launched in 2017. It owns stabilized, income-producing real estate in Kayne’s specialist sectors, medical office, senior and student housing, and storage, with room to put up to roughly 10% of capital into development and value-add. The fund targets a 9–10% net total return, with about 4–6% of that coming from income.

Structurally, it’s an evergreen, NAV-based vehicle: no fixed fund life, capital comes in and out through a contribution and redemption queue, and it runs around 34% leverage. In short, it’s the stabilized, permanent-capital way to own Kayne’s demographic-driven sectors, built for steady income rather than opportunistic upside.

At KACORE’s fee schedule (see below from a pension fund pitch), $5 billion in net assets generates $40-60 million of fees. $10 billion in net assets generates $80-120 million. And $20 billion in net assets generates $170-230 million.

From a platform perspective, this is the beauty of a lower-intensity, open-end vehicle: scaled operating costs. If it takes 5 people to run a $5 billion core fund, how many people does it take to run a $10-20 billion fund? 10? Even at $1-2 million each, operating profit scales substantially. …which helps to explain why platforms love the idea of these open-end vehicles (a topic for another post).

No doubt that KACORE was a desired component of the platform and, if it continues to outperform, could drive meaningful margins in the future.

Kayne Anderson Real Estate Partners (KAREP)

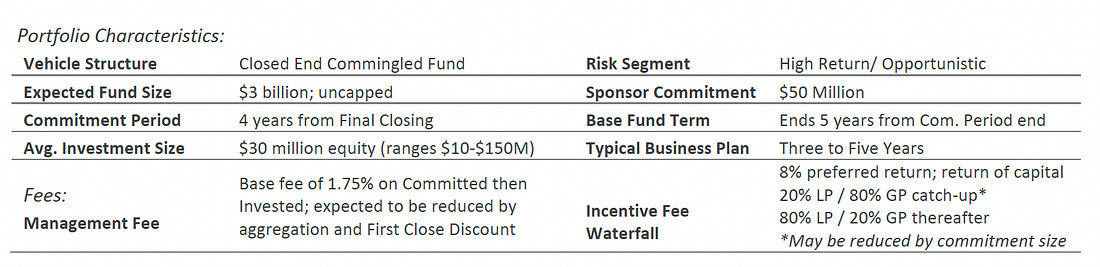

The star of the Kayne Anderson show is KAREP, Kayne’s flagship closed-end, value-add and opportunistic equity series, which launched in 2007 and is now on its seventh fund. Where the core fund owns stabilized assets for income, KAREP goes for appreciation: it acquires, develops, and repositions real estate in Kayne’s specialist sectors, medical office, senior housing, student housing, multifamily, and light industrial, then sells at a profit. It targets a 15-18% net return (18-21% gross), typically using 65–70% leverage over a roughly five-year hold.

Structurally, it’s a drawdown fund with a finite life: investors commit capital, it gets called and invested over a commitment period, and the fund harvests and winds down over about 8–10 years.

It charges a base fee of 1.25%–1.75% on committed capital (1.75% early, stepping down), an 8% preferred return, and a 20% carried interest. The record behind it is the reason it keeps growing: a 15% realized net IRR since inception and mostly top-quartile results across a 19-year track record.

Here’s what Bridgepoint flagged in its Kayne acquisition announcement:

| A guest post by

|