SREIT: What Happens When You Buy at the Peak?

How an $11 billion fundraising boom became a 48-month redemption crisis

I presented in a real estate MBA class at UC Irvine last week (Go, Anteaters!), and a great question came up:

“What happens to funds that raised billions in the Sunbelt at the market peak?”

It so happens that we have the perfect case study: Starwood Real Estate Income Trust. The fund raised $11.2 billion in 2021–2022, right as multifamily real estate peaked. Just a little over three years later, NAV is down 29%, redemptions are frozen, and investors who invested at the peak can currently access exactly $0.

“How do non-traded REITs come up with asset valuations?” Here you go:

👉 And here’s a recent case study on the subject:

In today’s post, we’ll look at what happened with SREIT: the fundraising surge, the redemption spiral, the leverage dynamics, and what can happen when fundamentally illiquid assets are placed inside a liquid wrapper (also, I have homework for you)

And here’s a fun case study on a single multifamily deal in Houston (acquired in 2022):

Disclosure: This case study is provided for educational and informational purposes only and should not be construed as investment, legal, tax, or financial advice. The views expressed are solely those of the author. All examples are illustrative in nature and not guarantees of future outcomes. Readers should conduct their own independent research and consult with qualified professionals before making any investment or financial decisions.

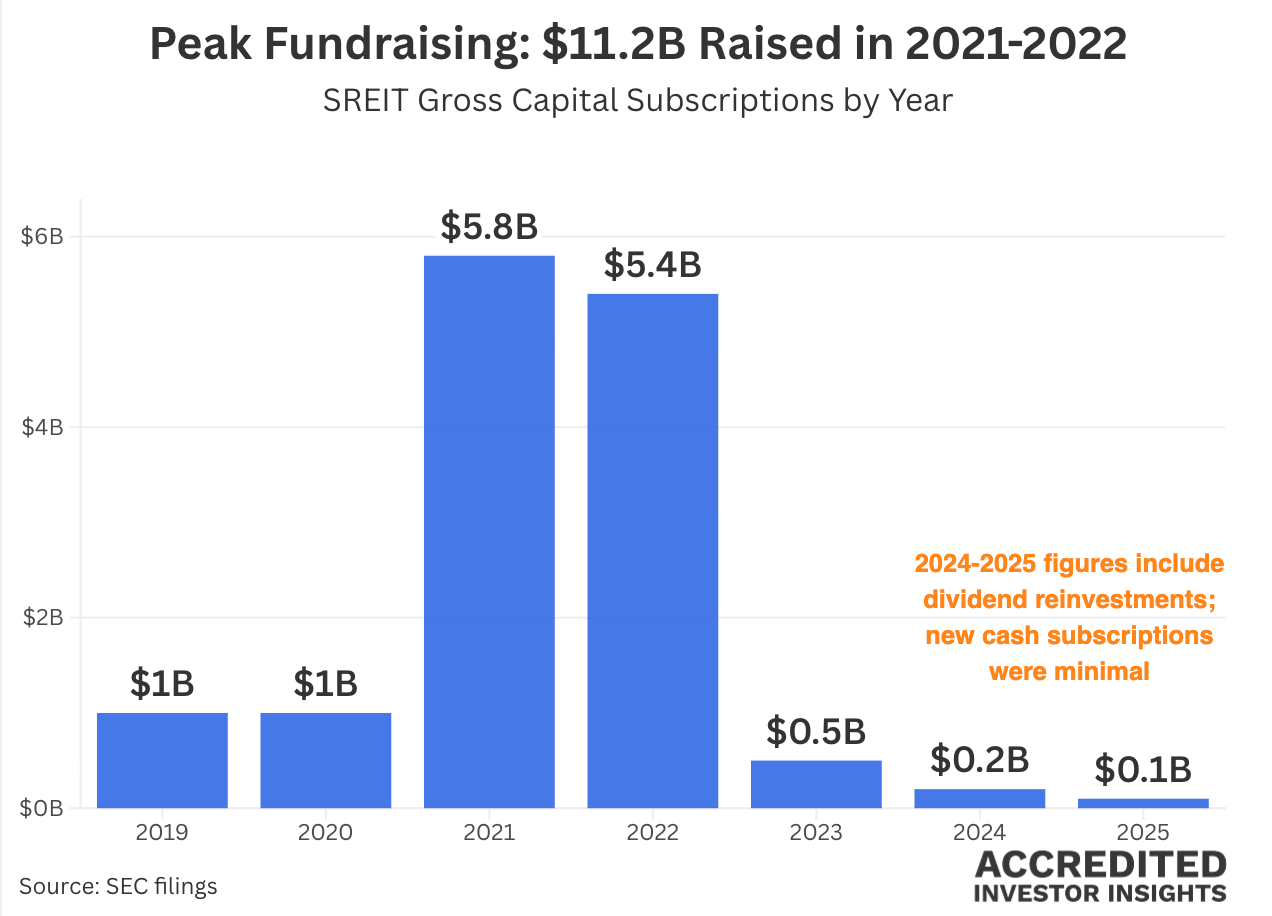

Raising Billions at the Peak

Starwood REIT’s fundraising tells the story of the euphoric years in commercial real estate. After modest growth from 2019–2020, subscriptions exploded: $5.8 billion in 2021, followed by another $5.4 billion in 2022.

That $11.2 billion was raised at the absolute peak.

What were they buying? As of December 2022, 65% of assets were multifamily apartments, and 58% of the portfolio was concentrated in the South (primarily Texas, Florida, Georgia, and Arizona).

In other words, this was a leveraged bet on Sunbelt multifamily at the exact moment valuations were peaking (and roughly a year before supply went parabolic).

The pitch was compelling: stable income from essential real estate, tax-efficient distributions, and professional management.

The reality: they were buying apartments at the top of the cycle, just as supply surged and interest rates were about to spike.

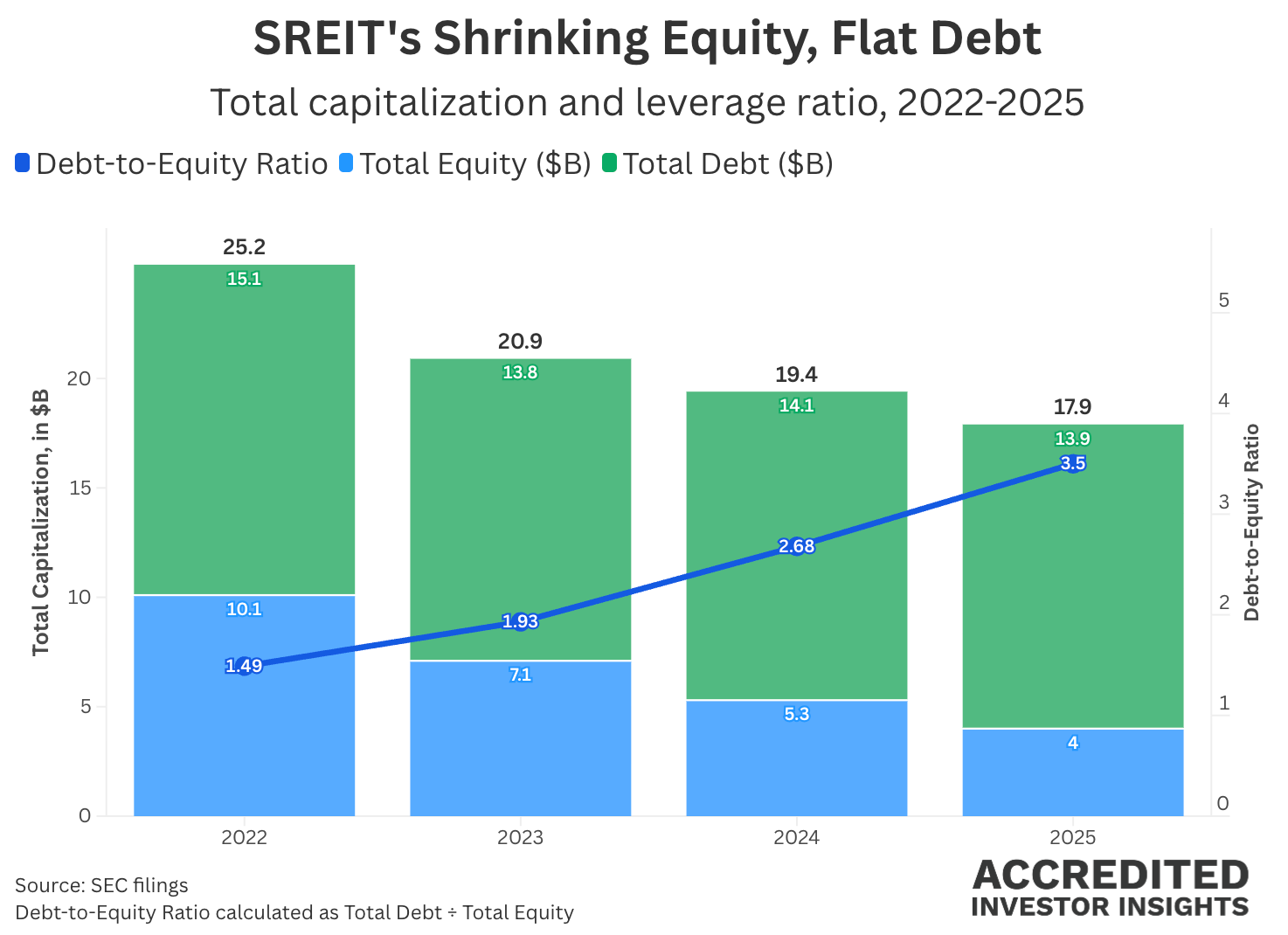

Liquidity Meets Leverage

Evergreen real estate funds face an age-old problem: they promise monthly liquidity while owning illiquid assets.

That works beautifully until it doesn’t.

When real estate values decline, redemption requests accelerate. One option is to shrink a fund into oblivion gracefully: sell assets, cut distributions, de-lever, and slowly return capital.

Starwood chose a different path.

As redemption requests accelerated through 2023–2025, the fund sold assets ($1.2 billion in 2025 alone), but did not materially reduce leverage.

Total debt stayed roughly flat at around $14 billion, while equity collapsed from $10.1 billion in 2022 to $4.0 billion in 2025. The debt-to-equity ratio exploded from 1.5x to 3.5x, while NAV per share fell from $26.34 to $19.65.

The fund’s stated leverage policy targets 50–65% (debt net of cash divided by gross real estate assets). By late 2025, actual leverage had climbed to approximately 64–67%, effectively sitting at or above the high end of the stated range.

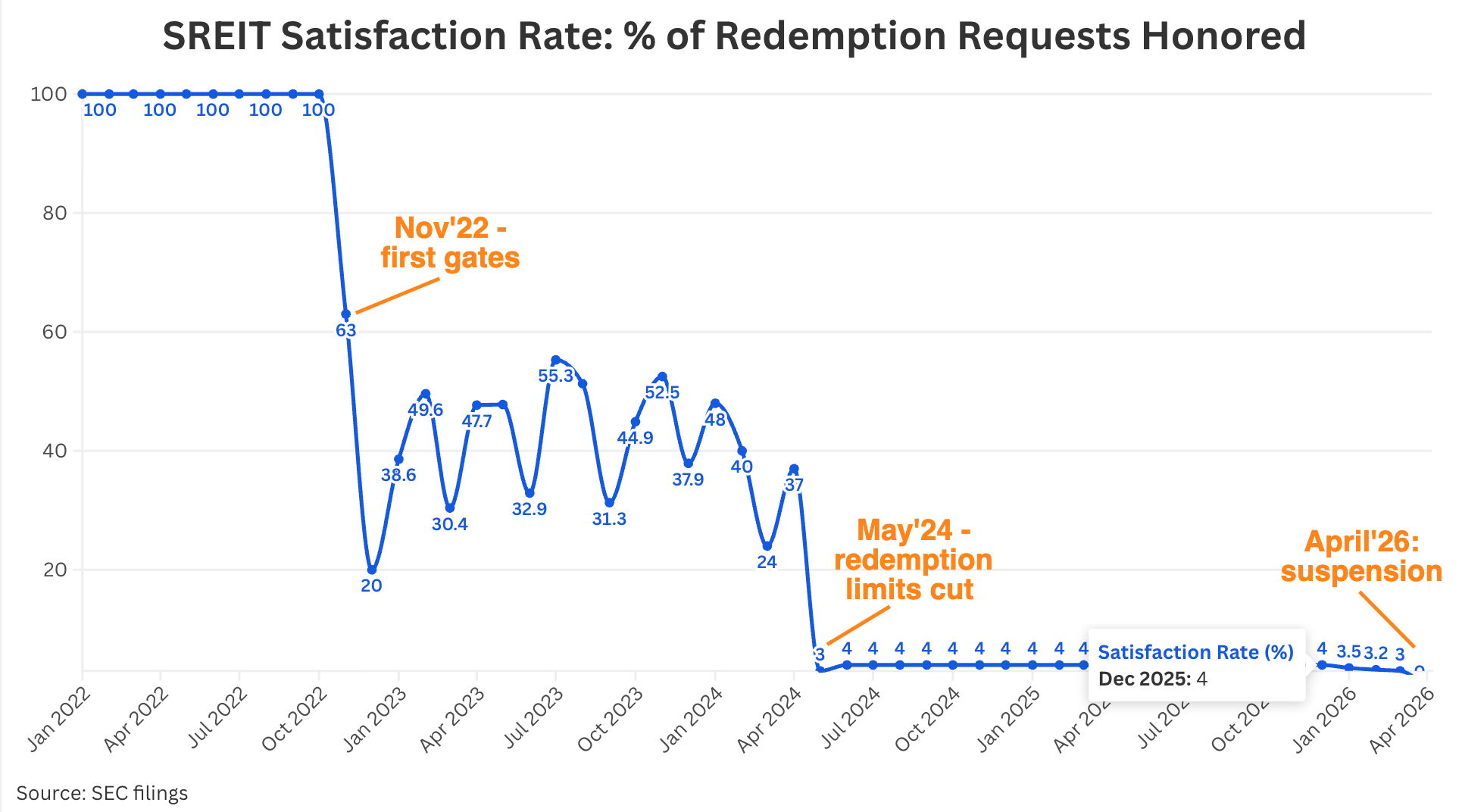

100% to 0% in 48 months

The redemption tsunami happened as they usually do:

slowly, then suddenly.

From January through September 2022, Starwood honored 100% of redemption requests.

In October 2022, requests hit 2.2% of NAV for the first time, exceeding the stated 2% monthly limit. The board made a fateful decision: waive the limit and pay 100% anyway.

Redemption requests jumped to 3.2% of fund’s total NAV in November, then 4.2% in December. Gates came down.

November satisfaction rate: 63% (meaning investors received liquidity for only 63% of the shares they submitted for redemption).

December satisfaction rate: 20%

The run had started.

Throughout 2023, satisfaction rates bounced between 30–55% as the fund tightened redemption limits. Then came May 2024: the monthly redemption cap was slashed from 2% to 0.33% (an 84% reduction).

Satisfaction rates collapsed to roughly 3–4% and stayed there.

By Q4 2025, the math had become impossible. The fund’s quarterly redemption limit was approximately $122 million. Meanwhile, investors were requesting roughly $1 billion per month, while only about $40 million was being honored monthly.

At that pace, it would take roughly 25 months to clear just one month’s redemption queue.

The fund suspended redemptions entirely.

Distributing What You Don’t Earn

Another problem was unfolding beneath the redemption panic: Starwood was paying out far more than it earned.

From 2023-2025, the fund distributed $1.461 billion to shareholders. But after paying property operating expenses and interest, distributable cash flow was only ~$894 million.

The ~$567 million shortfall was effectively funded through asset sales. In other words: part of the “yield” was simply investors getting their own capital back.

Every distribution check slowly eroded NAV per share, creating a vicious cycle:

Falling NAV triggered more redemptions

Redemptions forced asset sales

Asset sales pressured NAV further

By the time distributions were reduced to 4.7% in April 2026, the damage had largely been done.

The Fee Story

A brief aside on fees: while investors watched their capital evaporate, management collected $346 million in fees from 2023-2025 ($153M, $105M, $88M in each year, respectively).

Performance fees ($204 million in 2021 and $102 million in 2022) rewarded the team for buying at the peak. And when management received fee payments in shares, they redeemed them outside the queue at 100% satisfaction while regular investors got 4%.

Maybe it’s just me, but the optics aren’t great.

Leyla’s Notes

Some closing thoughts. First, I don’t think investors will lose all their equity here. But I do think it’ll take a while before redemptions resume.. Importantly, there are some lessons from this fund that we can all learn from:

1. Peak fundraising is peak danger.

When a fund raises record amounts, it’s usually because everyone else thinks it’s a great idea too (which means you’re late. I’m learning this lesson myself, btw). Starwood’s $11.2 billion in 2021-2022 was the warning sign.

2. Liquidity promises on illiquid assets don’t survive downturns.

One has to give. If you're after liquidity, public markets offer a way to allocate to any given strategy with daily liquidity. Public REITs took a beating during the same period, but investors could exit them at any point. The illusion of liquidity in non-traded REITs evaporates precisely when you realize you need it. Want illiquid assets? Drawdown funds are a better vehicle.

3. If distributions consistently exceed earnings, pay attention.

A fund can distribute more than it earns for a surprisingly long time. I see this done across different asset classes, and different deal sizes:

👉 BCRED is currently distributing more than it earns in net investment income:

👉And here’s a one-off multifamily deal that does the same:

But consistently funding distributions through asset sales or return of capital is not accretive to NAV. Ever.

4. What Could Have Been Done Better (open for debate, comment section is yours)

Unfortunately, when a fund finds itself in this pickle, there are no good options. But arguably, the least bad path may have been:

Limit redemptions aggressively and early (perhaps below 1% monthly)

Cut distributions sooner

Sell assets and de-lever, even if losses become realized

Shrink the fund before leverage becomes unmanageable

Last resort: publicly list the vehicle and let the market clear the price.

None of these options are attractive. But delaying reality often compounds the eventual damage.

5. What’s a Better Opportunity?

The below should not be considered investment advice. Would I allocate to this fund at this moment in time? Absolutely not, and for a variety of reasons.

Publicly traded REITs offer a much more compelling opportunity at this moment, because many of them are trading at fairly high implied cap rates, and cover distributions from the actual cash flow. Of course, many do not, so do your homework. Public REITs may be down 20-30%, but at least the price is honest and the exit door is open.

The best opportunities will be in REITs (and new vintage Regulation D funds) that are well-capitalized to buy new assets, are not burdened with too much debt, and don't deal with redemption issues. In other words: the opposite of Starwood REIT's current position.

Thank you for reading!

-Leyla

P.S. Letter to shareholders

If you made it this far, I have some homework for you. Go read this letter to shareholders, come back and tell me what you think.

What do I think? They’re hoping and praying the macro turns.

The letter is a masterclass in hope: waiting for interest rates to fall, for the Iran conflict to end, for Fed Chair Kevin Warsh to be seated, for multifamily supply to decline. The subtext: we need a miracle.

There is a point where someone forces the lenders to wake up and become more active. The remaining NAV is based on the ability to forestall a compelled liquidation for benefit of creditors, in which case the equity value could approach zero. This is a textbook stress test for the semi-liquid, leveraged model that seems to exist mostly for the purpose of accommodating enormous fees.

For Note #1. In 2021 actual rent growth was 20% in some locations. That was another retrospective lesson for me. When you see unreal rent growths, run away, it's too late for new money.