Cliffwater Corporate Lending Fund (CCLFX): The Machine Slows Down

Rising redemptions, falling NAV, and what's happening below the surface

Back in March, I compared the $31.5 billion Cliffwater Corporate Lending Fund (CCLFX) to Star Trek‘s Doomsday Machine.

For years, it behaved like one: assets grew at a 46% CAGR, and the fund went on to become one of the largest private credit vehicles available to ordinary investors. It consumed capital the way my teenagers consume groceries (and other resources): continuously, and without remorse.

I ended that piece with a question: is the machine still eating, or is the planet starting to eat back?

The annual report is out, and the May repurchase results are in. TL;DR, friends: the planet is eating back.

Here’s the first part of the series:

Here’s what we’ll cover in today’s update:

Redemption activity

What’s contributing to the decline in NAV per share

What’s happening with the portfolio

Let’s get into it. (Pour the coffee. You’ll want it.)

Disclosure: This case study is provided for educational and informational purposes only and should not be construed as investment, legal, tax, or financial advice. The views expressed are solely those of the author. All examples are illustrative in nature and not guarantees of future outcomes. Readers should conduct their own independent research and consult with qualified professionals before making any investment or financial decisions.

The Buyers Left

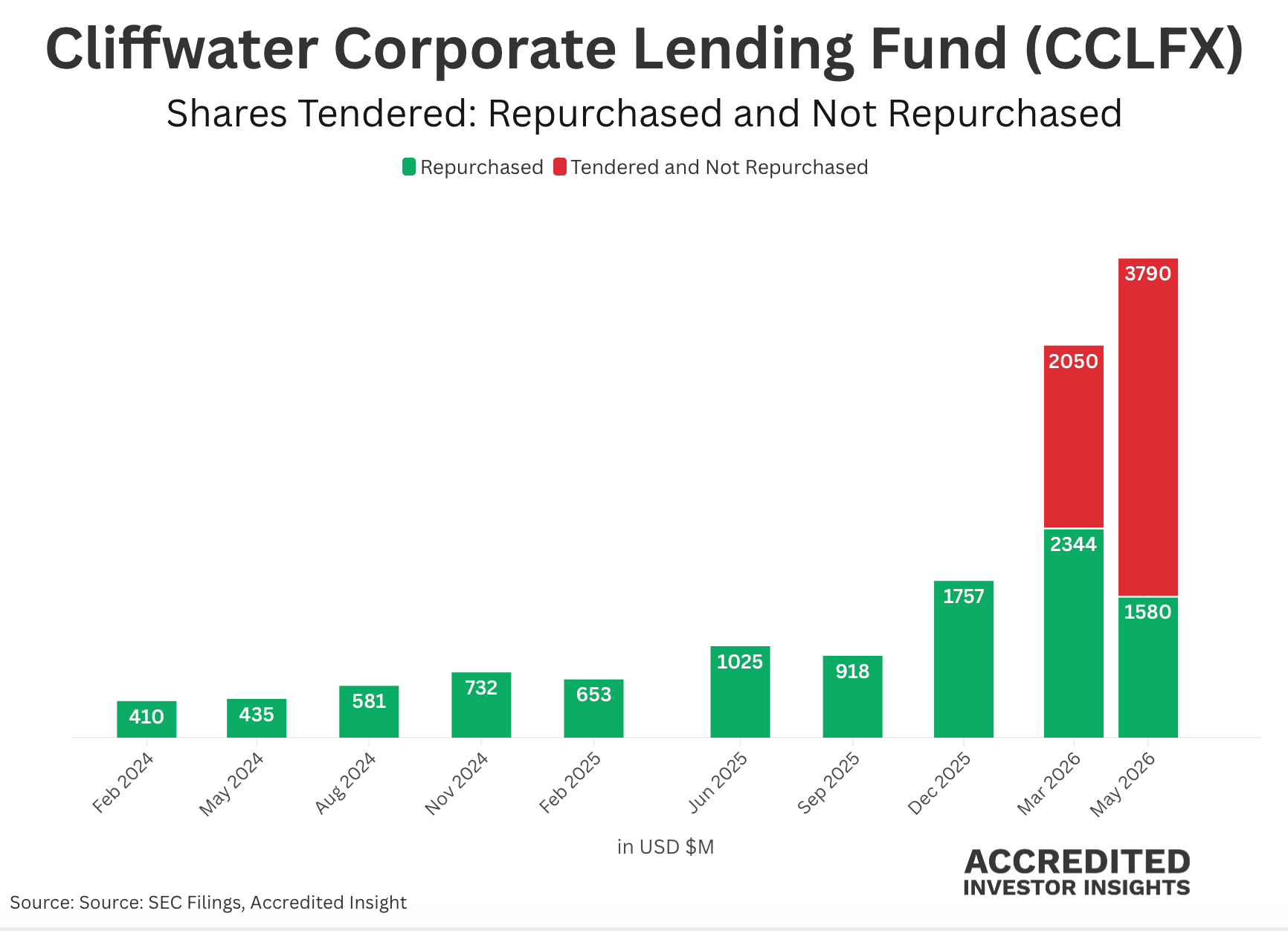

When I last wrote about CCLFX, the headline was a single oversubscribed repurchase offer. Investors asked to pull ~14% of the fund. Cliffwater honored about 50% of those requests. At the time, it wasn’t clear whether that was a one-quarter panic or the start of a trend. (Spoiler: it was a trend).

We now have more data points. Here’s every repurchase offer since the start of 2024:

Look at what the fund did with its gate as the pressure built. In March, it went all the way to the 7% ceiling (the maximum it can repurchase before it’s legally required to prorate). In May, with more people asking to leave, it pulled the cap back down to 5%.

But redemptions are only half the demand story. The other half is what the people who stayed decided to do with their money: