Is There Any Magic in $OZ?

Investors should be careful not to let the tax tail wag the dog.

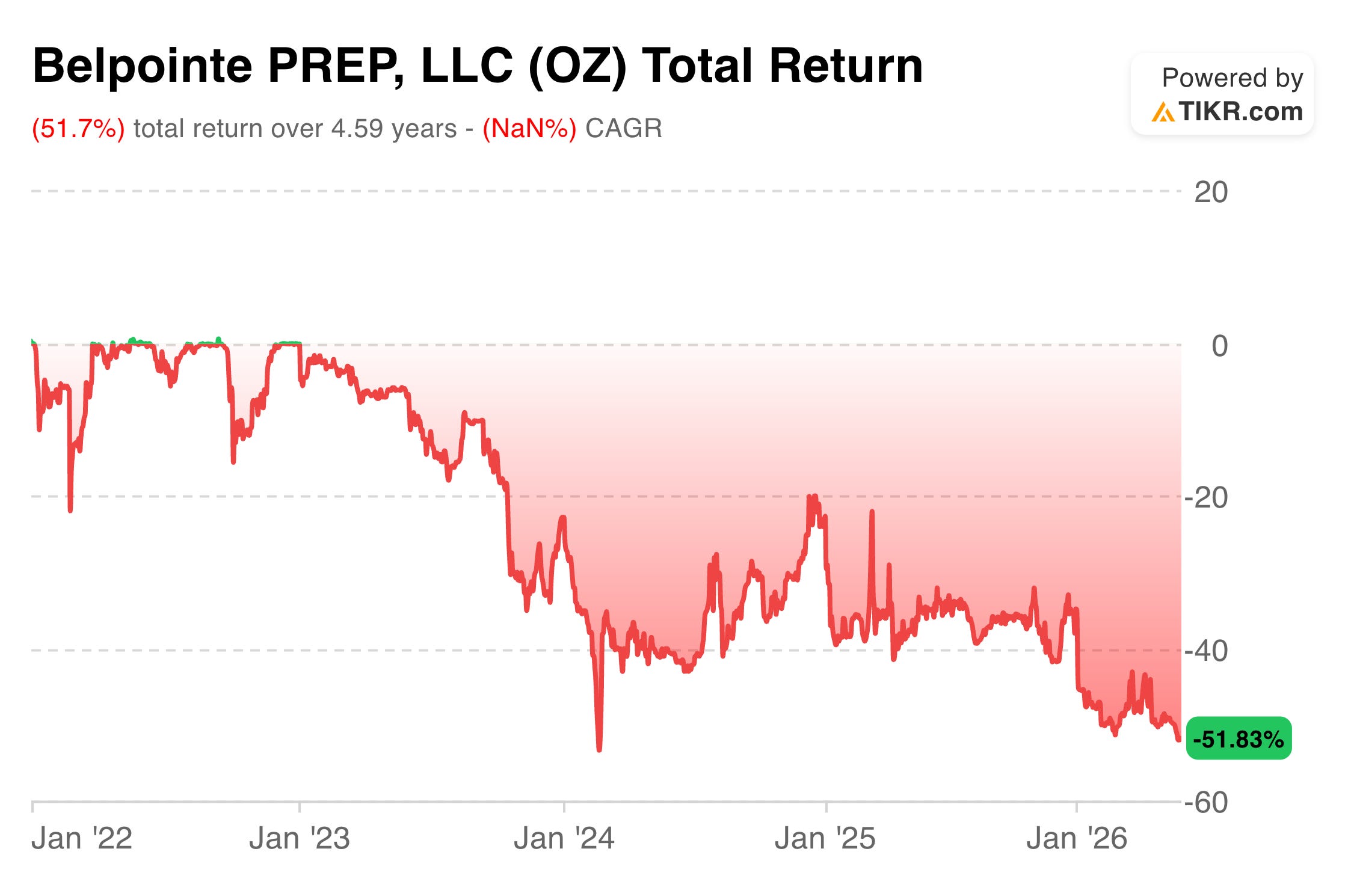

Belpointe PREP, LLC (ticker OZ) went public in late 2021 with a compelling pitch: become the first publicly-traded partnership structured as a Qualified Opportunity Fund, combining OZ tax benefits with the liquidity of exchange-traded units.

On paper, the idea sounds compelling. Belpointe is structured as a partnership for U.S. federal income tax purposes, meaning income passes through to investors (avoiding corporate-level taxation) while still qualifying for Opportunity Zone benefits. Investors get K-1s like any private OZ fund, but with the added advantage of NYSE liquidity. Put it all together, and you have what was marketed as a powerful tax-advantaged vehicle with unprecedented flexibility.

The reality has looked very different. Since going public, OZ shares have declined 51.8%.

In today’s guest post, Paul Drake takes a closer look at Belpointe OZ and walks through several structural red flags that investors may want to understand before chasing the tax narrative.

👉 If you're unfamiliar with Opportunity Zones or wondering about the December 31, 2026 tax cliff, we recently published primer:

Speaking of real estate, here’s a post on tax efficiencies in private placement real estate, and another one on phantom income.

-Leyla

About the author:

Paul Drake is a former award-winning physicist and professor who now writes about value investing at Focused Investing, specializing in REITs and energy markets. Since taking control of his portfolio in 2020, he's outperformed the S&P 500 through focused research and disciplined strategy across market cycles.

The purpose of Opportunity Zones, in their present incarnation since 2017, is to incentivize investment in undercapitalized communities. They do this primarily by enabling temporary deferral or permanent exclusion of capital gains produced by investments in those zones. There are details, but they need not distract us today.

So one can invest in property in such a zone, with the hope that enhanced investment throughout the zone will produce a significant increase in value that one can eventually harvest. But one will still owe taxes on current income throughout.

To get around that, why not put the properties in a REIT, so that no taxes are owed at the corporate level? That is what Belpointe OZ (OZ) is doing.

Belpointe present themselves as a real-estate development company with a focus on mixed-use and multifamily properties. They have two properties in lease-up and four in pre-development, at a total cost of $1B.

They also describe themselves as a “public Qualified Opportunity Fund,” enabling easier exits for investors. They expect to designate new OZs every 10 years, and are about to transition from OZ 1.0 to OZ 2.0.

But we don’t need to explore the details here, for reasons discussed next.

🚩🚩🚩🚩🚩

There are a bunch of red or orange flags about OZ.

🚩 Red Flag #1. They are externally managed with, as usual, misaligned incentives detailed in their 10-K. The manager gets paid more for increasing NAV, even if this is done by diluting shareholders. NO publicly listed REIT with this structure has performed well for shareholders (to my knowledge, and I’ve seen a lot of them). For me this is a terminal red flag.

🚩 Red Flag #2. They are also what NAREIT labels a “Diversified REIT.” In their 10-K, they describe their investments as

located in qualified opportunity zones for the development or redevelopment of multifamily, student housing, senior living, healthcare, industrial, self-storage, hospitality, office, mixed-use, data centers and solar projects located throughout the United States and its territories.

By far the poorest historical gains among classes of listed REITs have come from the Diversified REITs. There are real benefits to being focused and today the markets respond to that. To be fair, the current investments by OZ are more concentrated.

🚩 Red Flag #3. Their Debt Ratio is 48%, which is too high to support a secure dividend. No quality listed REIT is that high these days. The office REITs tend to run near 50%, and we’ve seen lots of dividend cuts in recent years even among those doing relatively well, as one could have predicted. I recently discussed Why Leverage Often Does No Good.

🚩 Red Flag #4. They are operating at a substantial loss even after adding back in depreciation. They claim that their initial developments are ongoing, that they will refinance at stabilization, and then start paying dividends. They say nothing I could find about what their capital allocation policy will be.

This REIT seems a bit reminiscent of Clipper Realty (CLPR), whose business model has long involved leveraging gains in property value to support further new development. Clipper’s dividend never has had much relation to their underlying economics.

In my opinion, the tax benefits from opportunity zones do not come remotely close to making up for these flaws.

This call is easy. Beware the seductive siren of OZ.

P.W. If you are new here, check out our other articles on:

Case Studies (with many on real estate deals and funds)

One of my favorite articles: capital stacks

| A guest post by

|

Here via Paul Drake

I think I've rarely seen so many red flags pop up at a short notice.

Then again, the analysts I follow tend to mention stocks they recommend, not stocks to absolutely avoid.

Whenever the tax tail wags the dog...