Is Partners Group Private Equity (Master Fund) Showing Its Age?

A nine-year case study in subscriptions, redemptions, fees, and what mature looks like in evergreen private equity.

Private equity evergreen funds don't get sick. They just develop chronic conditions. Rising redemptions here, slowing exits there, a credit facility draw that wasn't there six months ago. Nothing fatal. Just a lot of things happening at once (I’m starting to experience this myself, even though I technically am NOT an evergreen fund).

🩺 The early symptoms are easy to miss. A redemption rate that doubles. A credit facility that goes from zero to $711 million in six months. A net cash inflow that quietly reverses into the negative zone for the first time in nine years.

Partners Group Private Equity (Master Fund), one of the oldest and largest evergreen PE vehicles in the wealth channel, is having that kind of moment.

Here’s a fund from the same asset manager that’s youthful and energetic:

Today we’ll take a look at:

The usual: how it works, what’s in it, and what it costs

The less usual: where returns come from (and how that’s changed)

And finally: whether a $16 billion mature evergreen fund still makes sense when you have alternatives

💡 If you missed the UNREAL Gains Part 1 and Part 2 discussion, you’ll find it enlightening.

Disclosure: This case study is provided for educational and informational purposes only and should not be construed as investment, legal, tax, or financial advice. The views expressed are solely those of the author. All examples are illustrative in nature and not guarantees of future outcomes. Readers should conduct their own independent research and consult with qualified professionals before making any investment or financial decisions.

The Pitch

Partners Group Private Equity (Master Fund) is one of the largest evergreen private equity funds available to wealth-channel investors, with ~$16 billion in net assets as of September 2025.

The value proposition is straightforward: access to institutional private equity through a semi-liquid structure. Investors gain exposure to a globally diversified portfolio of direct investments, secondary acquisitions, and primary fund commitments that would typically be difficult to access individually.

Liquidity is offered through periodic tender offers, subject to Board approval and available fund liquidity.

Here’s how tender offer funds differ from interval funds:

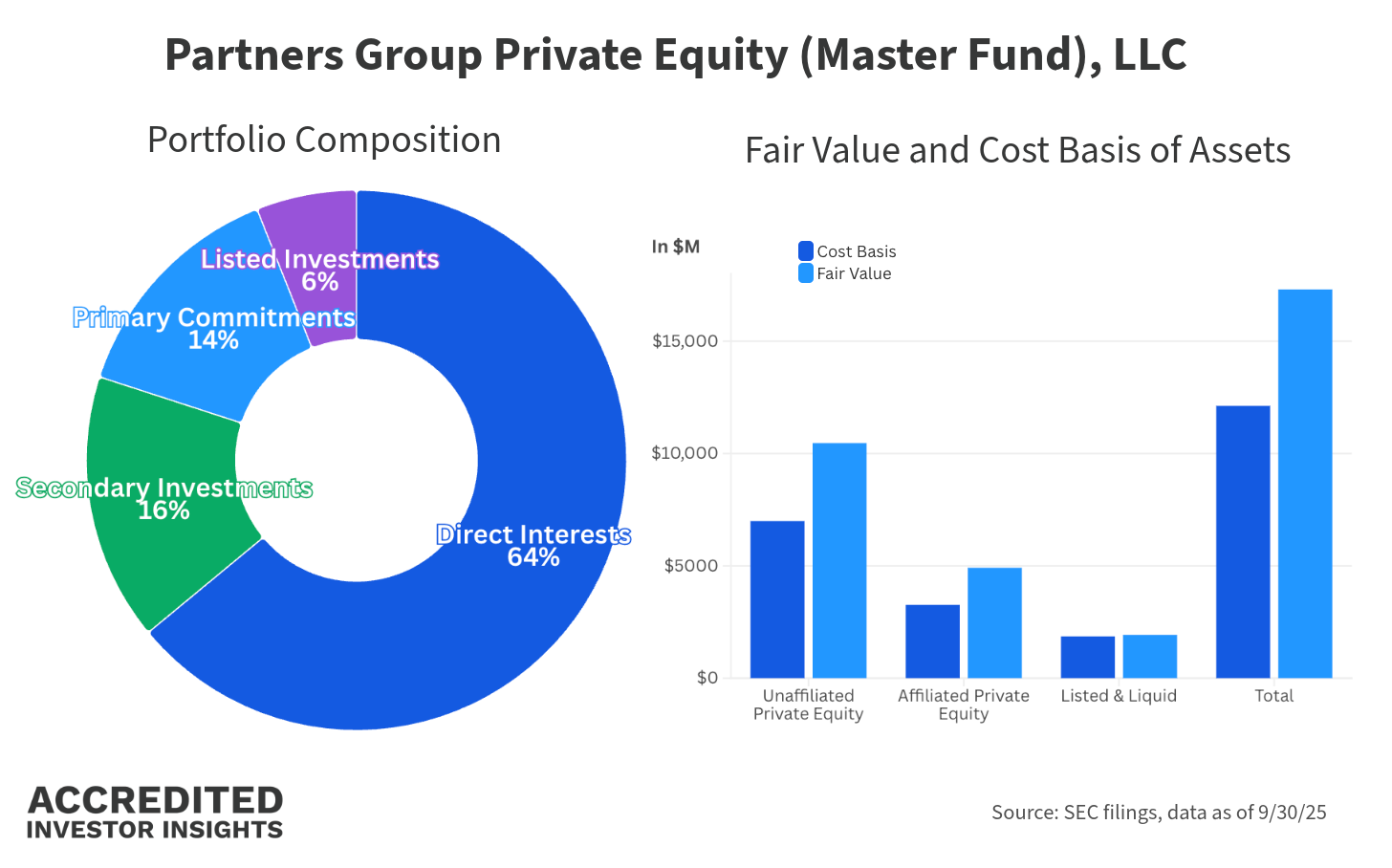

What’s in the Fund

The portfolio is broadly diversified across investment types, with exposure to:

417 direct investments

223 primary fund commitments

81 secondary investments

110 listed investments

As of September 30, 2025, the portfolio looked like this:

The fund does not provide a detailed industry breakdown. Based on management commentary and the schedule of indirect investments, technology and healthcare appear to be among the larger sector exposures, though precise allocations are difficult to determine.

One disclosure worth noting is that approximately 30% of the portfolio consists of primary and secondary fund investments valued using the NAV practical expedient. In other words, Partners Group is largely relying on valuations reported by underlying fund managers, with adjustments made when deemed appropriate.

Visibility into the underlying holdings for that portion of the portfolio is limited.

Here’s how that works:

Roughly 90% of the portfolio is classified as Level 3 assets. That’s not unusual for private equity: most portfolio companies do not trade on public exchanges, so observable market prices generally don’t exist. It does mean, however, that reported values are heavily dependent on valuation models and assumptions.

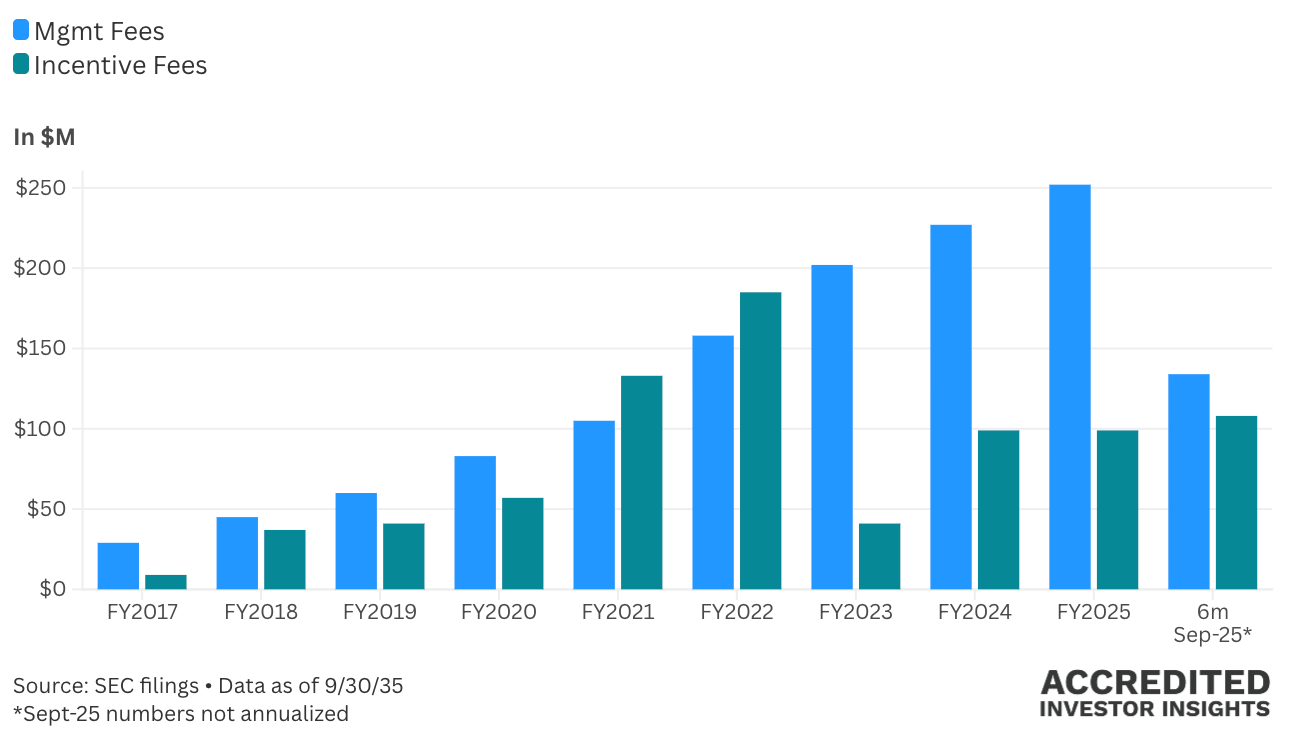

Which brings us to the most transparent part of any evergreen fund: the fee structure.

Fees

Like most evergreen private equity vehicles, the Master Fund has multiple layers of fees. Some are visible in the financial statements. Others are embedded within underlying funds and never appear in the reported expense ratios.

Here’s what investors can see:

1️⃣ Management Fee

The management fee is 1.50% annually, calculated monthly on the greater of:

NAV, or

NAV less cash, plus unfunded commitments

Because unfunded commitments are included in the calculation, the fee base can exceed NAV. The effective management fee is capped at 1.75%.

2️⃣ Incentive Fee

The incentive fee is 10% of net profits, calculated and paid quarterly.

Importantly, net profits include both realized and unrealized gains.

There is no hurdle rate.

Instead, the fund uses a “New Loss Recovery Account”. After periods of negative performance, incentive fees are paused until prior losses are recovered.

❗️In practice, this is not a hurdle rate. It does not require investors to achieve any minimum return before the manager can participate in gains. It simply delays fee collection after drawdowns, and then resets once performance turns positive again.

Class A investors pay an additional 0.70% annual distribution fee on top of the above, plus a potential one-time placement fee of up to 3.50%. Class I is not subject to either.

In dollar terms, here’s what the fee structure has generated over time:

And there’s something else worth holding in mind before we move on.

Since FY2019, the fund has generated negative net investment income every single year.