UNREAL Gains

Part 1: The Mark-Up Machine (or How to Turn Discounts Into Returns)

In its first eleven days of operation, Franklin Lexington’s private markets fund deployed ~$326 million into 20 secondary positions and one co-investment.

By December 31, 2024 (just eleven days after inception), those positions were reported at approximately $377 million in fair value, generating ~$52 million in unrealized gains before the fund had completed its first two weeks of existence.

By March 31, 2025 (just over three months from inception), the fund’s assets had grown to approximately $1.3 billion, and the manager had earned roughly $11 million in incentive fees.

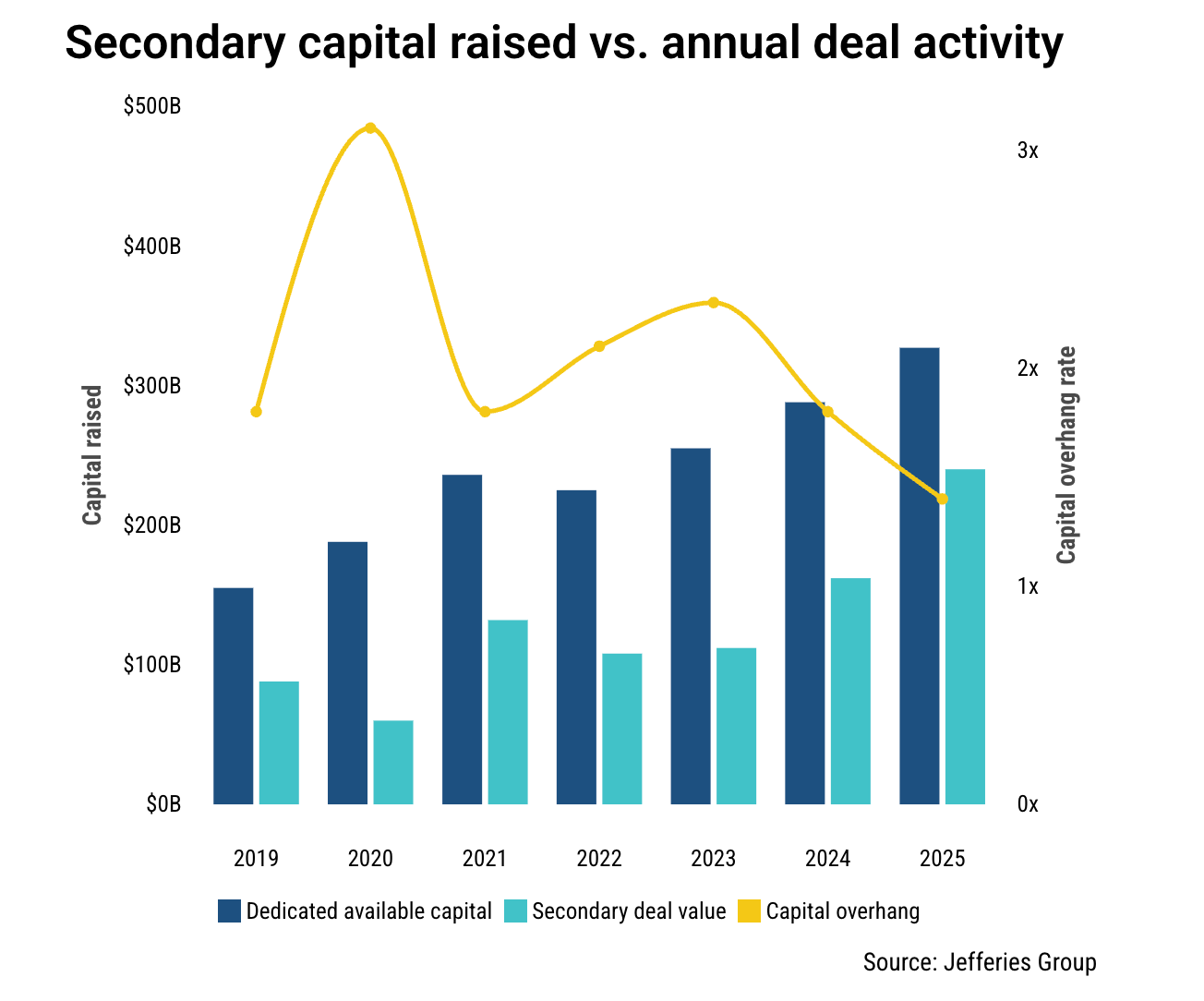

Franklin isn't alone. I analyzed five major evergreen private equity funds launched between 2022 and 2024 with 50-98% of assets allocated to secondaries: Franklin Lexington, Coller Secondaries, Carlyle AlpInvest (deep dive here), Ares Private Markets (read more here), and FS MVP Private Markets Fund1. In total, these funds represent a combined $11.6 billion in assets.

The pattern was nearly identical across all five: early returns overwhelmingly driven by unrealized gains from marking discounted secondary purchases to sponsor-reported NAV.

Welcome to the strange intersection of ASC 820, private equity secondaries, and evergreen fund structures. Oh, and UNREAL gains (a term I stole from Mark Higgins, CFA, CFP, whose newsletter you should subscribe to).

“Leyla, what in the world are you talking about?” Here’s your primer on evergreen secondaries:

👉 Want some case studies on secondaries evergreens? Here’s Coller Private Credit Secondaries (LINK), Carlyle AlpInvest (LINK) and Partners Group Next Generation Infrastructure (LINK).

The Nuts and Bolts of ASC 820

Under ASC 820, investment funds are permitted to use underlying managers’ reported NAV as a “practical expedient” for fair value. This means a fund can purchase a secondary stake at a discount, then immediately mark the investment to the sponsor’s reported NAV (even when that NAV is materially higher than the transaction price).

No independent appraisal required.

❗️More importantly, the transaction price itself does not determine the carrying value❗️

The practical expedient exists for a reason. When the guidance was introduced, secondary markets for private fund interests were relatively small, illiquid, and opaque. Investors often had little observable pricing data beyond the underlying manager’s reported NAV.

The issue isn’t that secondary purchases should never appreciate toward NAV (discount capture is a legitimate investment strategy). The questions are:

Whether it still makes sense to mark up assets immediately when we now have observable secondary market pricing, and

whether managers should get paid quarterly on paper gains that haven't been tested by an actual exit.

Today, that market looks very different.

Secondary transaction volume in private equity has grown dramatically over the past decade, and evergreen private market vehicles have grown like mushrooms2 🍄 after rain as sponsors seek to bring private markets to a broader investor base (“democratization of alternatives”, and all).

For secondaries-focused evergreen funds, the playbook is brilliantly simple:

Buy discounted secondary interests

Mark them to sponsor-reported NAV

Record immediate UNREALized gains

Show great total returns (and in some instances, get paid real dollars in performance fees)

Raise additional capital at the higher NAV

Repeat

As long as the accounting treatment remains unchanged, the early-stage economics can be extremely attractive (I’ll show you just how attractive in a minute).

This fund is an excellent case study on the topic (guest post by TheAltView, whose newsletter you should also subscribe to)

The mechanism can also work in reverse: if updated NAV information implies lower values than transaction cost, the practical expedient can produce immediate markdowns as well. We saw that with Bluerock:

‼️ Importantly, this is a non-issue in a traditional drawdown fund structure, where investors commit capital upfront and unrealized marks are eventually tested through realizations over the life of the vehicle.

Evergreen funds operate differently. New investors continuously subscribe at current NAV. If that NAV already incorporates immediate mark-ups from discounted secondary purchases, future investors may effectively buy into unrealized accounting gains before those gains are ever validated through exits.

Last month, Mark Higgins, Tim McGlinn and I submitted a formal agenda request to the Financial Accounting Standards Board (FASB), asking the Board to reevaluate the continued appropriateness of ASC 820’s NAV practical expedient when observable secondary transaction data exists (Institutional Investor).

Side Note on Reporting

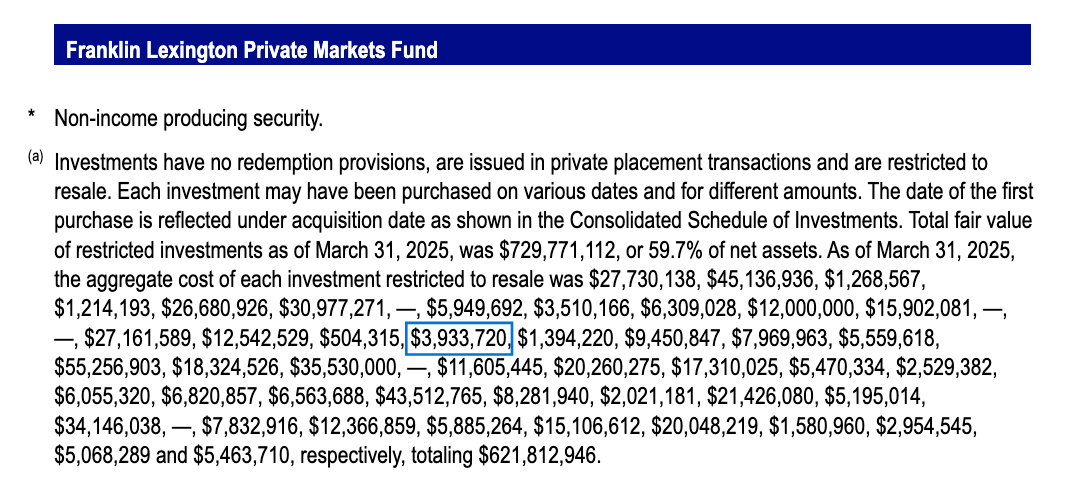

Franklin’s disclosures were also notable in how they presented acquisition cost. Funds are required to disclose cost information, but there is no standardized reporting format for how these figures must appear.

This fund did the same, btw:

In Franklin Lexington’s case, the cost basis shows up in supplemental footnotes rather than directly alongside fair value within the Schedule of Investments. Like this:

That one fund, with the cost of $3.9M? That’s Resolute Fund V, L.P. Form N-PORT reported its fair value at $60,104,327 (a 1400% gain) as of the same day, 12/31/24.

Granted, reconstructing every single position is reserved for those who enjoy inflicting accounting pain upon themselves (I do it for you, dear reader), and doesn’t really matter in the grand scheme of things.

The aggregate economics are already visible in the filings themselves: ~$326M of investments reported at ~$377M in fair value after the fund’s first eleven days of operation, generating approximately $52 million in net unrealized gains.

The Pattern

By now you should realize where I’m going with this: Franklin Lexington isn’t an outlier.