Retail Done Right (Case Study)

Dissecting a retail deal that delivered a 23% IRR - and why it's not a unicorn

Today’s case study might look like a unicorn for two reasons:

It’s refreshingly transparent about what actually happened (and for the love of all that’s good, LPs, you need to demand transparency, here’s why);

A 23% IRR with a 3.8x equity multiple isn’t exactly a 2025 market norm.

Except — it’s not a unicorn. Because this GP has repeatedly executed this exact scenario. Over and over again, over the course of a couple of decades. Today, we’ll dissect an actual deal, and see what went right.

For those of you evaluating retail deals, I’ve included one of my go-to AI prompts at the end of this post.

But before you grab your lab coat…

Accredited Insight is the only publication offering a clear, unfiltered view from the LP side of the table. We cover private credit, private equity, and CRE investing, drawing on hundreds of deals we’ve seen.

Paid subscribers get full access to our growing library of 30 case studies and our in-depth series on how to read a CRE proforma. If you are a GP, this is your window into the world of capital allocators. Click below to choose your plan:

👉 $10/month or $100/year.

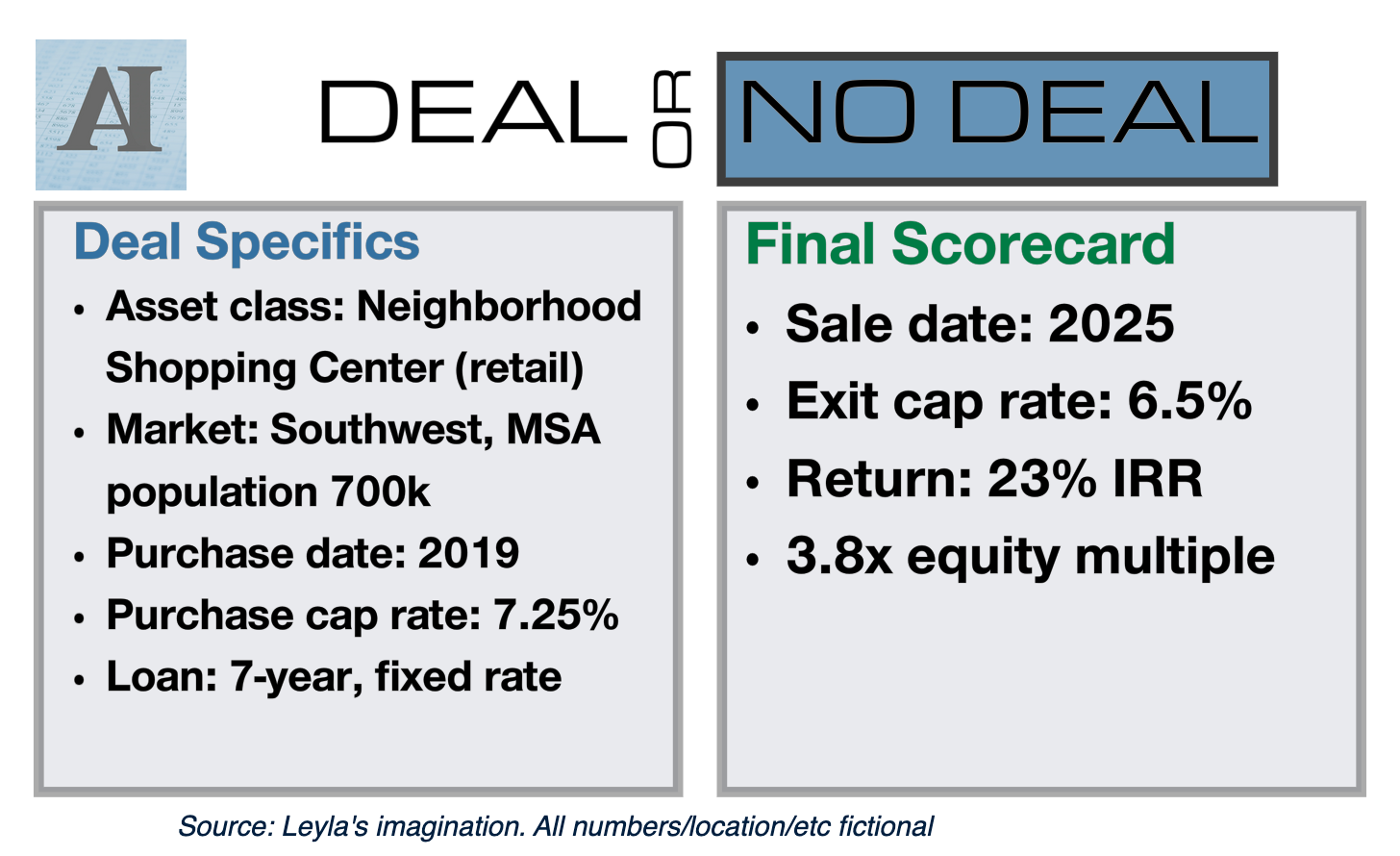

Deal or No Deal?

Just a friendly reminder: this is for educational purposes only, not financial advice. Numbers, location, and details have been changed to keep the sponsor’s identity confidential.

The Deal at a Glance

Asset class: Neighborhood shopping center (retail)

Size: 50,000 SF (anchor tenant: national retail chain)

Location: A fast-growing suburb, secondary market in the Southwest.

This post will help you evaluation deal location:Acquired: 2019

Hold period: 6 years

Capital structure: Straightforward deal, one class of equity, financed with a 7-year loan at 65% LTC. For more on capital structure:

Business plan: Value-add via lease-up, tenant mix upgrade, operational efficiencies, and deferred maintenance cure.

What They Did Right

The GP’s value-add strategy wasn’t Earth-shattering, but it was executed well. Here’s what they did:

Rebuilt the rent roll: GP negotiated stronger leases and re-anchored with a national retail chain. Contractual base rents up ~28% from acquisition.

Deferred maintenance clean-up: spent about $250K in repairs and improvements, making the property functional and marketable.

Cost controls: operational expenses trimmed without cutting into tenant or shopper experience.

NOI growth: increased by ~50% over the hold period (CAGR ~5.8%).

Why NOI growth is important to track:

The Exit

The property was acquired in 2019 at a 7.25% cap rate. By the time of sale, the team had achieved roughly 75 bps of cap rate compression, exiting at about 6.5%. The buyer? Institutional capital, drawn to a fully stabilized asset in a high-growth submarket.

Yes, some of the returns came from cap rate compression, but one could make a strong argument the GP made the property more attractive to an institutional buyer by stabilizing it, and brining in higher quality tenants. There is a lot to be said about selecting the right location, as well.

Returns came in at:

~23% IRR

3.8x equity multiple (gross)

Are you having FOMO yet??

Takeaways for LPs

Value-add in retail isn’t just lease-up: it’s the combination of better tenants, better lease terms, and operational discipline.

Cap rate compression is a gift, not a given. It worked here because the sponsor bought well, executed consistently, and sold into strong demand. Caveat emptor: when it works the other way, things get ugly:

Boring can be beautiful. This deal didn’t require any magical tricks on the surface - but simple isn’t always easy. The debt was well-matched to the business plan: no surprises with floating interest rates re-adjusting upward (and given the loan was near term-end, we’ll assume prepayment costs were minimal).

If you’re looking at retail opportunities yourself, here’s one of the AI prompts I use to speed up my analysis (for a deeper dive on how I use AI, read this):