Cliffwater's Cascade Private Capital Fund (CPEFX)

23.5% of the portfolio is effectively a fund-of-funds-of-funds (you read that right)

This is Cliffwater’s third (and youngest) fund. The baby of the family, if you will.

As a parent of three, I can tell you the third one is always the wildest, because ain’t nobody got time for parenting anymore. (Please do not transpose this observation to private funds. Also, I’m not your mother or financial advisor).

Cascade Private Capital Fund (CPEFX) an interval fund-of-funds that went from $477 million to $5.3 billion in two years (and it’s still growing). In its four-year life, the fund has had four names and three managers. 85% of the portfolio is valued by NAV practical expedient, and returns are mostly driven by unrealized gains.

If you missed the CCLFX story, start here. It’s the firstborn:

And here’s Cliffwater’s middle child:

Disclosure: This case study is provided for educational purposes only and does not constitute an offer, solicitation, or recommendation to buy or sell any security or financial instrument. Nothing herein should be construed as legal, tax, investment, or financial advice. All opinions are my own and may change without notice. Readers should perform their own due diligence and consult qualified professionals before making any investment decisions.

The Back Story

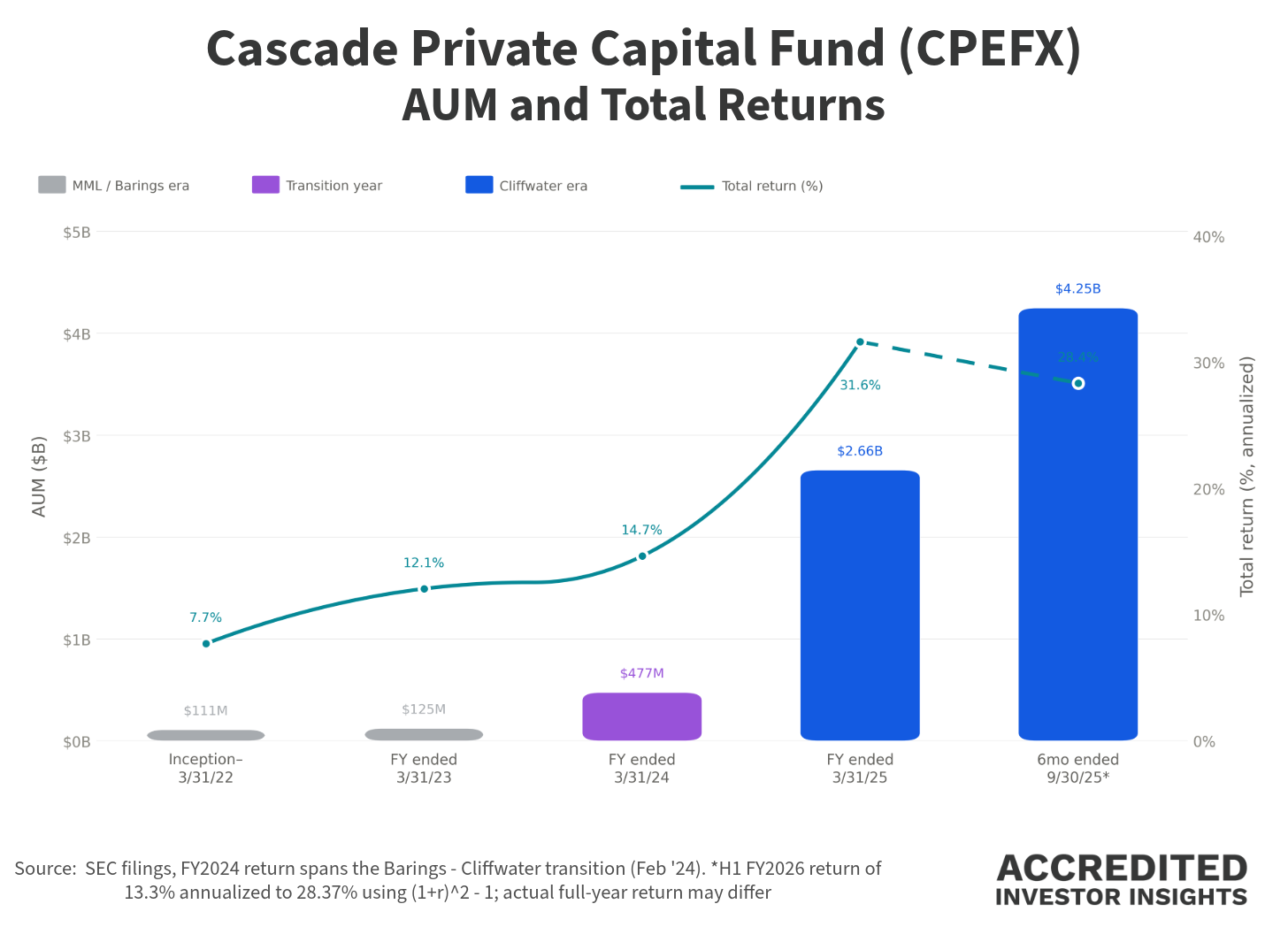

CPEFX was born in January 2022 as the MassMutual Access Pine Point Fund, a captive vehicle seeded entirely by MassMutual with $74 million of existing PE investments contributed in-kind.

For the next two years, MassMutual owned 100% of the shares, and showed 0% portfolio turnover. The fund cycled through two name changes and a handoff to Barings LLC before Cliffwater took over on February 27, 2024.

👉 At the handoff, net assets stood at ~$477 million. Nineteen months later: $4.25 billion. Here’s what the growth trajectory and returns look like:

Do you see what I see? In FY2025, the fund reported a 31.6% total return (here’s your reminder: high returns do not give you a pass on doing due diligence)

This is yet another “democratized” offering with no income or investor qualification requirements (firm minimum, however, is set at $25M).

This post shows you the mechanics of semi-liquid secondaries funds - it’s a fun one:

What It’ll Cost You

Cliffwater charges a 1.40% management fee on average daily net assets, but waived the entire fee through June 2025 and is charging 1.00% through June 2026.

Good news: that waiver saved LPs $20 million in FY2025.

Bad news: the waiver expires in June of this year.

There's no fund-level incentive fee, which is a meaningful positive. But CPEFX is a fund-of-funds (-of-funds), and here's where the fees live. The underlying PE managers charge their own management fees (1-2%) and carry (typically 10-20%).

The prospectus estimates this at 0.68% annually. ‼️ But read the footnote carefully: that figure excludes performance-based fees on realized gains. The 0.68% is a floor, not a ceiling, friends.

Here’s why you should read footnes (and how to do it without turning murderous):

🔎 What’s in the Fund

Well, I’ll cut to the chase: 23.5% of the portfolio is investments in funds-of-funds (which makes CPEFX’s position a fund-of-funds-of-funds).

Let’s start from the top. As of 2/28/26, CPEFX holds $5.3 billion in assets: