Loan Gone Bad: BCRED's Medallia Problem

A $1 billion loan, a 30% markdown. What does it mean for NAV?

Private credit has sold investors on a simple proposition: higher yields, floating-rate income, and lower volatility than public markets. Unlike traded bonds, private loans are not repriced every second. That can make returns appear smoother and portfolios more stable.

But when the marks are set by the manager, that smoothness is a function of accounting timing (rather than economic reality).

If public markets are an open pot of boiling water, private credit funds are pressure cookers: quiet on the outside, harder to inspect inside.

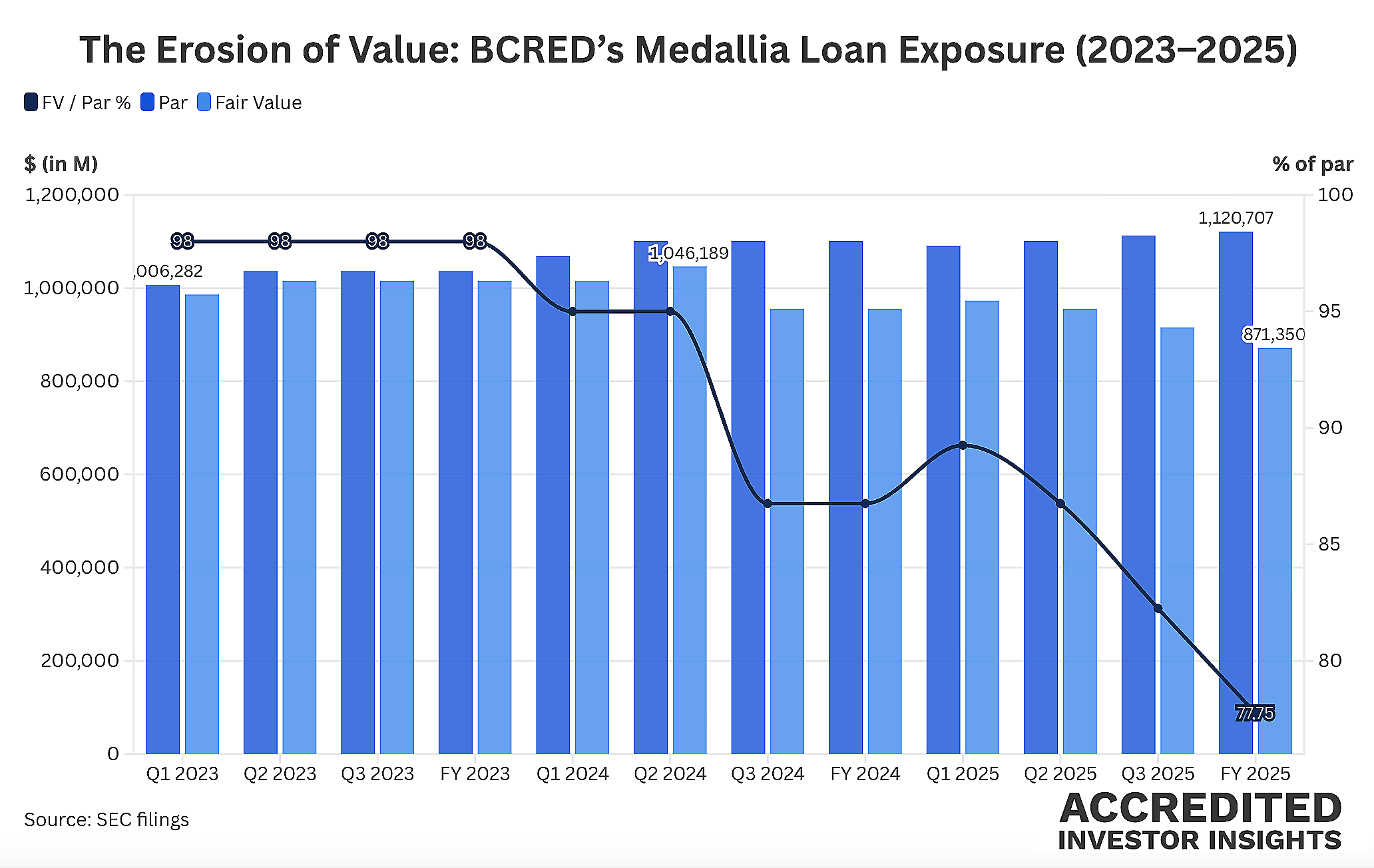

The unfolding restructuring of Medallia, a $1.1 billion position inside Blackstone Private Credit Fund (BCRED), offers a rare look inside the pot.

The mark has fallen from 98 cents to 78 cents to a reported 69 cents over three years. And yet the impact on BCRED’s $24.79 NAV per share will be almost imperceptible post-restructuring. That’s the good news.

That is not because the loss isn’t real. It’s because NAV already reflects the lower marks via unreali

zed losses. I'll walk through two hypothetical scenarios to show how that math works.

👉 This case study shows you how GAAP mechanics work when it comes to credit losses (pay attention to the side note about equity positions!):

The bigger question today’s case study raises: how many other Medallias are sitting in private credit portfolios right now? (that’s maybe the not-so-good news) - we’ll take a closer look at BCRED’s disclosures.

Disclosure: This case study is provided for educational and informational purposes only and should not be construed as investment, legal, tax, or financial advice. The views expressed are solely those of the author. All examples are illustrative in nature and not guarantees of future outcomes. Readers should conduct their own independent research and consult with qualified professionals before making any investment or financial decisions.

The Loan

In October 2021, at the peak of the pandemic-era software boom, Thoma Bravo acquired Medallia in a $6.4 billion leveraged buyout. Financing came from a who’s who of private credit lenders, including Blackstone, Apollo, KKR, and Antares.

Blackstone wrote the largest check, with BCRED holding more than $1.1 billion of par value exposure on its direct book.

It was a classic large-cap direct lending deal: sponsor-backed, scaled borrower, premium spread. But two features stood out:

The loan was underwritten based largely on Medallia’s annual recurring revenue (ARR), rather than traditional cash flow metrics. Public filings show that Medallia’s EBITDA was negative $109 million in 2021 (before the takeover). The lenders were betting on revenue growth converting to profitability.

The capital structure included payment-in-kind (PIK) interest. Rather than paying all interest in cash, Medallia could satisfy 5.6% of the rate by adding it back onto the loan principal (PIK is what you offer a company that can't generate cash).

A good read on the relationship between PIK and dividend yield:

When a borrower pays cash interest, lenders receive money. When a borrower pays PIK interest, lenders receive a larger loan balance. Reported income on lenders’ books climbs, and so does the borrower’s leverage.

And here’s how company leverage, interest coverage ratio, and enterprise value interact:

Between 2023 and 2024, BCRED’s direct par balance grew from roughly $1.0 billion to more than $1.1 billion, driven in part by capitalized interest. Across the lender group, total debt rose to approximately $2.8 billion, reflecting both PIK accrual and additional financing for add-on acquisitions.

The Warning Signs

The first sign of trouble was a 2024 amendment that widened the loan spread to SOFR + 6.5% and dropped the PIK component to 4.00%. That combination (a wider spread paired with reduced PIK) is what lender amendments look like.

Then the marks began to fall. Reported fair value went from the high 90s into the 80s, eventually reaching the high 70s by year-end 2025. Bloomberg subsequently reported that some lenders had marked the loan materially lower still: Blackstone and HPS Investment Partners (now part of BlackRock) wrote it down to 69 cents in February 2026, a nine-point drop in two months.

In late 2025, the lender group made a pivotal decision: they refused to extend the PIK arrangement, which expired at year-end. Medallia would now have to pay its full contractual interest in cash.

According to Bloomberg, the switch to all-cash interest will increase Medallia’s annual debt servicing costs by approximately $100 million to nearly $300 million, exceeding the company’s roughly $200 million in annual earnings.

The math does not math, even assuming the $200 million earnings figure is not inflated.

Before we get to the restructuring scenarios, let’s talk about PIK, LTV and scale.

The PIK Problem

Throughout this deterioration, BCRED never placed Medallia on non-accrual status. Under BDC accounting rules, a loan goes on non-accrual when collection of interest becomes doubtful.

Here’s more on PIK (plus another good story, Pluralsight):

Medallia was PIK-ing for over two years and the fair value had fallen 22 points, yet