Carlyle Engineers Liquidity; Private Credit Gates Multiply; and CRE Gets a Second Look

🗞️ Sunday digest: private markets insights 3/22

Happy Sunday.

Every other week, we send a quick digest on what’s catching our eye across private markets (the data, the drama, and the stuff LPs should actually care about).

Today’s lineup:

1️⃣ Private equity: AI is coming to private equity, and Carlyle is engineering an exit

2️⃣ Private credit: S&P cuts CCLFX's outlook, a Morgan Stanley fund caps redemptions, and BCRED posts its first monthly loss in three years

3️⃣ Commercial real estate: BREIT records net inflows for the first time since 2022, and the private credit exodus may be sending capital back to real estate

Before we dive in:

Accredited Insight delivers the LP’s perspective on private credit, private equity, and CRE, drawing on hundreds of deals, and thousands of conversations. Paid subscribers gain access to our database of over 40 case studies and articles on everything from evergreen funds to due diligence.

1️⃣ Private Equity

TL;DR:

OpenAI and Anthropic are coming to PE

Carlyle is structuring a multibillion-dollar deal, and it looks like a collateralized fund obligation.

1. OpenAI Wants PE to Be Its Enterprise Sales Force

OpenAI is negotiating a $10 billion joint venture with four private equity firms (TPG as anchor, Advent International, Bain Capital, and Brookfield) to distribute its enterprise AI products across their portfolio companies (Reuters). Equity commitments would be $4 billion.

Anthropic, is allegedly in similar talks with Blackstone, Permira, and Hellman & Friedman. (Bloomberg).

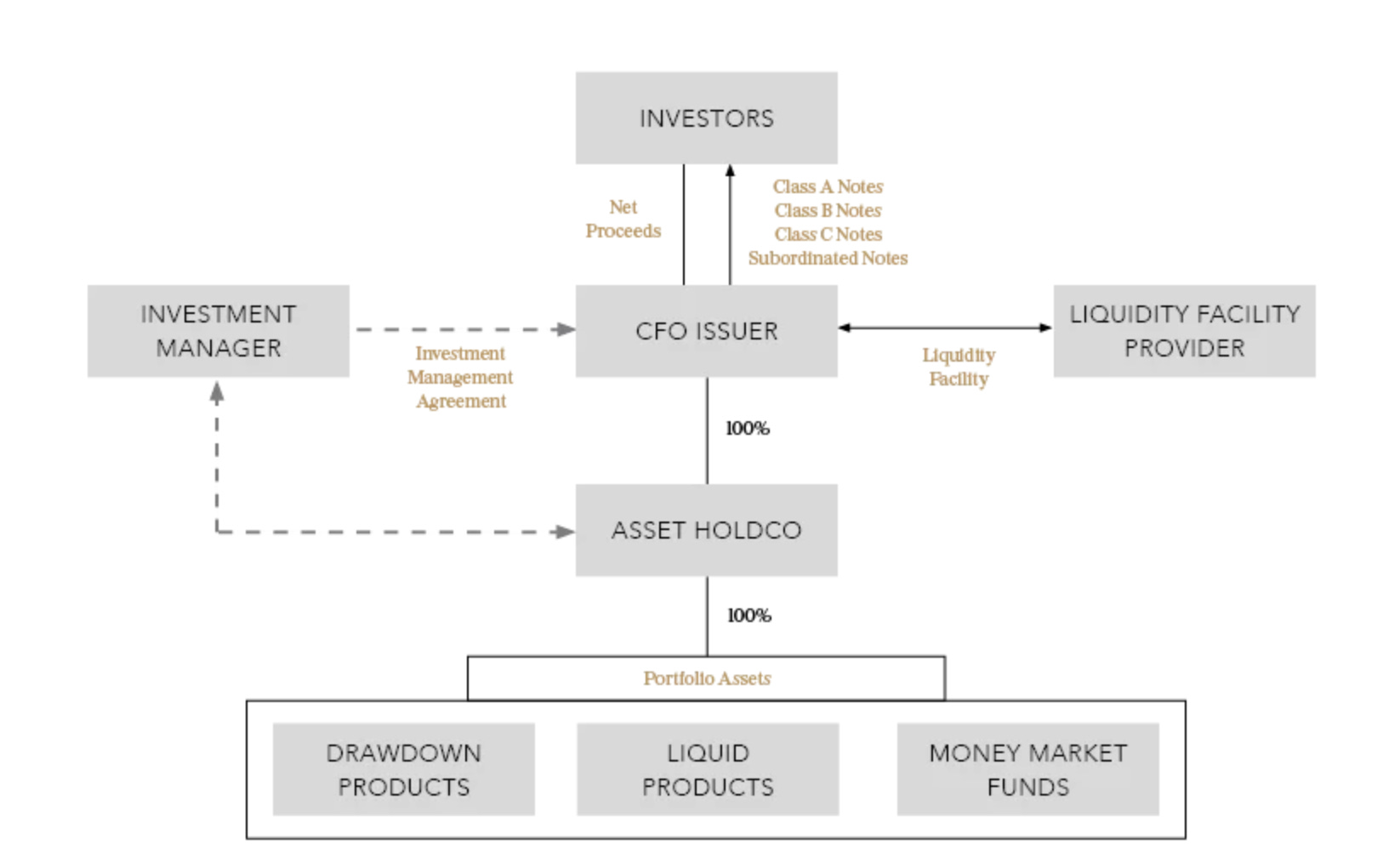

Carlyle’s Answer to the Exit Drought via CFO

Carlyle is building what could be the largest collateralized fund obligation-style transaction on record (Bloomberg). The deal would seed Carlyle Partners IX, while simultaneously paying back investors in older funds.

The mechanics: investors in prior funds transfer their holdings into a new vehicle that provides them with equity and some cash. That vehicle then invests in the new fund.

Here’s a sample CFO structure from Mayer Brown:

The financing combines senior debt, preferred shares, and common equity, with Carlyle retaining a significant minority equity stake.

A few unusual features: no credit rating (atypical for structures that need to attract insurance capital), large amounts of preferred shares (atypical for CFOs), and it’s being structured by AlpInvest, Carlyle’s own secondaries platform. What are the odds this will make its way to some secondaries evergreen funds?

➡️ When GPs start building their own structured products to manufacture liquidity, you know the exit backlog is a problem. Co-President John Redett acknowledged that the seventh flagship fund was “not our best work of art,” though distributions have improved. The eighth fund is 80% committed and invested. Project Potomac will hold stakes in both.

👉 Invest in PE? Read this:

2️⃣ Private Credit

TL;DR:

S&P cuts CCLFX’s outlook to negative after record 14% redemption requests

Morgan Stanley’s North Haven fund capped at 5%, returning less than half of what investors requested

BCRED posts its first monthly loss since September 2022

1. S&P Cuts Cliffwater’s Outlook

What a change in two weeks: in the last issue, we flagged CCLFX’s repurchase deadline as the one to watch. Since then: investors submitted redemption requests of ~14% of shares (a record for the fund).

Cliffwater capped repurchases at 7% (the max without changing fund terms), meaning roughly half of investors who wanted out didn’t get out. For more, read this:

S&P affirmed the A rating but revised the outlook to negative (link), citing the risk that elevated redemptions and above-minimum repurchases could become the norm.

Separately (or maybe relatedly?), CCLFX was also reportedly in the secondary market looking to sell approximately $1 billion in loan assets from the fund (PitchBook).

2. Morgan Stanley Joins the Club

Morgan Stanley’s $7.6 billion North Haven Private Income Fund received redemption requests totaling approximately 10.9% of shares in Q1 2026.

The fund enforced its 5% quarterly cap, returning roughly $169 million, or ~45.8% of what investors asked for (Reuters and Morningstar).

👉 Need to understand how gating actually works?

3. BCRED’s First Monthly Loss in Three Years

Blackstone’s $83 billion BCRED posted a -0.4% total return in February, its first monthly decline since September 2022 (FT). Performance is flat year-to-date after an 8% gain in 2025.

The fund “wrote down the value of a “select” number of loans during the month, including the debt it extended to customer service software company Medallia”, reported FT.

Meanwhile, Q1 redemption requests hit approximately $3.7 billion (~8% of assets). Blackstone upsized its repurchase offer and put in $400 million of its own capital (including $150M from employees) to cover the gap

Before we move on: both CCLFX and BCRED use sale/buyback agreements. Worth understanding if you’re trying to make sense of how these funds manage liquidity.

3️⃣ Commercial Real Estate

TL;DR:

BREIT records net inflows for the first time since 2022

Capital may be rotating from private credit into CRE

CRE debt markets are funded but selective

1. BREIT is Back, baby!

Blackstone’s $55 billion BREIT raised $1 billion more than it paid out in redemptions in 2025 - first net inflows since September 2022 (Bisnow). The fund’s net return on I Shares was over 8% last year.

➡️ This is interesting: BREIT is offering 1% bonus shares (funded by Blackstone, non-dilutive to existing holders) for new subscriptions through April 1.

2. The Private Credit → CRE Rotation

Here’s another interesting tidbit: as capital exits private credit funds, some of it appears to be flowing back into real estate.

Non-traded REIT capital formation went from $33.2 billion in 2022 to $5.7 billion in 2025, but recent months suggest a reversal. BREIT’s February net inflows (the first positive month in nearly four years) are one data point. As Willy Walker (CEO of Walker & Dunlop) put it: private credit funds dwarf CRE debt funds (trillions versus billions) so even a modest rotation could have a material impact on CRE capital flows (CNBC).

👉 Real estate people, you are going to love this icymi:

P.S. New here?

After 2 years of publishing, we got around to creating a table of contents 😅:

Thanks for reading! As always, if you have any suggestions, reply to this email, leave a comment, or find me on socials (unhinged me on X, or come troll me - intelligently - on LinkedIn)

-Leyla

Leyla is the best source for the illiquid stuff for those who don't understand!