Software Isn’t Dead, PIK Is Fine, and the Best-Performing Cities

🗞️ Sunday digest: private markets insights 5/3

Happy Sunday!

Every other week, we send a quick digest on what’s catching our eye across private markets (a pulse, if you will).

Today’s lineup:

1️⃣ Private equity: AI infrastructure is hot, software isn’t dead, and regulators are eyeing PE in law firms

2️⃣ Private credit: PIK is fine, banks are fine, probability of defaults is fine (I’d add the dog meme, but this email is too long as is)

3️⃣ Commercial real estate: did your market make it on the best cities list?

Before we dive in:

Accredited Insight delivers the LP’s perspective on private credit, private equity, and CRE, drawing on hundreds of deals, and thousands of conversations. Paid subscribers gain access to our database of over 40 case studies and articles on everything from evergreen funds to due diligence.

1️⃣ Private Equity

1. From KPMG’s Q1 Pulse on Private Equity:

Infrastructure (particularly AI-adjacent/energy infrastructure) is the hottest theme in PE right now. The largest deal? The $41B take-private of AES, a clean energy company.

And yes, retail is getting access to infrastructure too. Here’s an evergreen infra fund deep dive:

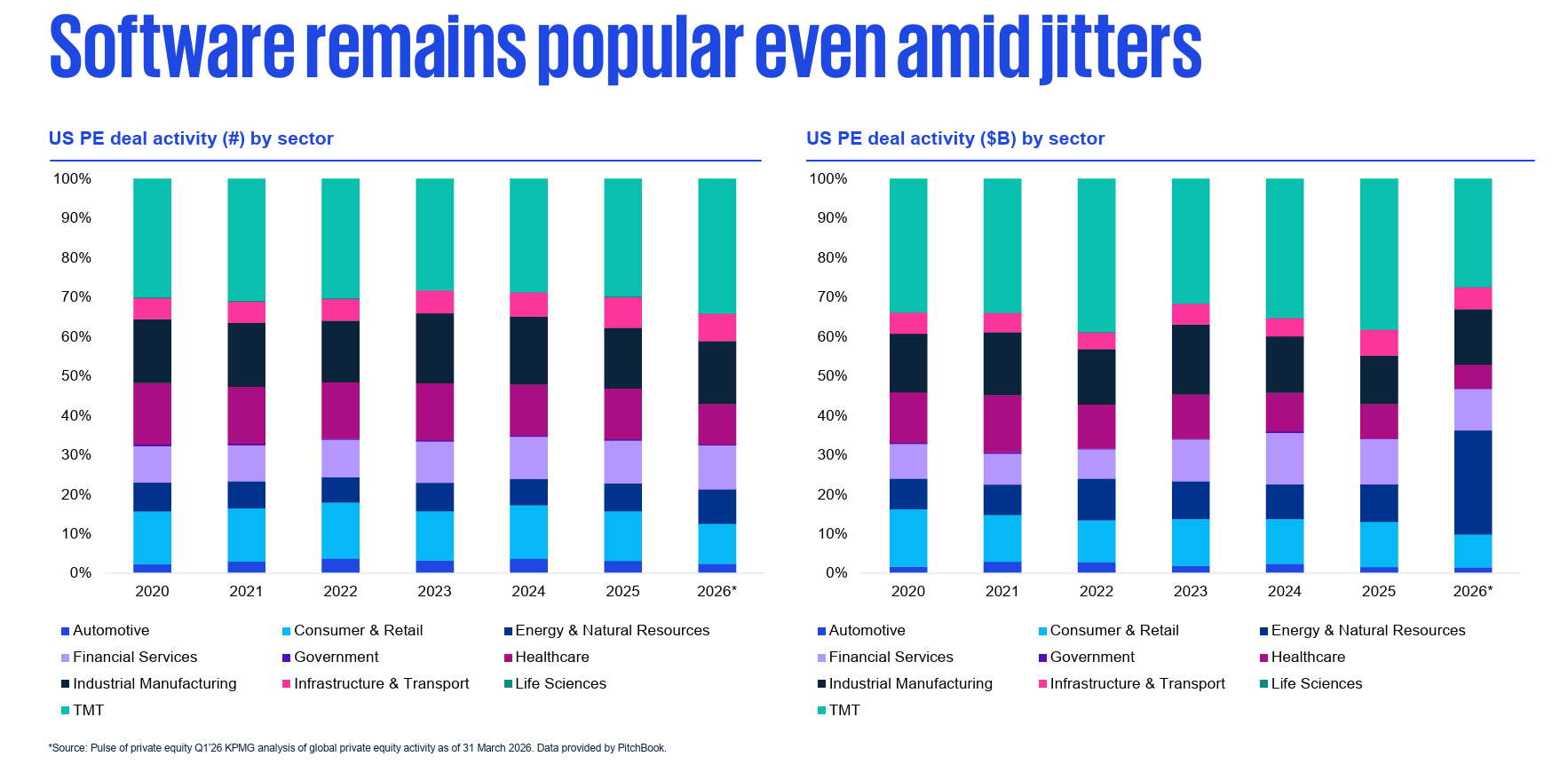

That said, software isn’t dead. Despite all the AI disruption noise, TMT (tech/media/telecom) still led PE investment in Q1, with $62B deployed. This is the largest sector allocation in the U.S:

2. PE ate accounting firms

Since 2021, PE funds have taken ownership of ~24 of the top 100 US accounting firms. Now, those assets are starting to trade.

The first “flip” happened in January 2025 when Citrin Cooperman changed hands from New Mountain Capital to Blackstone (at 15x EBITDA, up from the 11x New Mountain paid). More are expected.

The second wave of buyers is running into a problem: the easy value creation is already gone (tech upgrades, roll-ups, margin expansion). What’s left is operational grind.

Every PE manager claims they add operational value. Here’s how to tell which ones actually do it:

3. PE wants to eat law firms, too

Several states are moving to block the workaround MSO (Management Services Organizations) structure that allows PE to invest in law firm economics without owning the practice (WSJ):

California (AB 2917): bans non-attorney control

Illinois (HB 5670): bans fee/profit-linked arrangements entirely

The opposition zeros in on professional ethics: conflicts of interest (where investors may prioritize profit over client outcomes), threats to lawyer independence, and risks to client confidentiality.

Net effect: early accounting firm acquisitions have been successful (for PE firms). But the universe of professional services industries to acquire might be shrinking.

That said, incentives are strong, minds are sharp and money is flowing in. I expect the industry to keep finding new loopholes angles.

2️⃣ Private Credit

Goldman Sachs’ latest view on private credit is essentially: relax, but don’t get comfortable.

On that note: here’s a comparison of Goldman Sachs’ non-traded and listed BDCs:

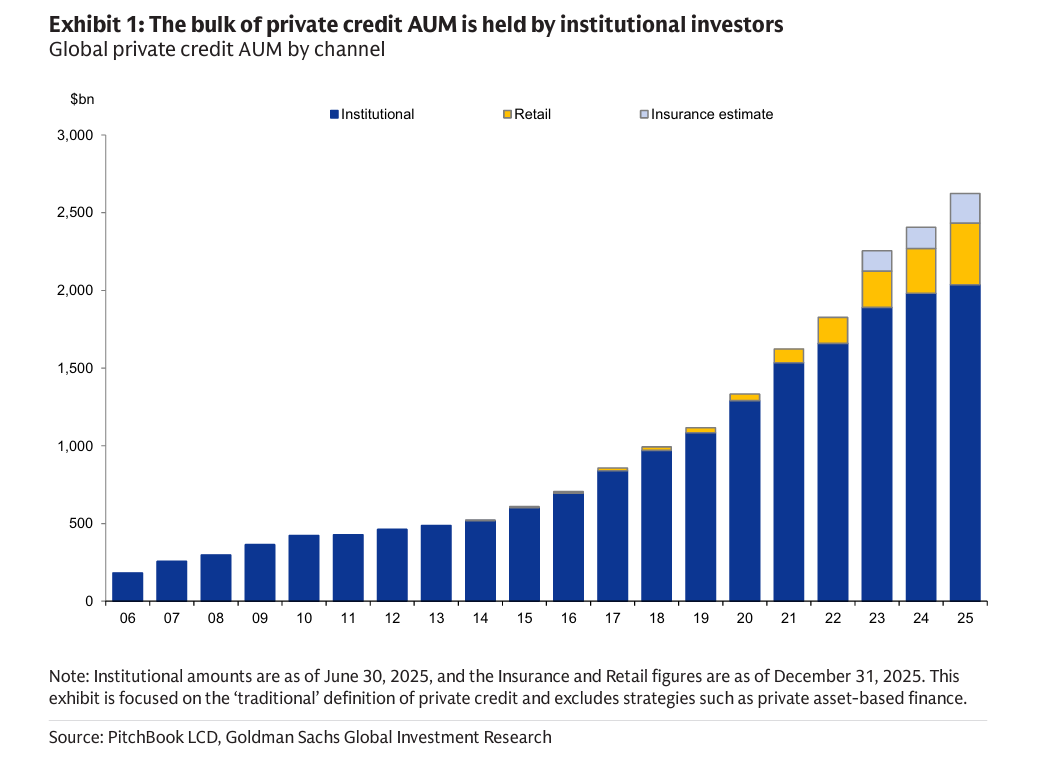

Yes, there has been recent volatility (especially in retail-focused BDCs), but GS frames it as noise at the margin of a much larger market. Institutional investors still hold the lion's share of private credit AUM, though retail and insurance capital drove most of the growth over the past three years:

Worth noting: most retail money sits in semi-liquid evergreen funds (with quarterly redemption windows), while institutional capital is locked up in traditional drawdown structures.

If the retail influx slows, it's unclear where the next leg of growth comes from.

👉 Here’s how liquidity in semi-liquid funds works:

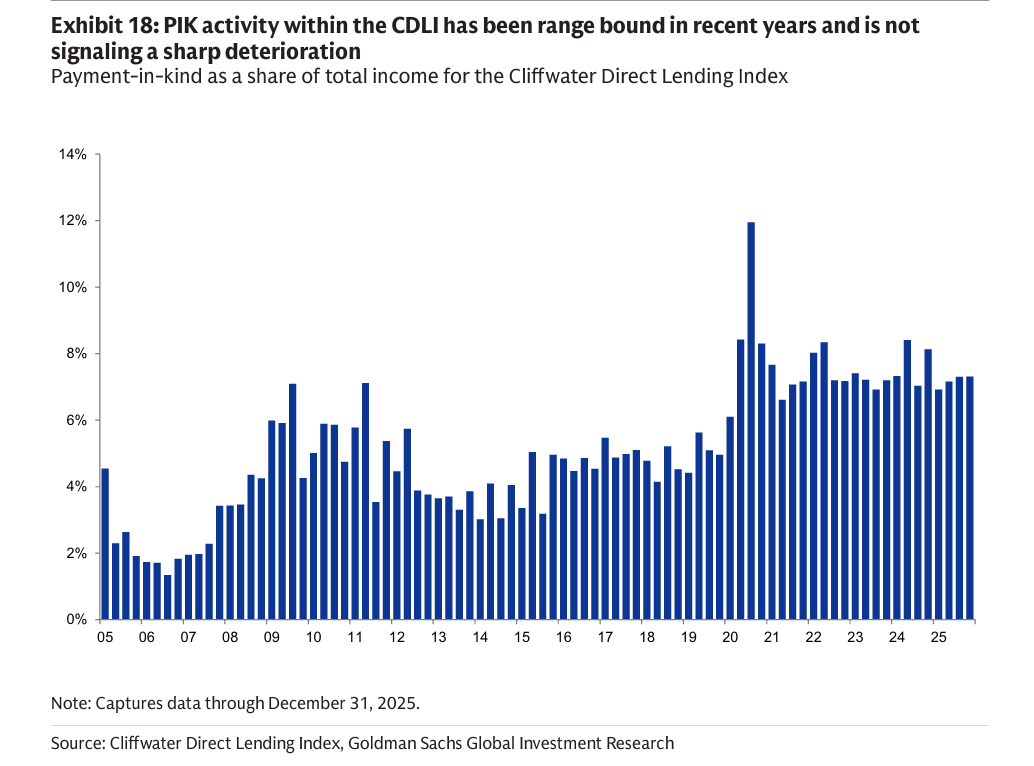

So far, fundamentals are holding:

Realized losses: 64bps (vs. ~100bps historical avg)

PIK income: elevated, but not spiking

Non-accruals: stable

Goldman's conclusion: no systemic risk, and experienced managers with dry powder are well-positioned if dislocations emerge in syndicated markets.

But the margin for error is thin.

Moody’s baseline forecast projects GDP growth of ~1.5% (right at the threshold where defaults typically accelerate).

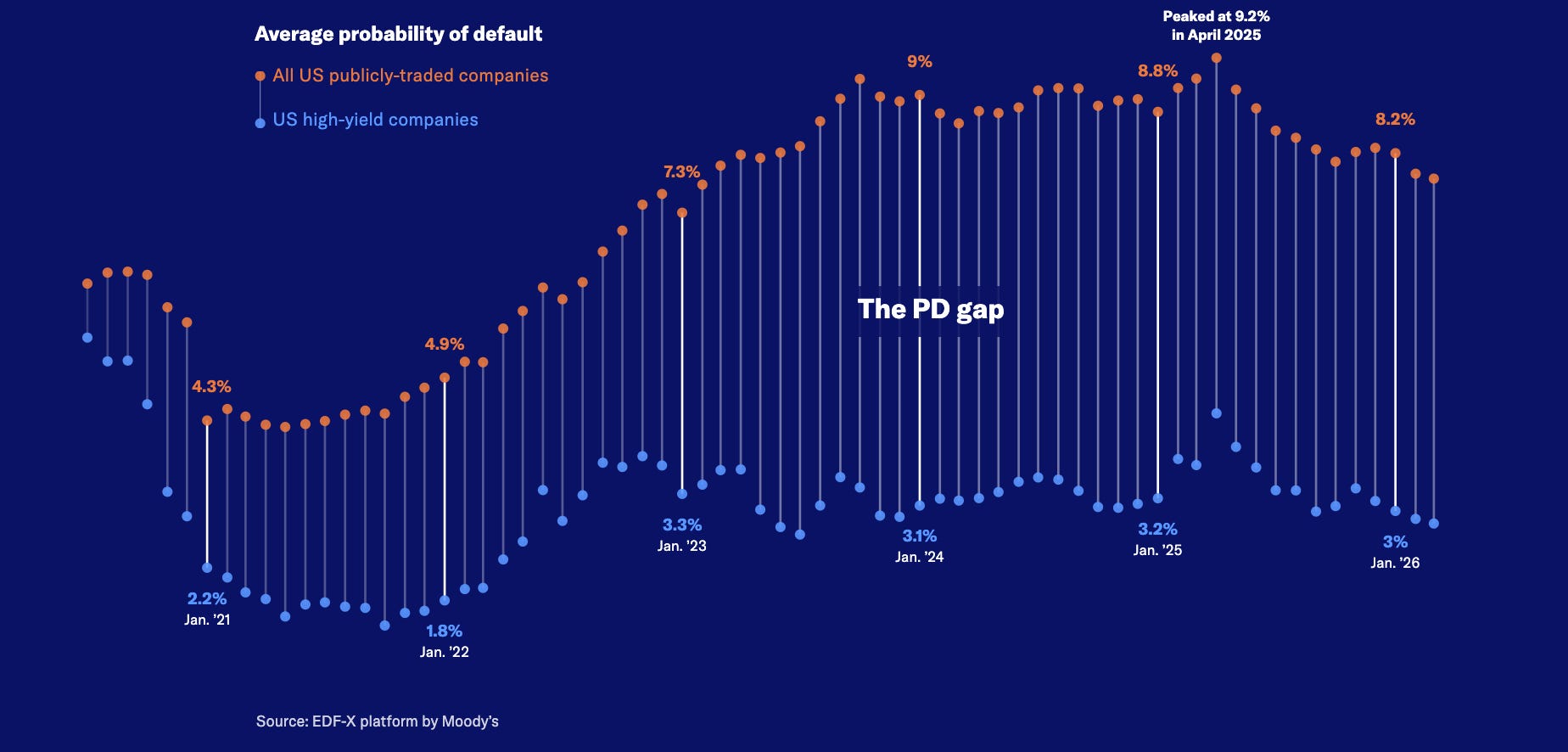

The chart below shows the average probability of default (PD) for all U.S. listed companies at 7.9% as of March 2026, compared to 3.2% for high-yield companies:

Why the gap between all US and high-yield?

High-yield companies refinanced at low rates during 2020-21, and size helps: the median high-yield company is roughly 11x larger than the median firm in the all-US portfolio. These companies have better access to capital markets.

Smaller, non-rated borrowers (the bread and butter of private credit) don't have that cushion.

From Moody’s (emphasis mine): "Corporate lending AUM will exceed $2 trillion in 2026 and approach $4 trillion by 2030... Growth brings complexity: covenant erosion, the proliferation of PIK features, NAV lending, and back-leverage structures are introducing layers of structural opacity that can mask true leverage levels."

Also worth noting: 44% of 2025 non-accruals are coming from 2021–2022 vintages (the ultra-low rate era). Loans originated in the easy-money era are starting to show cracks.

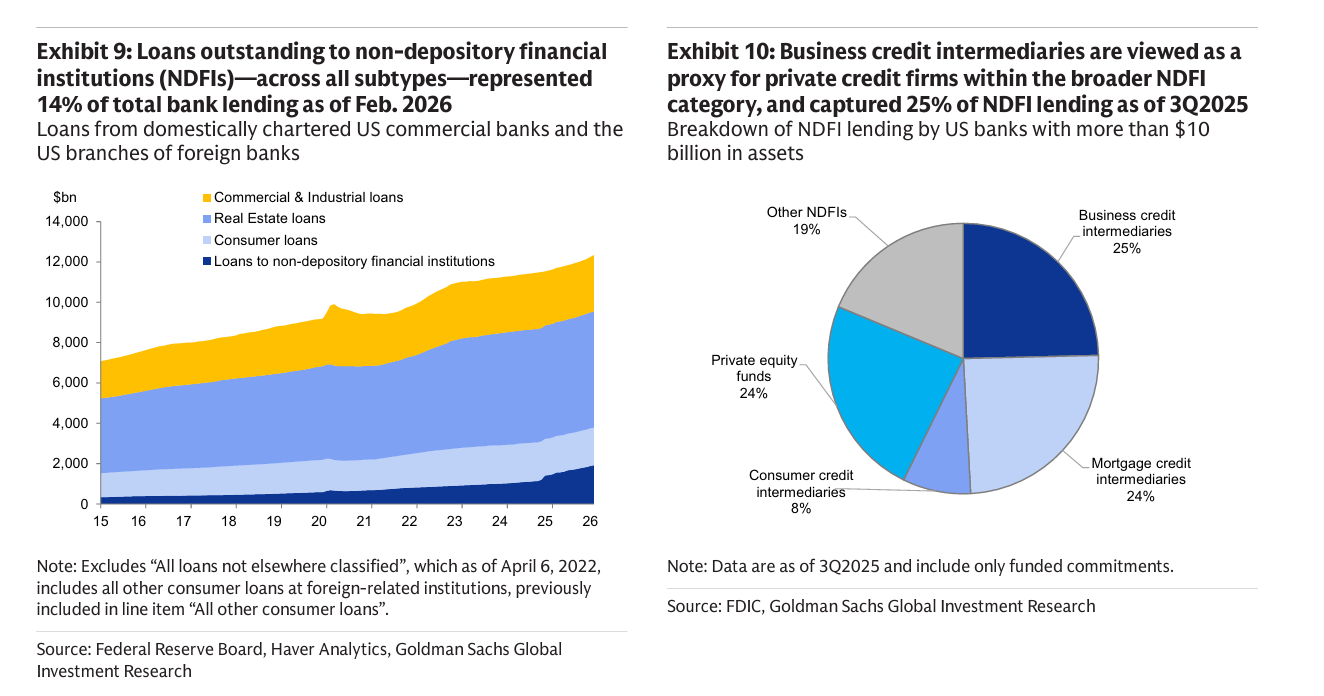

One last data point: loans to non-depository financial institutions (NDFIs, which includes private credit funds) represent only 14% of total bank lending. So concerns around bank exposure to private credit, while worth monitoring, aren't yet at systemic levels.

3️⃣ Commercial Real Estate

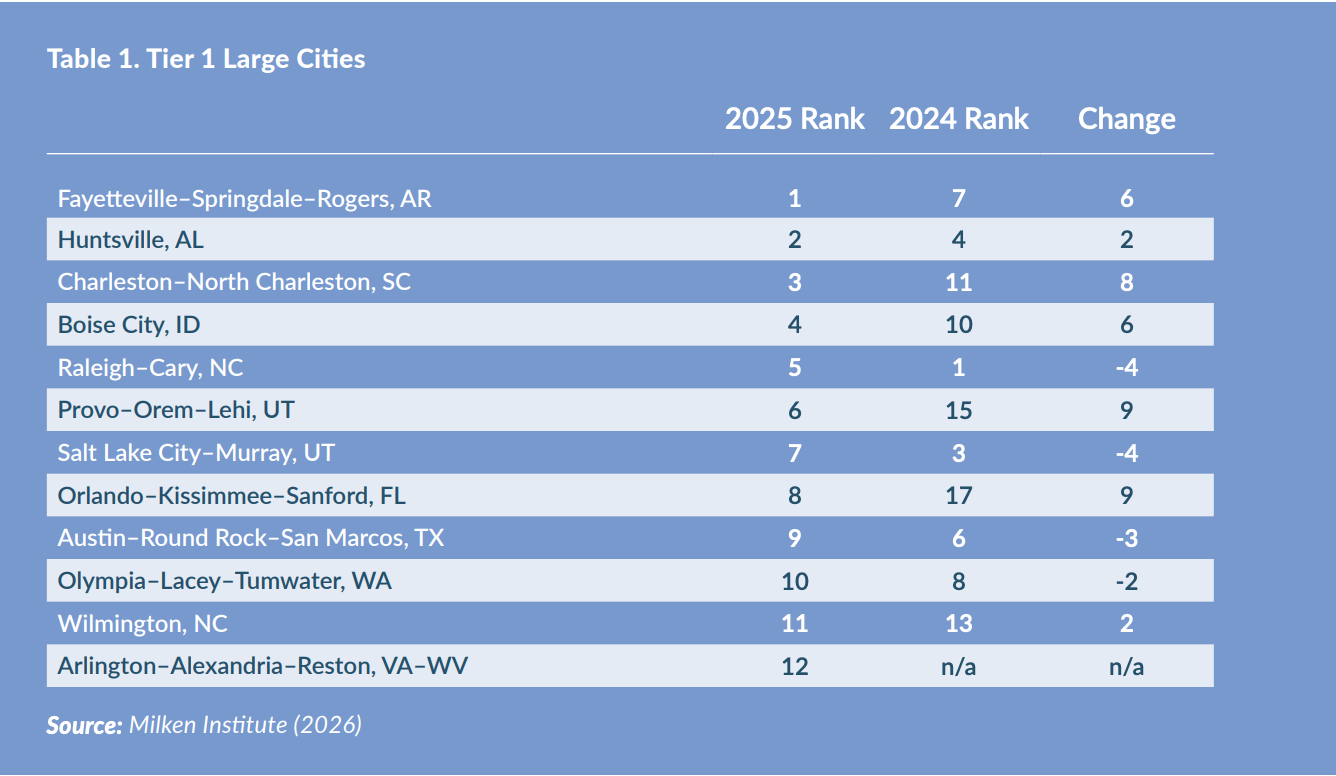

1. Milken Institute’s Best Performing Cities report is excellent

Idaho Falls, Boise, and Punta Gorda led the nation in job growth from 2019–2024.

Here’s the list of top large cities across all metrics (the report goes into detail on each one - it’s free, you just need to create an account).

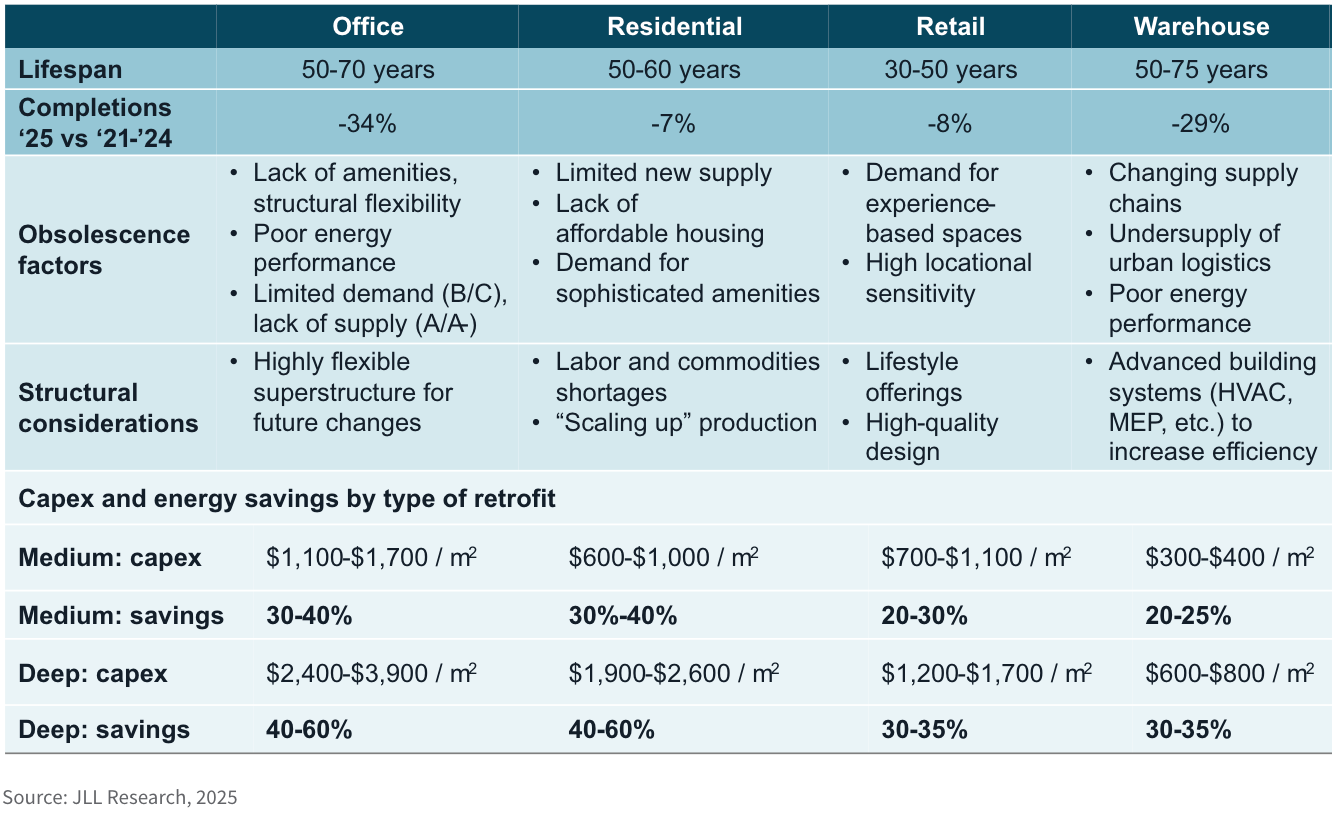

2. JLL published an interesting article on repositioning of obsolete assets and portfolios.

Most buildings standing today will still be around in 2050, so obsolescence is becoming a major risk.

Assets are falling behind across design, location, and regulation (especially energy standards).

Retrofitting can cut energy costs by up to 60% and boost rents, often at a discount to redevelopment.

Lastly, I presented at the Passive Pockets Summit on using AI for real estate due diligence. If you missed it, I’ve updated my original post (originally written in the dark ages of 2024) with best practices and five prompts for evaluating multifamily deals. You can find it here:

P.S. New here?

Here’s where you’ll find the full archive (somewhat organized):

As always, if you have any suggestions, reply to this email, leave a comment, or find me on socials (unhinged on X, and a slightly more filtered on LinkedIn)

-Leyla

Key context from regulators:

NDFI loans outstanding rose from $56 billion in Q1 2010 to $1.32 trillion in Q3 2025. NDFI lending as a share of bank lending grew from less than 1% of total loans to 10.0%, and now accounts for more than a third of lending to businesses not secured by real estate. FDIC

From 2010 to 2024, outstanding balances of bank loans to NDFIs rose at a compound annual growth rate of 21.9 percent — almost three times as high as the next-fastest-growing segment. FDIC

Lending to nonbank financial institutions accounted for about 40% of bank loan growth in 2025, though the category only represents about 13% of total bank loans. American Banker

Important caveat on 2024 data: The largest portfolio increases in Q4 2024 were reported in "all other" loans and loans to non-depository financial institutions, largely due to reclassifications following the finalization of changes to how certain loan products should be reported.

Reclassifications also likely caused declines in other loan categories from which the loans were reclassified, particularly C&I and "other" consumer loans. This means the 2024 jump in NDFI share is partly a reporting change, not purely organic growth. FDIC

Banks with assets greater than $100 billion held about 86% of total industry loans to NDFIs as of Q3 2025, and ten of those institutions held about 71% of total loans to NDFIs. FDIC

The trend is unmistakable: NDFI lending has grown from a negligible slice of bank portfolios to a significant and closely-watched category, driven largely by the largest U.S. banks funding private credit funds, mortgage originators, insurance companies, and other shadow banking entities.

That’s priced like “fine” means stable. The variable is how leverage behaves when growth slows.