The Discount Capture Machine: Inside Coller’s PE Secondaries Fund (C-SPEF)

The early years of evergreen secondaries can look extraordinary, this is a look inside one

There’s a fairly straightforward way many secondaries funds generate returns in the early days:

Buy private equity stakes below reported NAV

Mark them back to NAV

Book the spread as unrealized appreciation.

📣 Before you gallop off to read the riveting details of today’s case study, quick announcement: I’m doing a live webinar with Kunal Kapoor, the CEO of Morningstar at 9:30 am PT/12:30 ET today. Register below if you’d like to join us.

👉 You can see the mechanics here:

As long as sellers need liquidity and buyers can acquire interests below reported NAV, the model can produce very attractive early-stage returns.

And historically, it has.

None of this is investment advice, obviously. But every once in a while, private market fund structures, incentives, and accounting mechanics come together in a holy union. Early-stage evergreen secondaries funds are one example.

Notice the early-stage part.

Like any union, as these funds scale, problems eventually emerge (in our case, it’s due to the denominator effect, stay tuned for Part 2 of UNREAL gains).

Anywho. I wanted to do a case study on an early-stage secondaries vehicle while the machine is still operating at full speed. Which brings us to Coller Secondaries Private Equity Opportunities Fund (“C-SPEF”).

Here’s another fund that operates at full speed:

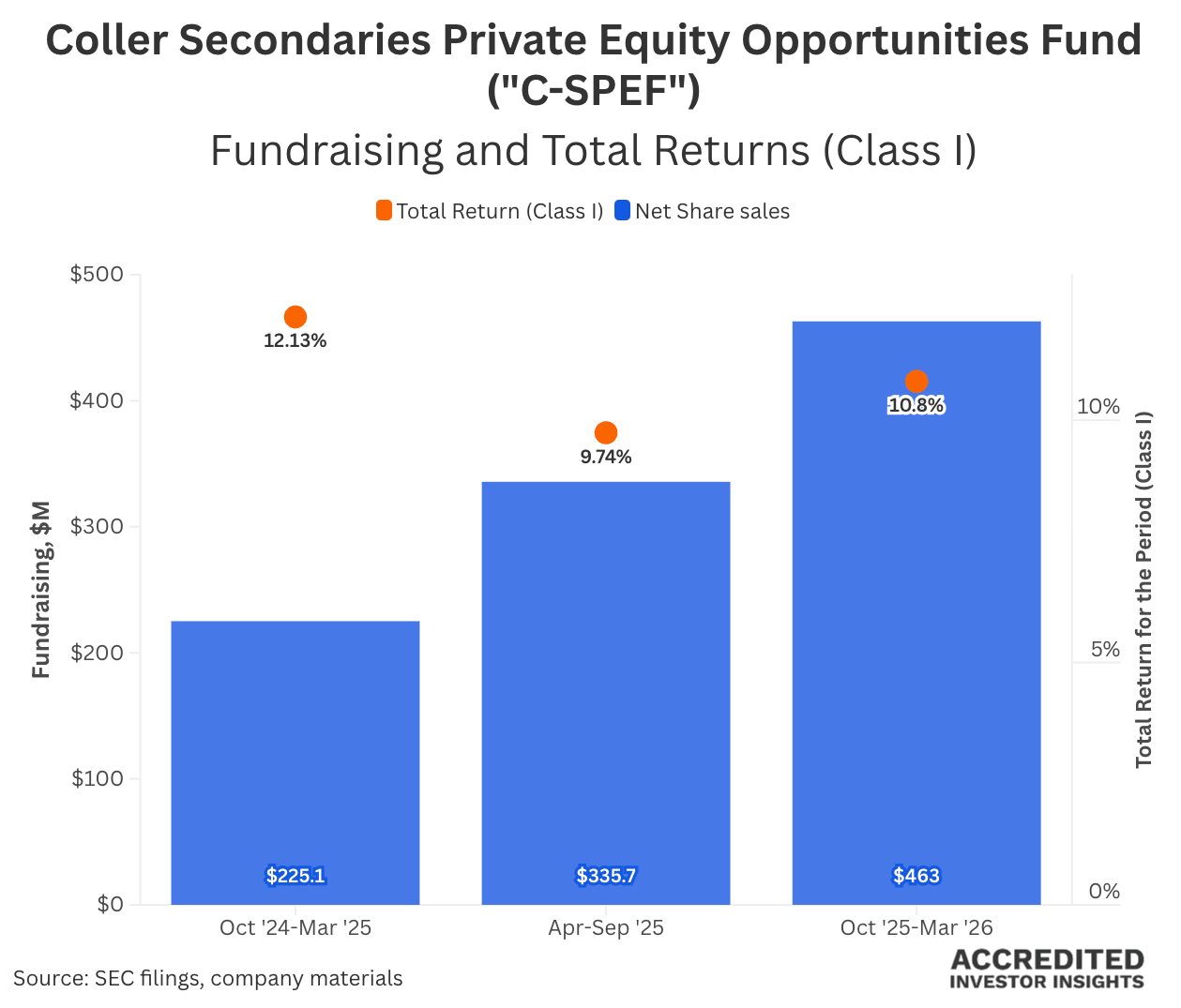

The fund has grown from roughly $323 million at launch in April 2024 to ~$1.44 billion by March 2026 while reporting annualized returns approaching 17%.

More interestingly, management essentially explained the entire strategy themselves in one sentence, right in the SEC filings:

Today we’ll take a look at:

The usual: how it works, where returns come from

The less usual: the investor-friendly fee structure

And finally: two very different ways this story could end

Disclosure: This case study is provided for educational and informational purposes only and should not be construed as investment, legal, tax, or financial advice. The views expressed are solely those of the author. All examples are illustrative in nature and not guarantees of future outcomes. Readers should conduct their own independent research and consult with qualified professionals before making any investment or financial decisions.

The Pitch

This evergreen tender-offer fund launched in April 2024 and scaled to roughly $1.44 billion in NAV within two years.

Coller Capital, of course, is one of the OGs in the asset class. Founded in 1990, the firm manages approximately $54 billion across secondaries and other private market strategies (it was acquired by EQT earlier this year).

Here’s a deep dive on their private credit secondaries vehicle:

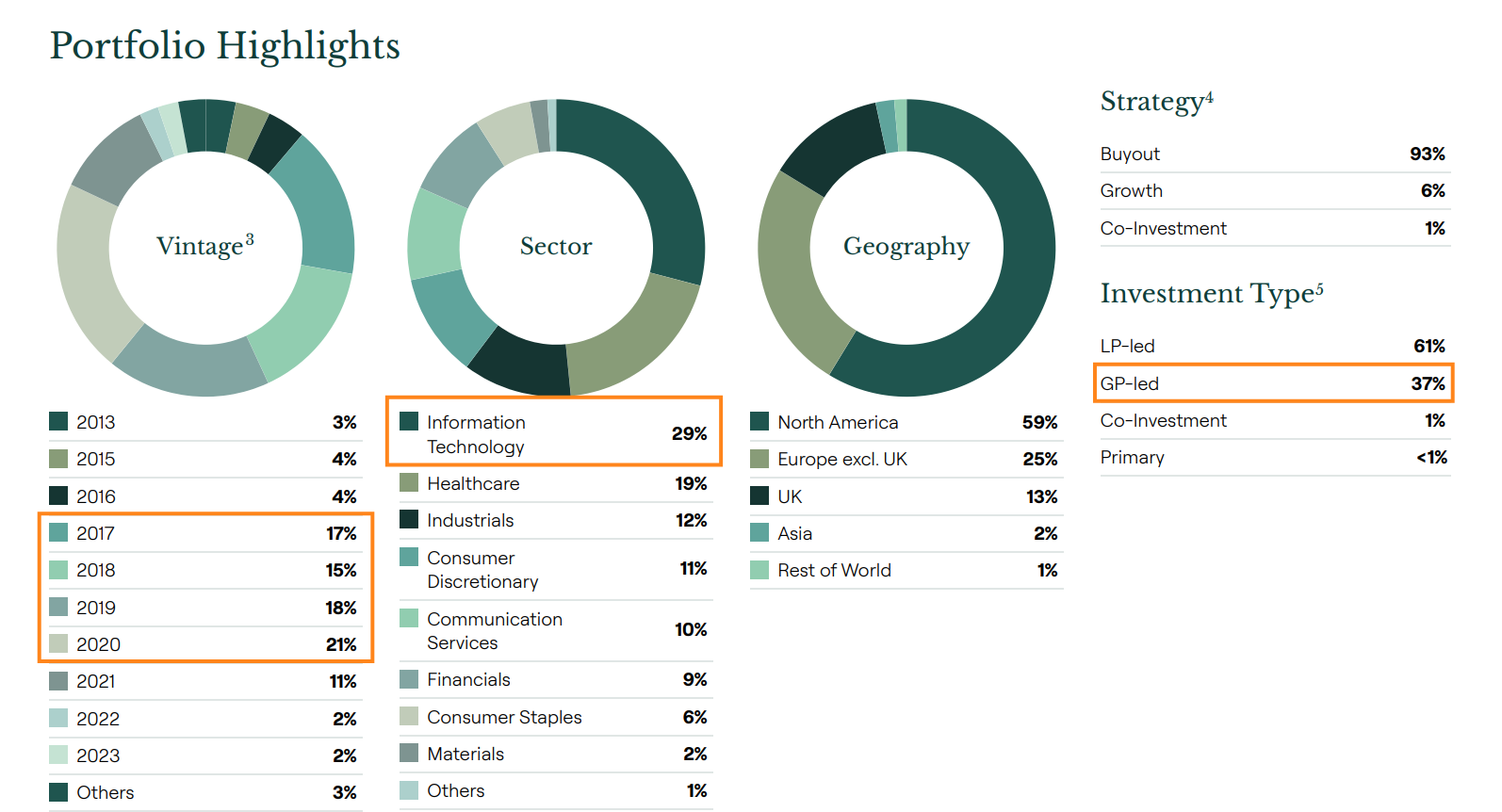

Under the hood, C-SPEF is a fairly diversified secondaries vehicle:

171 underlying fund positions

82 distinct GPs

nearly 1,500 underlying portfolio companies

At launch, the portfolio was overwhelmingly traditional LP-led secondaries exposure. That changed quickly.