When the Music Stops

Why Private Credit Evergreens Can Handle Redemptions (And Private Equity Can't)

The duration mismatch between assets and liabilities is a well-documented problem. Banks are the most obvious example, but evergreen funds are not insulated from the same risk.

And yes, the 5% redemption caps in semi-liquid funds are in place to protect capital by avoiding fire sales. But we’ve already seen examples where the redemption queue does not clear after a few quarters, and forces the manager’s hand. Remember Bluerock?

Today, I’ll make the case for why private credit is not going to be the undoing of evergreen structures. And why private equity (where redemptions are currently running low) might be.

The Big Picture

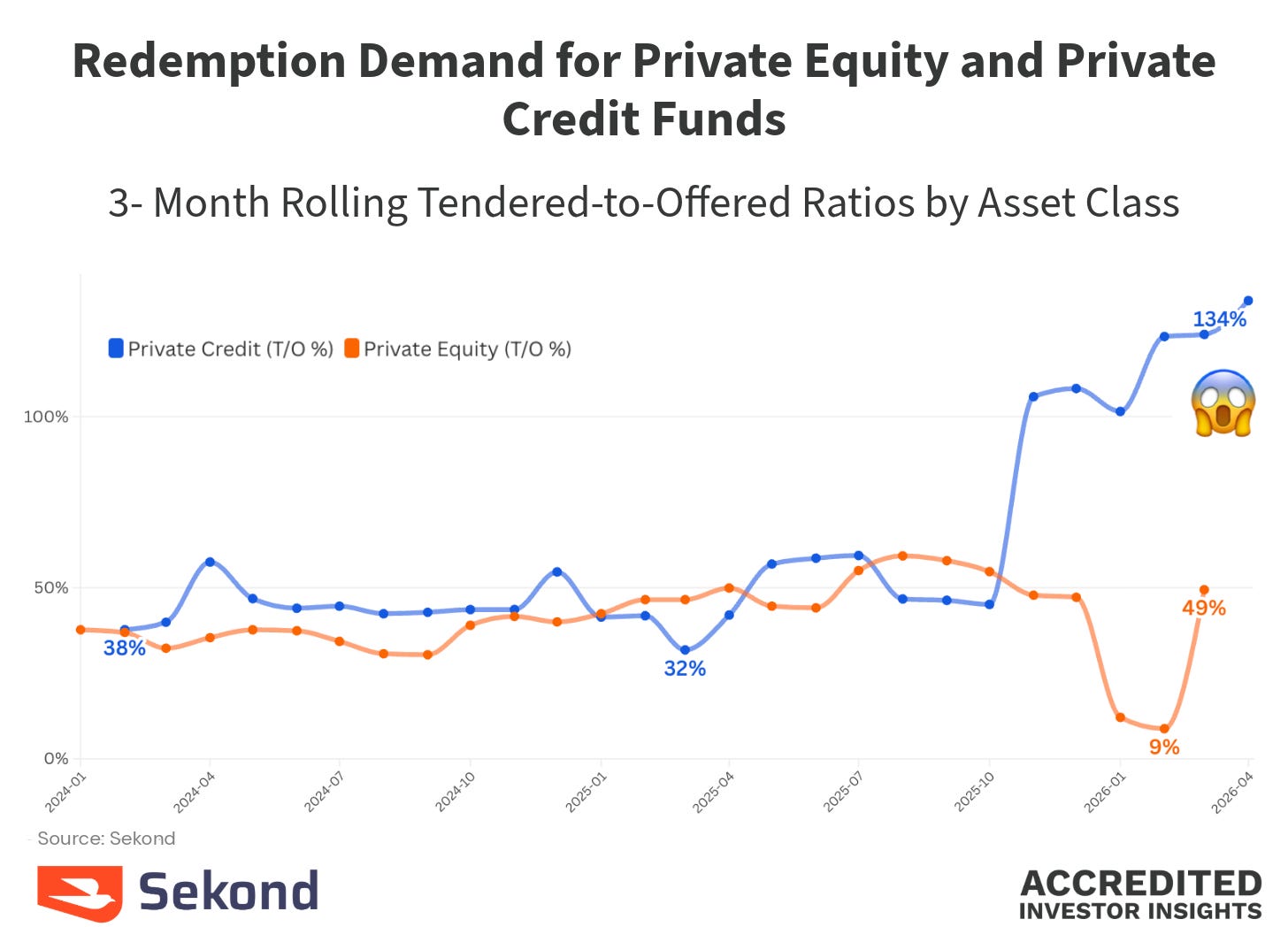

The redemption headlines center on evergreen private credit funds. Requests are up across the board, with many managers capping outflows per their prospectus provisions.

👉 Everything you wanted to know about gating provisions across different fund structures:

What's interesting: private credit funds are experiencing redemption pressure. Private equity funds? Not so much.

Side note: You access Sekond’s redemption tracker (LINK). It’s free with a Sekond account. And no, I’m not paid to promote it, I just really like data.

Why Private Credit Can Handle This

I recently attended an event where Mark Rowan of Apollo was presenting. His take on evergreen private credit funds was blunt: it would take a very incapable manager to fail to meet the 5% quarterly redemption cap.

I wholeheartedly agree. And the data proves it.

I pulled financial statements for four of the largest private credit evergreen funds: Blackstone Private Credit (BCRED), Cliffwater Corporate Lending, Blue Owl Credit Income, and HPS Corporate Lending.

I then compared them to four large evergreen PE funds: Partners Group PE, Blackstone Private Equity Strategies, KKR Private Equity Conglomerate, and AMG Pantheon.

Here’s what embedded liquidity actually looks like: