What Will Liquidity Cost You When Barbarians Shut the Gates?

A deep dive into OBDC II’s tender offer and what investors actually pay for liquidity.

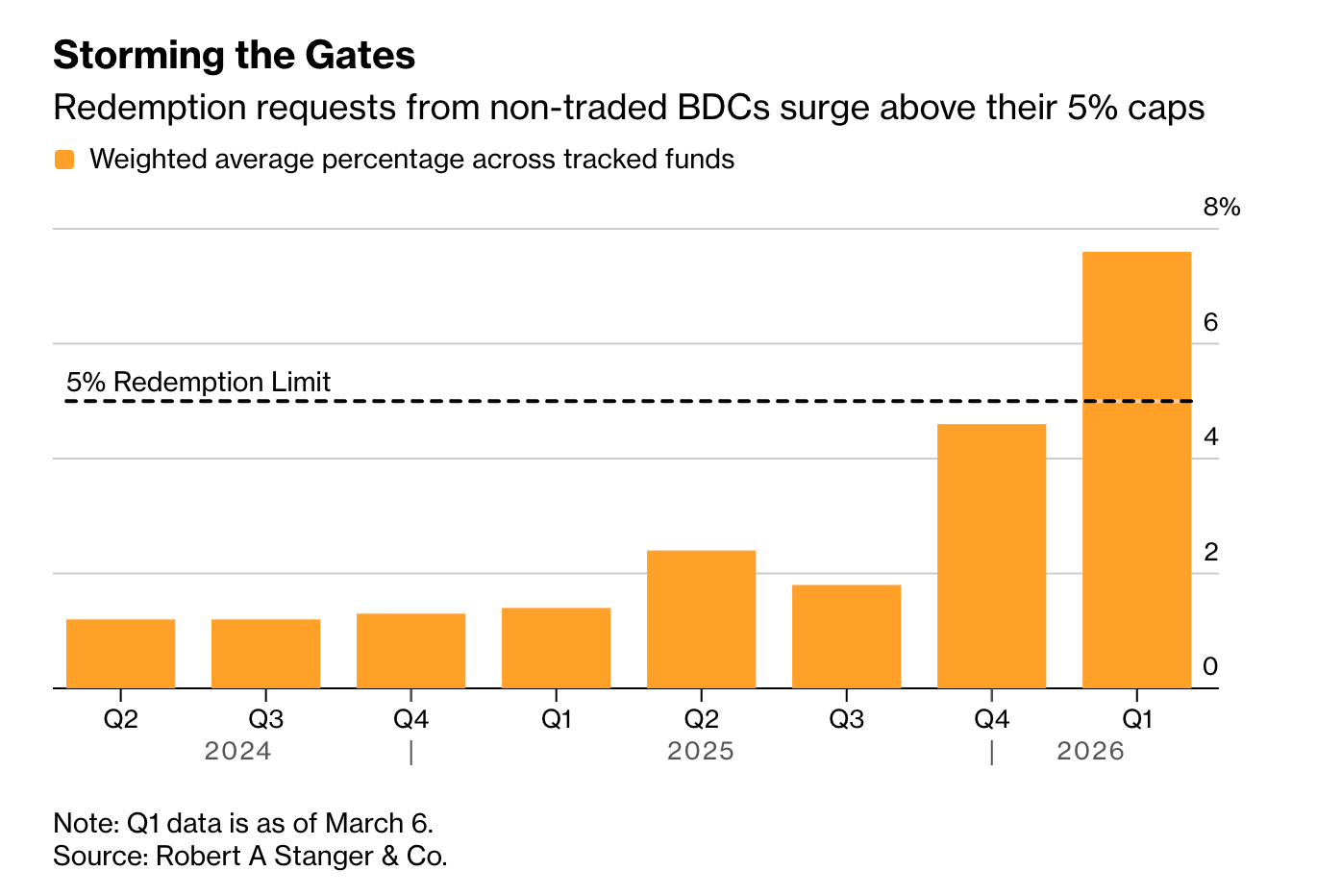

Do you hear the herd?

Investors are starting to gallop out of evergreen private credit funds. Several large vehicles have recently bumped up against their redemption limits.

HLEND gated redemptions (after receiving requests equal to 9.3% of NAV)

BCRED saw redemption requests exceed 7% of NAV (though it met them)

CCLFX capped redemptions at 7% (after investors sought to redeem ~14% of shares)

Speaking of CCLFX, stay tuned for an update on that fund, meanwhile, read this:

Evergreen structures were designed to solve a real problem: how to package inherently illiquid assets into a format that feels accessible to a retired dentist in Oklahoma. The industry solution came with a convenient label: “semi-liquid.”

Now I can hear the argument forming inside your head: “Investors were explicitly told these funds limit liquidity.”

Technically, that’s true.

I’d be curious how many investors (and advisers) actually understood gating provisions before hitting one. If that sounds fuzzy, here’s a quick primer:

For years, while markets were cooperative, gating felt like a theoretical risk reserved for doomsayers. Especially in private credit, where loans amortize and generate steady cash flow. Liquidity almost felt built into the asset class.

Well, those assumptions are about to be tested.

What options do investors have once gates close?

⚰️ Some funds will prioritize redemptions for deceased investors. But death is a bit of an extreme exit strategy.

Sometimes another path appears: secondary tender offers.

Today, we’ll:

Evaluate the OBDC II portfolio post-sale

Estimate potential outcomes for remaining investors (and what’s in it for the party making the offer)

And answer the key question: what does liquidity actually cost in evergreen private credit funds?

Here’s how you can check financials to assess fund’s liquidity (not to gloat, but the timing was 🤌):

Disclosure: This case study is provided for educational purposes only and does not constitute an offer, solicitation, or recommendation to buy or sell any security or financial instrument. Nothing herein should be construed as legal, tax, investment, or financial advice. All opinions are my own and may change without notice. Readers should perform their own due diligence and consult qualified professionals before making any investment decisions.

What's Going On With OBDC II?

If you missed the prior episodes, here’s a quick recap:

Blue Owl Capital Corporation II (OBDC II) is a non-traded business development company managed by Blue Owl Capital. As of December 31, 2025, the fund had ~$1.6B in total investments at fair value, a NAV of $8.27 per share, and ~114.9 million shares outstanding.

After a cancelled attempt to merge with its publicly traded sibling (OBDC), Blue Owl is winding down the fund. They sold $600M of the fund's best loans, declared a $2.50/share special distribution (about 30% of NAV), and plan to return 50%+ of capital to shareholders over the course of 2026.

Now enter Saba Capital and Cox Capital Partners. On March 6th, they announced a tender offer for OBDC II shares at $3.80 per share for up to 8 million shares (6.9% of outstanding shares in the fund)

The offer price represents a 34.9% discount to the post-distribution NAV of ~$5.84.

Now the fun part, let’s do the math on the remaining portfolio and game-play scenarios for investors: