$1T in PE Zombie Funds, PC Gates Multiply, and CRE Fundraising Bounces Back

🗞️ Sunday digest: private markets insights 4/5

Happy Easter! 🐣

Every other week, we send a quick digest on what’s catching our eye across private markets - a quick rundown of things you need to know.

Today’s lineup:

1️⃣ Private equity: CVs now account for 14% of all PE exits (meanwhile, zombie fund AUM is likely over $1T)

2️⃣ Private credit: Apollo, Ares, and BlackRock all gated the same week. Default rates ticked down in February

3️⃣ Commercial real estate: Core real estate finally turned positive. Fundraising is up 13%. Net cash flows are still going out the door (all true, simultaneously).

Before we dive in:

Accredited Insight delivers the LP’s perspective on private credit, private equity, and CRE, drawing on hundreds of deals, and thousands of conversations. Paid subscribers gain access to our database of over 40 case studies and articles on everything from evergreen funds to due diligence.

1️⃣ Private Equity

TL;DR:

CVs now represent 89% of GP-led secondary volume and 43% of total secondary volume

Zombie funds AUM is likely already at $1T

1. The CV as Exit Strategy

In 2025, CVs represented 89% of all GP-led secondary volume and roughly 14% of all private equity exits, according to CAIA.

As of 2025, nearly 80 percent of the top 100 sponsors by AUM had completed a CV transaction, Jefferies reports. This, folks, is the new exit mechanism.

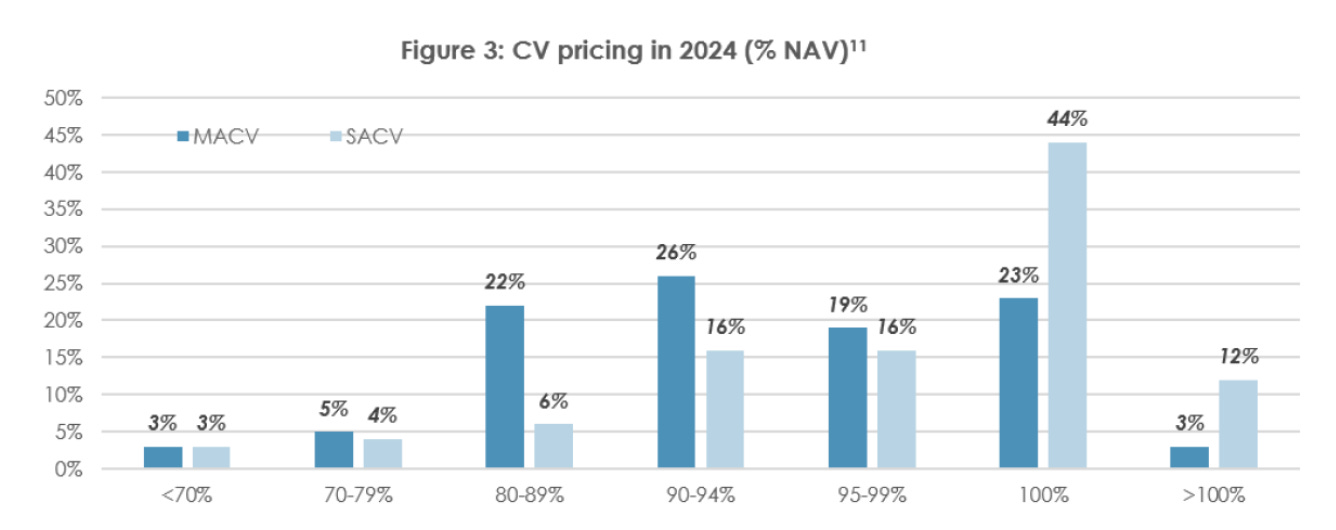

Take a look at the pricing trends in the chart below: (SACV = single-asset CVs, MACV = multi-asset ones). Research shows SACVs (which typically include “trophy” assets) command meaningfully stronger valuations than their multi-asset counterparts.

What you need to know about continuation vehicles:

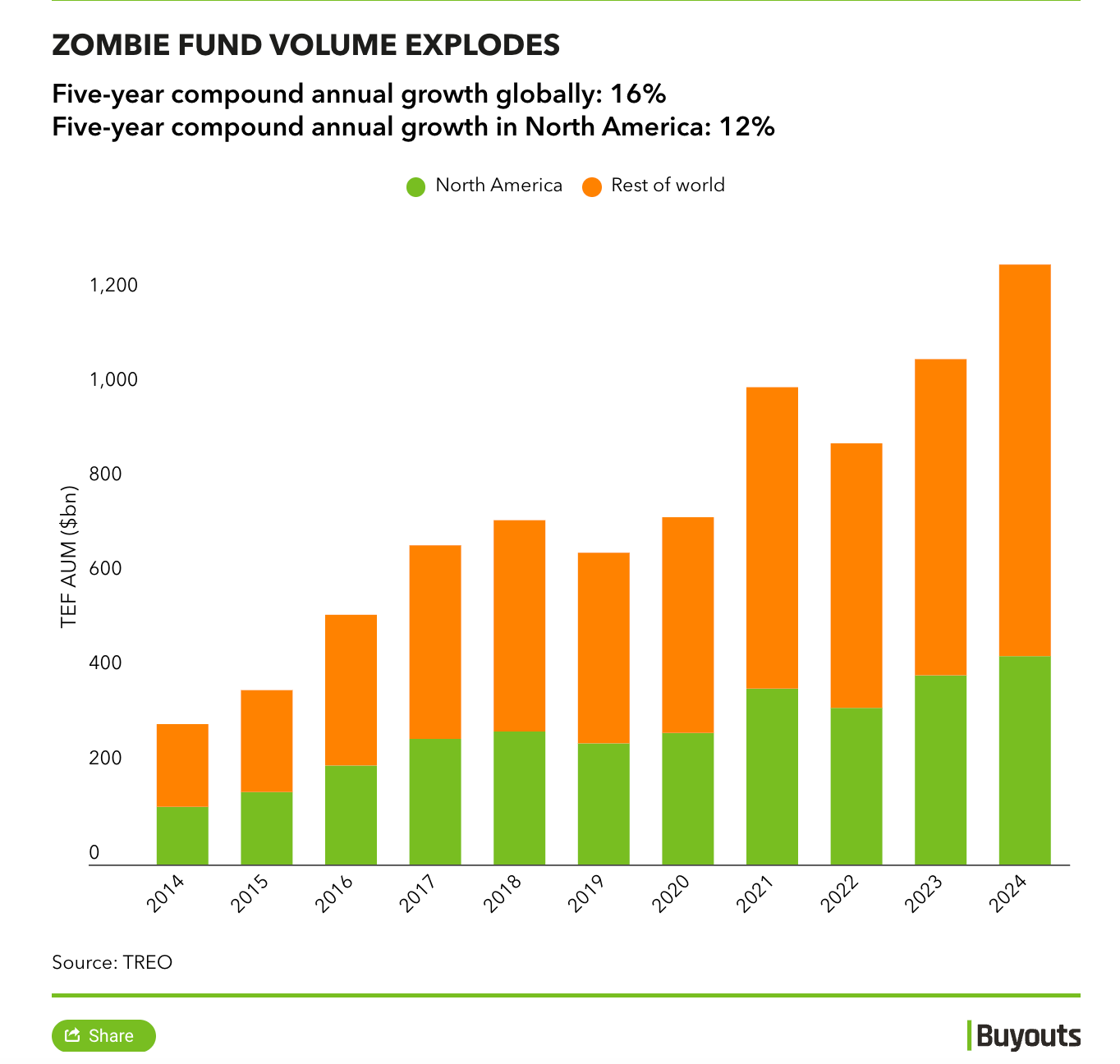

2. The Rise of Zombie Funds

Buyouts wrote on research by TREO Asset Management, which shows that global tail-end fund (TEF) AUM hit $829 billion in 2024, up 24% from 2023's then-record $668 billion. Tail-end funds are at least a decade old (PEI wrote about it here).

For context: TREO's spring 2024 report projected $1 trillion in TEF AUM by 2030. At the current trajectory, they're likely already there.

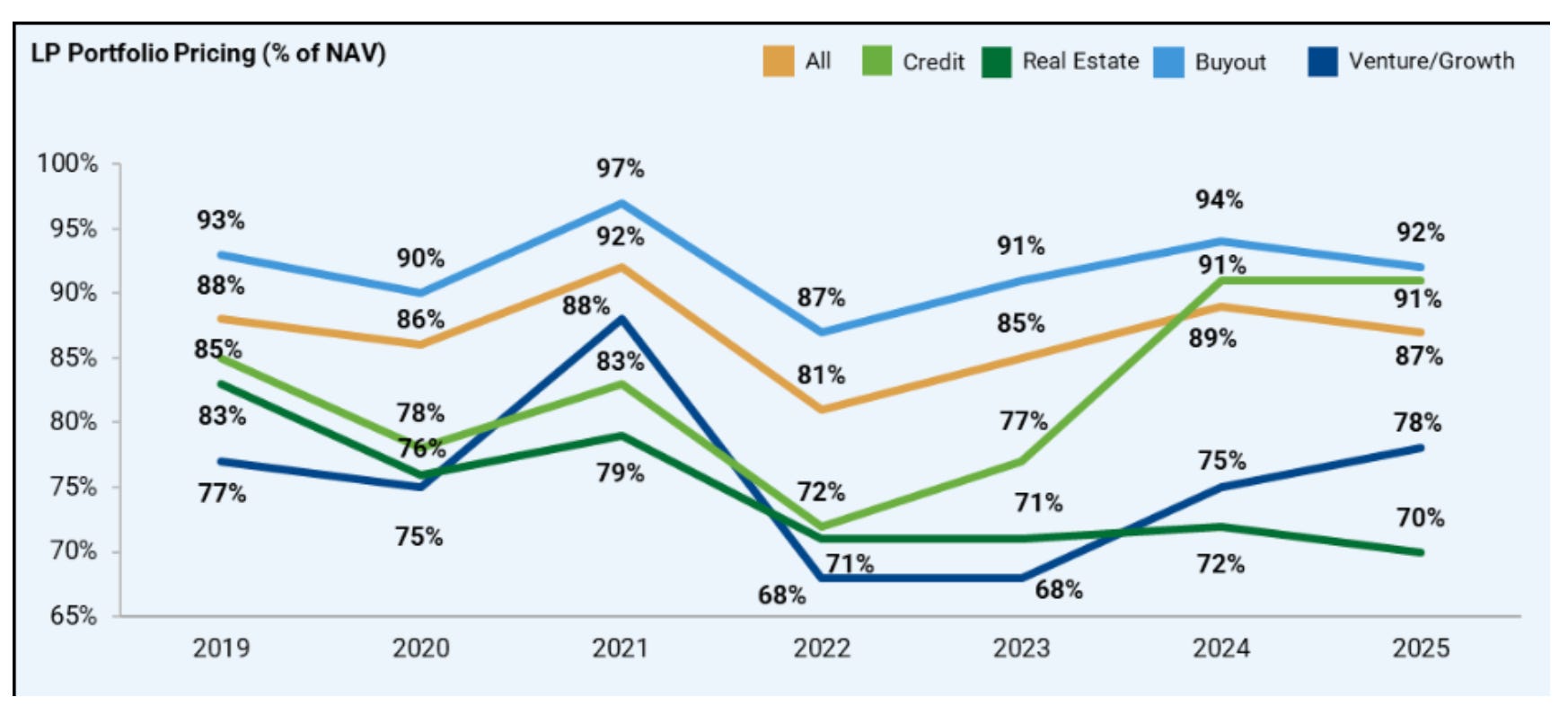

The secondaries market is not coming to the rescue (at least not for these assets).

Here’s how secondaries work:

Jefferies data shows that pricing varied by fund age: funds less than five years old priced at an average of 95% of NAV, while tail-end funds more than ten years old priced at 73% of NAV. The weighted average vintage sold across strategies was 2018.

👉 Invest in PE? Read this:

2️⃣ Private Credit

TL;DR:

Apollo, Ares, and BlackRock all hit their redemption gates within days of each other ($4.6B now queued)

Default rate came in at 5.4% in February, down from 5.8% in January

I wanted to share a quick resource: Sekond has launched a free liquidity tracker for non-traded funds. This tool is free (and not sponsored, I just thought it might be useful). You can check it out by clicking the button below:

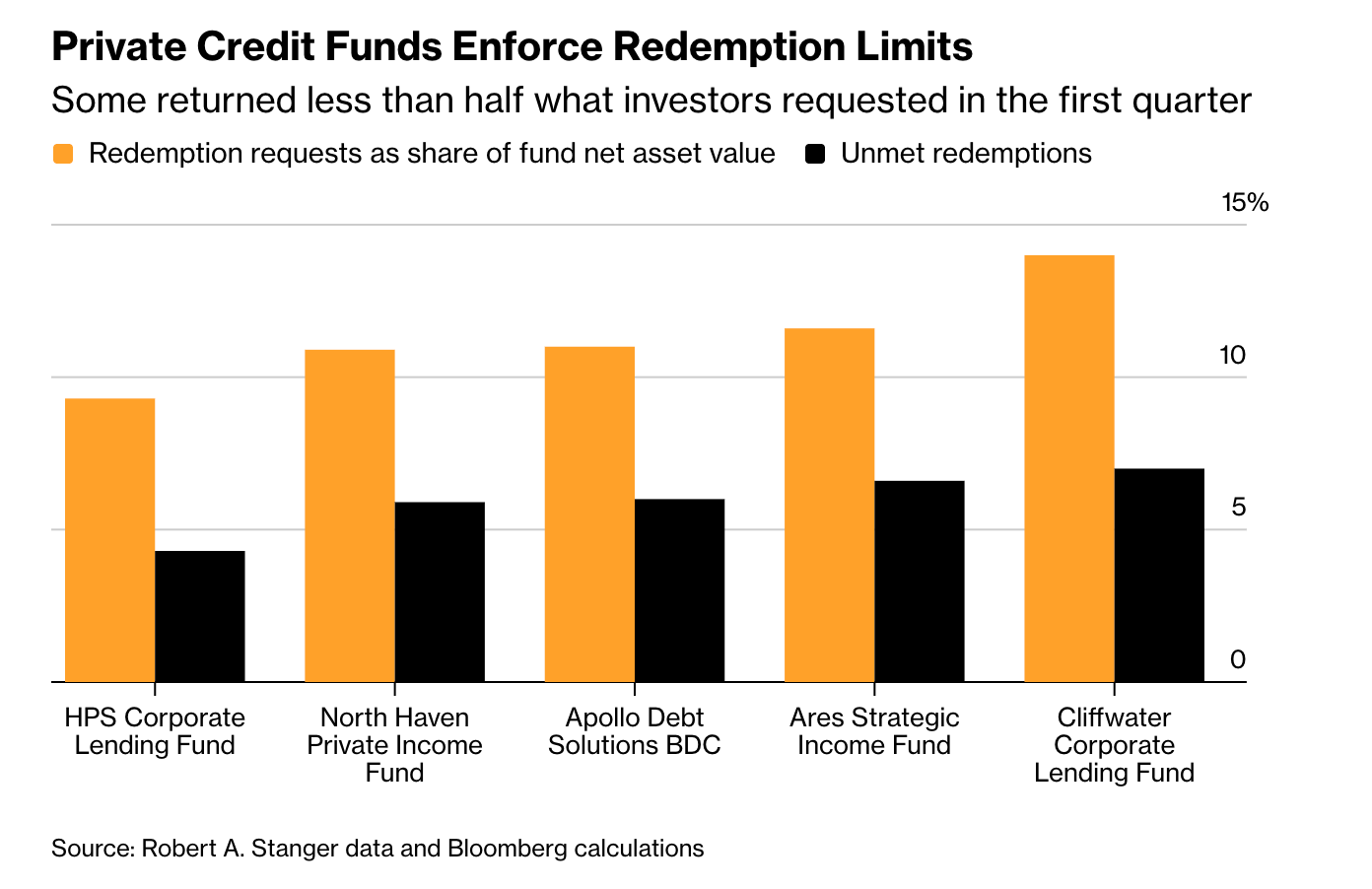

1. Gates Everywhere

In late March, Apollo, Ares, and BlackRock all hit the same wall within days of each other:

Apollo Debt Solutions (~$15B AUM): 11.2% in requests against a 5% gate

Ares Strategic Income Fund ($10.7B AUM): 11.6% in redemption requests, 5% gate

BlackRock’s HPS Corporate Lending Fund (~$26B AUM): 9.3% in requests, 5% gate

The sector is now sitting on roughly $4.6 billion in queued redemption requests.

👉 Need to understand how gating actually works?

2. What's in the portfolio?

Per Fitch Ratings, the U.S. private credit default rate was at 5.4% in February (down from 5.8% a month earlier):

72 borrowers → 87 default events over the trailing 12 months (multiple events per borrower)

Liquidity stress is driving defaults:

55%: interest deferrals or switches to PIK

31%: stressed maturity extensions

There is “good” PIK, and there’s “bad” PIK:

Hard defaults remain limited:

6%: uncured payment defaults

True break situations are still a minority (8%): bankruptcies, liquidations, debt-for-equity swaps, or restructurings

In these cases, sponsors exited their investments

Speaking of defaults, I traced all impaired loans in BlackRock’s TCP. Read the case study here:

3️⃣ Commercial Real Estate

TL;DR:

Private RE fundraising hit $172B in 2025, first YoY increase since 2021

Core open-end funds returned 3.7%, first positive year since 2022, but net cash flows are still negative $7.7B

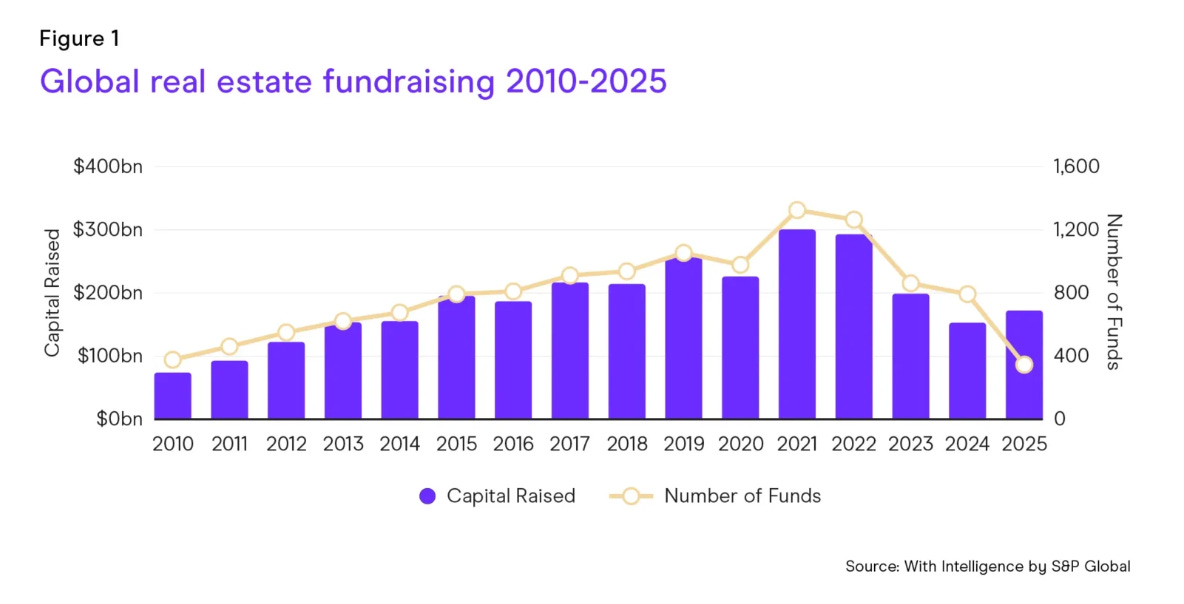

1. Fundraising Up

Private real estate fundraising reached $172 billion in 2025, up 13% from the prior year. This is the first year-over-year increase since 2021, per With Intelligence's 2026 Real Estate Outlook.

U.S. open-ended core funds posted a 3.7% return for the year, technically marking the first positive outcome since 2022. Net investor cash flows from open-ended core funds remained negative at -$7.7B for the year (an improvement from the -$9.4 billion outflow in 2024), but still a net exodus.

Here’s an interesting dynamic: top 10 funds captured 40% of total 2025 fundraising, highlighting industry consolidation.

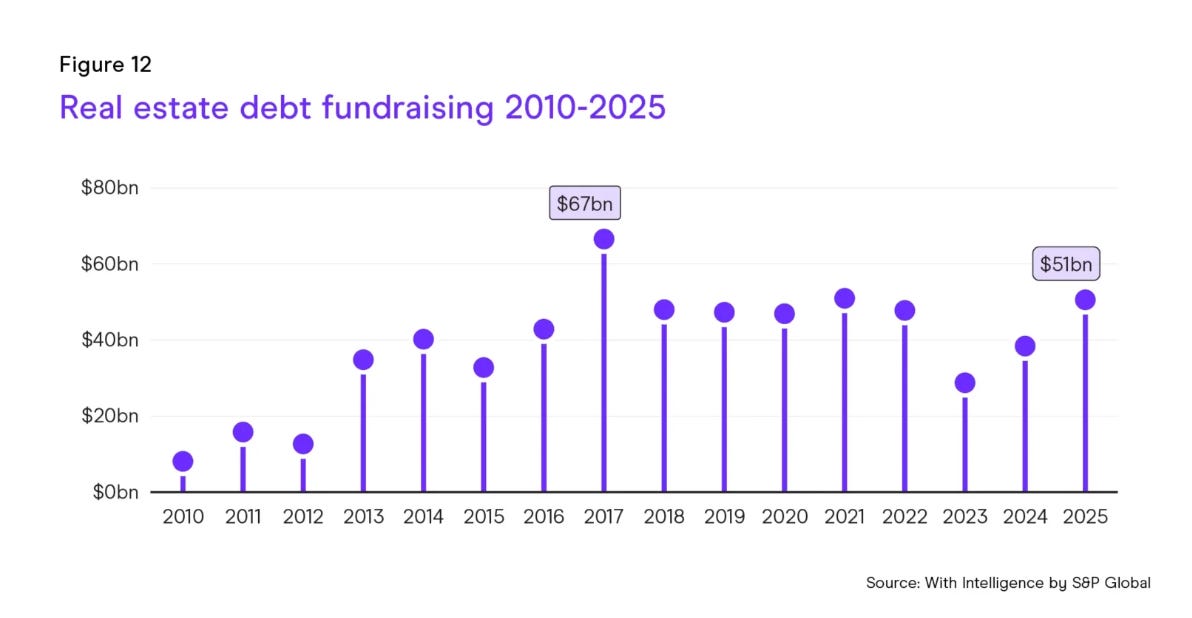

2. Real Estate Debt Funds on the Upswing

Higher interest rates and tighter lending push borrowers toward private credit. Real estate debt funds closed $51B in 2025, the highest since 2021:

Both established and new managers are launching debt strategies; market share expected to grow.

From S&P: “Debt funds have also outperformed their equity counterparts: the NCREIF/CREFC Open-end Debt Fund Aggregate, tracking 18 real estate debt funds, returned 5.5% YTD gross of fees at the end of Q3 2025, against the NFI-ODCE’s 4% over the same period.”

👉 Real estate people, you are going to love this icymi:

P.S. New here?

Here’s where you’ll find the full archive (somewhat organized):

Thanks for reading! As always, if you have any suggestions, reply to this email, leave a comment, or find me on socials (unhinged me on X, or come troll me - intelligently - on LinkedIn)

-Leyla

Can someone contact me. I’ve paid and can’t access.