K-Shaped PE, Private Credit Gates, and $0.58 Recovery on a AAA Bond

🗞️ Sunday digest: private markets insights 3/8

Happy Sunday.

Every other week, we send a quick digest on what’s catching our eye across private markets (the data, the drama, and the stuff LPs should actually care about).

Chart of the day (I’ll explain later, keep reading):

Today’s lineup:

1️⃣ Private equity: $1.3 trillion in dry powder, and PE comes to your brokerage account

2️⃣ Private credit: the golden age is over. The question is, can you leave voluntarily?

3️⃣ Commercial real estate: a AAA bond recovers 58 cents, and extend-and-pretend might never end

Before we dive in:

Accredited Insight delivers the LP’s perspective on private credit, private equity, and CRE, drawing on hundreds of deals, and thousands of conversations. Paid subscribers gain access to our database of over 40 case studies and articles on everything from evergreen funds to due diligence.

1️⃣ Private Equity

TL;DR:

The K-shaped recovery in PE: deal value surged but only the mega-funds are eating

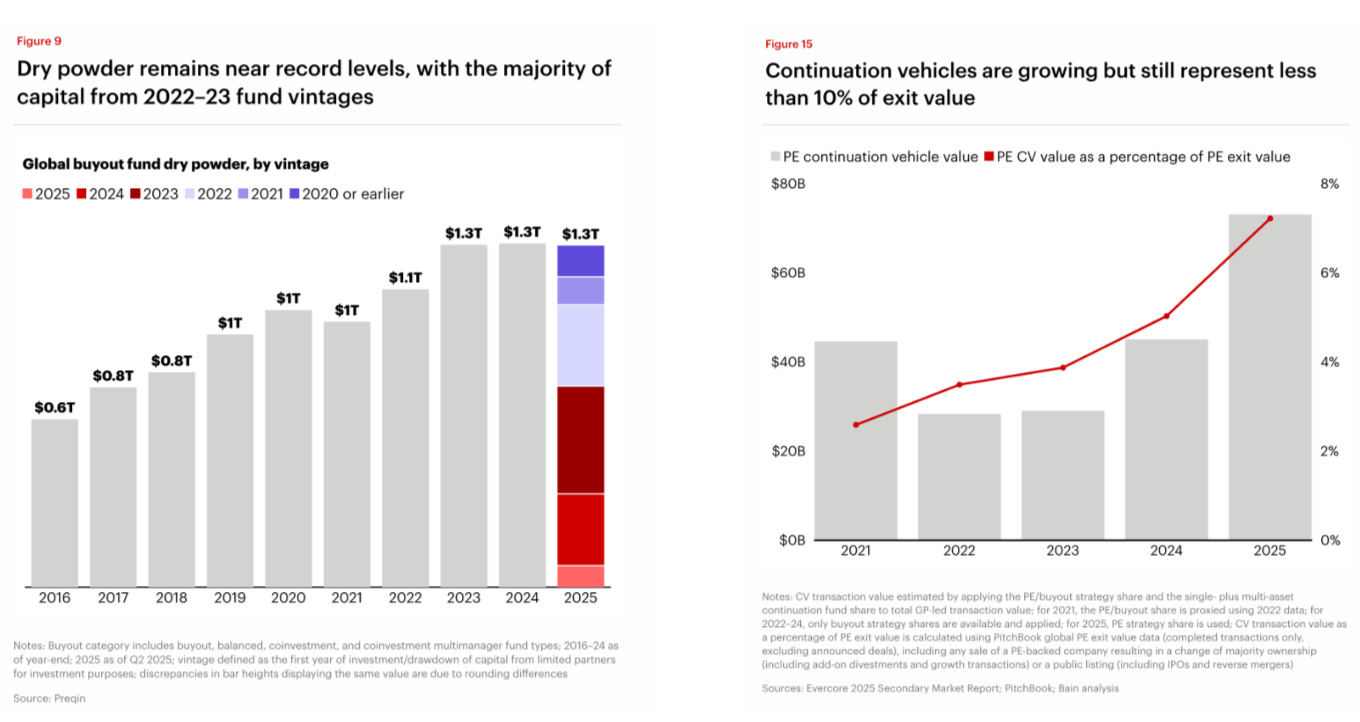

$1.3 trillion of dry powder, and a surge in CVs

Capital Group and KKR just launched a PE interval fund for retail investors with a $1,000 minimum

Bain dropped its 17th annual Global Private Equity Report

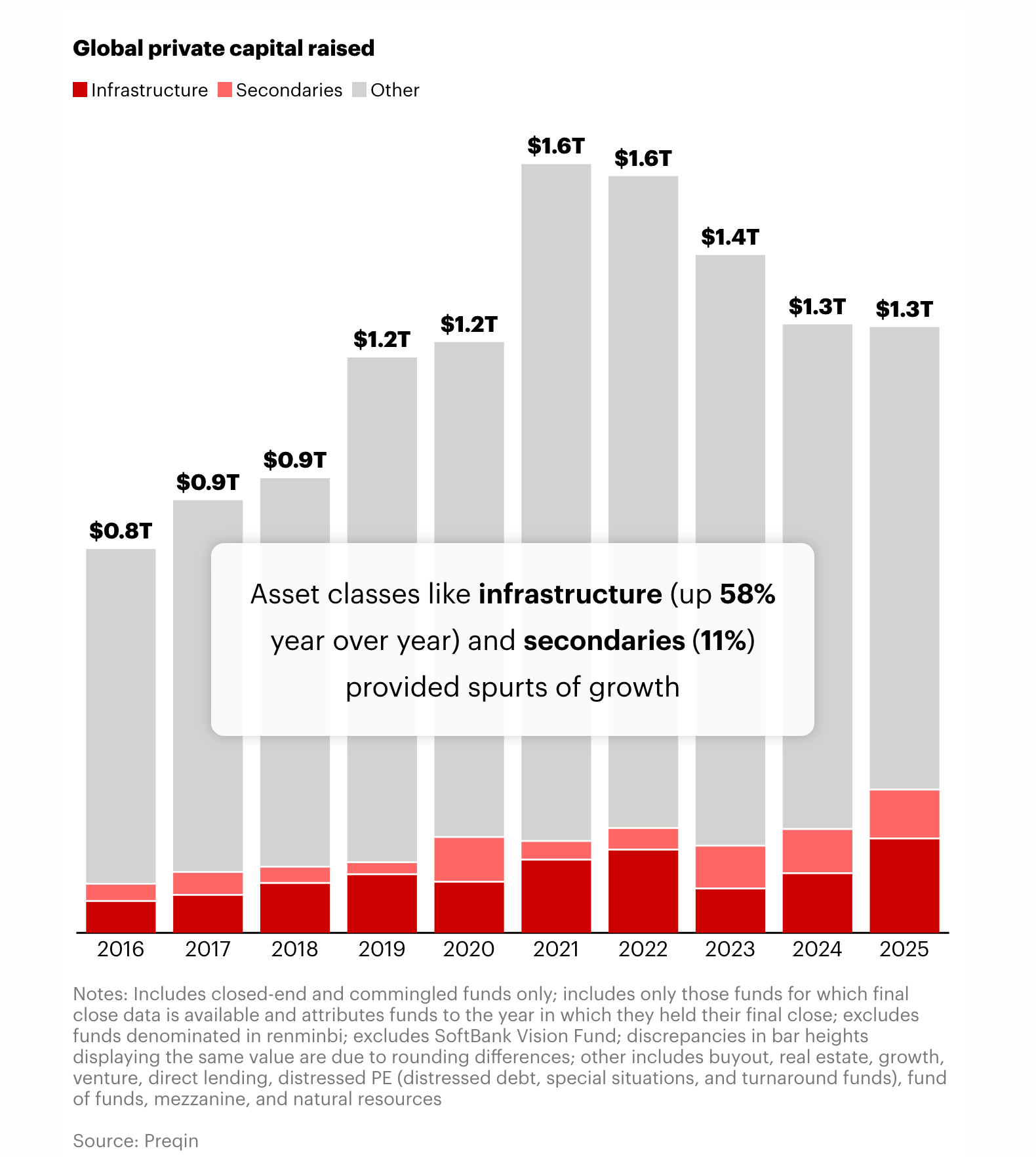

Buyout deal value hit $904 billion in 2025, up 44% year-over-year. Exit value jumped 47% to $717 billion. Second-best year ever on both counts.

Fundraising remains flat (down 30% from 2023 peaks). Why? Distributions to LPs as a percentage of NAV have been stuck below 15% for four consecutive years (industry record). LPs are tapped out: when distributions aren’t coming, LPs don’t make new commitments.

It would be very interesting to find out how many institutional LPs are having trouble coming up with liquidity to meet capital calls on prior commitments - has anyone seen this data?

The industry is sitting on 32,000 unsold companies worth $3.8 trillion. Holding periods at exit now average around seven years, up from five to six during the 2010s.

Continuation vehicles continue to fill the gap. GP-led CV volume grew 62% year-over-year. Secondary deal volume (GP- and LP-led combined) rose 41%.

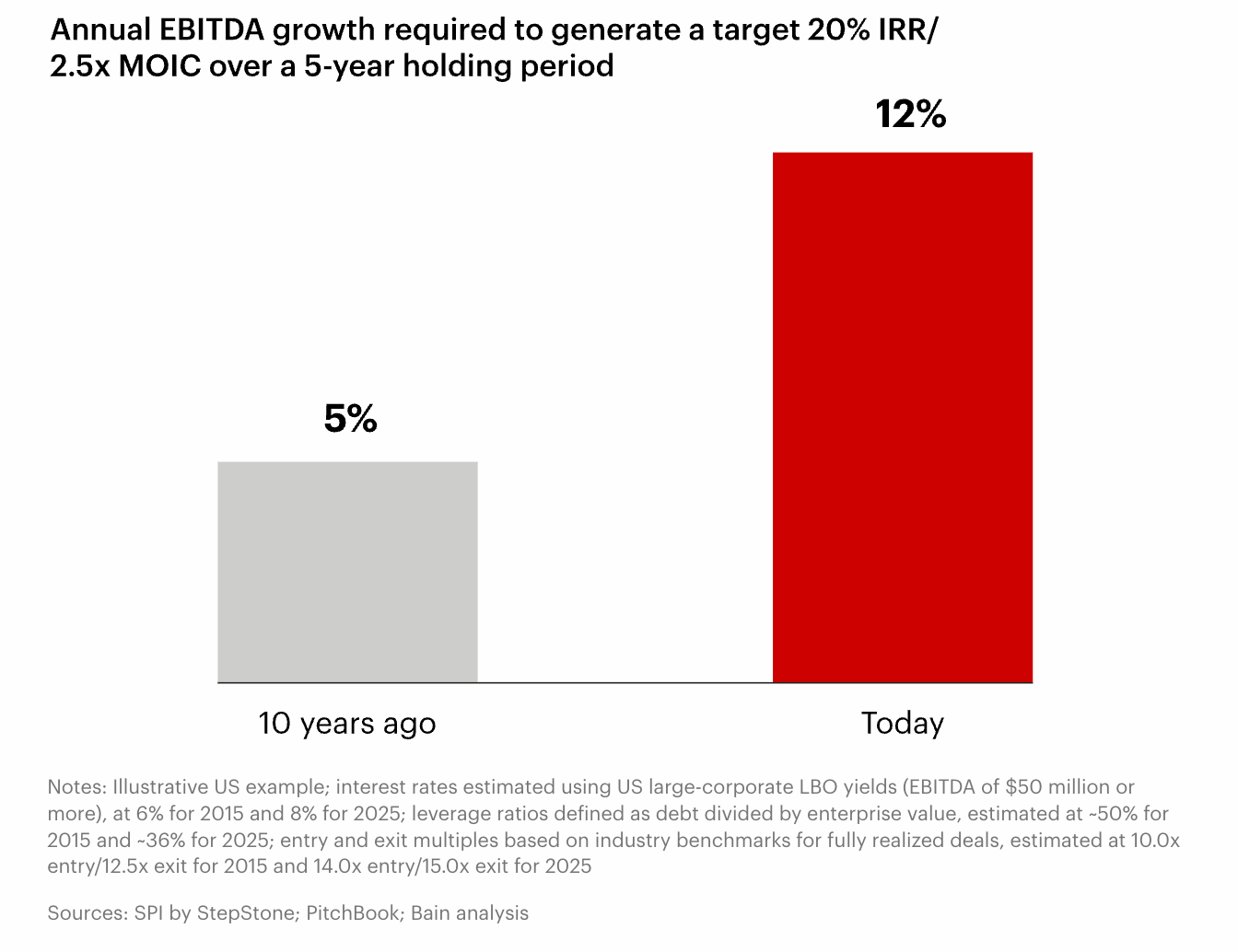

➡️ Bain’s big thesis this year: “12 is the new 5.” In the 2010s, a typical deal needed ~5% annual EBITDA growth to hit a 2.5x return over five years. Today, with borrowing costs at 8–9%, leverage ratios at 30–40%, and purchase multiples at record highs, that same return requires 10–12% annual EBITDA growth. The math is A LOT harder.

👉What drives returns in PE deals:

2. Capital Group + KKR: PE Comes to Your Brokerage Account

The retailification of private equity continues.

On March 3, Capital Group and KKR launched Capital Group KKR U.S. Equity+, the first public-private equity interval fund from their partnership. (The two firms already rolled out two credit interval funds in 2025).

The structure: roughly 60% in actively managed large-cap US equities, up to 40% in KKR’s private equity strategies. A truly “democratized” product: no accreditation required, and $1k minimum. This, friends, is an interval fund, with limited quarterly liquidity.

👉 Yes, you need to know how gating provisions work:

2️⃣ Private Credit

TL;DR:

BlackRock just gated redemptions at its $26B HPS fund (the first time since inception)

Blackstone met record $3.8B in redemptions at BCRED (but had to step in with its own capital)

Dare I say it? We have begun testing the limits of semi-liquid structures.

Here’s your primer on evergreen vehicles:

The Gates Are Going Up

Turns out, the OBDC II saga was the opening act. Last week we got the main event.

On Friday, BlackRock disclosed that investors in the $26 billion HPS Corporate Lending Fund (HLEND) requested redemptions of 9.3% of shares, roughly $1.2 billion (LINK). Management capped repurchases at 5%, paying out approximately $620 million. It’s the first time requests have breached the 5% threshold since the fund’s inception.

BLK stock dropped ~8%. KKR and Ares sold off in sympathy.

Three days earlier, Blackstone reported that investors requested a record 7.9% of shares from BCRED, its $82 billion flagship credit fund (~$3.8 billion). Blackstone upsized its quarterly repurchase offer from 5% to 7%, then the firm and its employees collectively put in ~$400 million to cover the rest ($250M came from the firm, $150M - from employees).

Investment bank RA Stanger is now forecasting a ~40% year-over-year decline in BDC capital formation for 2026. If accurate, that would be the most severe fundraising contraction in the sector’s modern history.

👉 Invest in private credit? Here’s how you can learn to read the statements:

→The one to watch this week is CCLFX: the repurchase offer deadline for Q4 is 3/10/26.

3️⃣ Commercial Real Estate

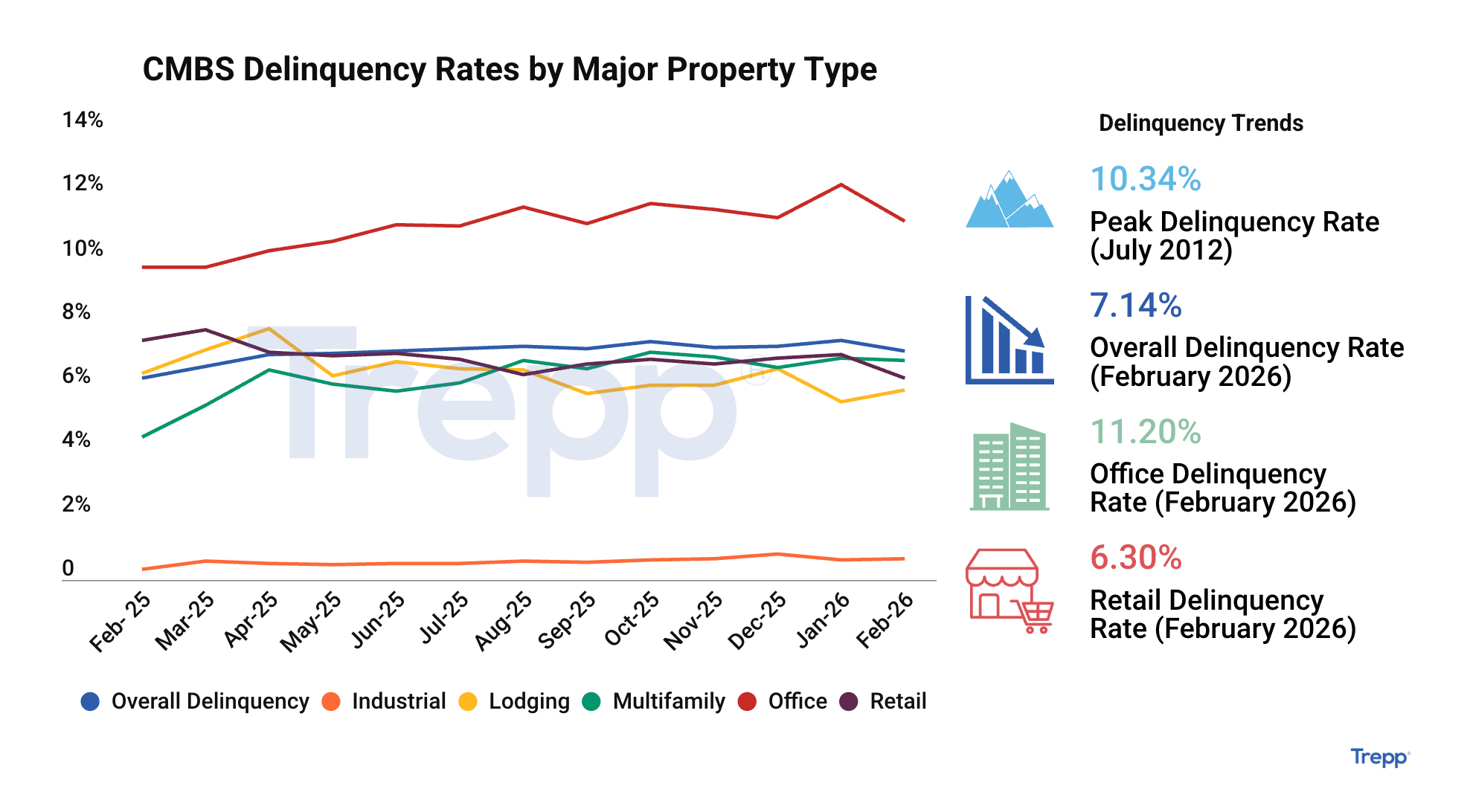

CMBS bondholders just lost $139 million on a single San Francisco office tower

The February Trepp data for office delinquencies looks better, after hitting an all-time high of 12.34% in January. But don’t pop the champagne yet

The February CMBS delinquency rate fell 33 bps to 7.14%, but it was driven by modifications and extensions on a handful of large office and mall loans, not by borrowers actually paying off debt.

Extend and pretend is alive and well. The rate is 8.75% including loans past maturity but current on interest.

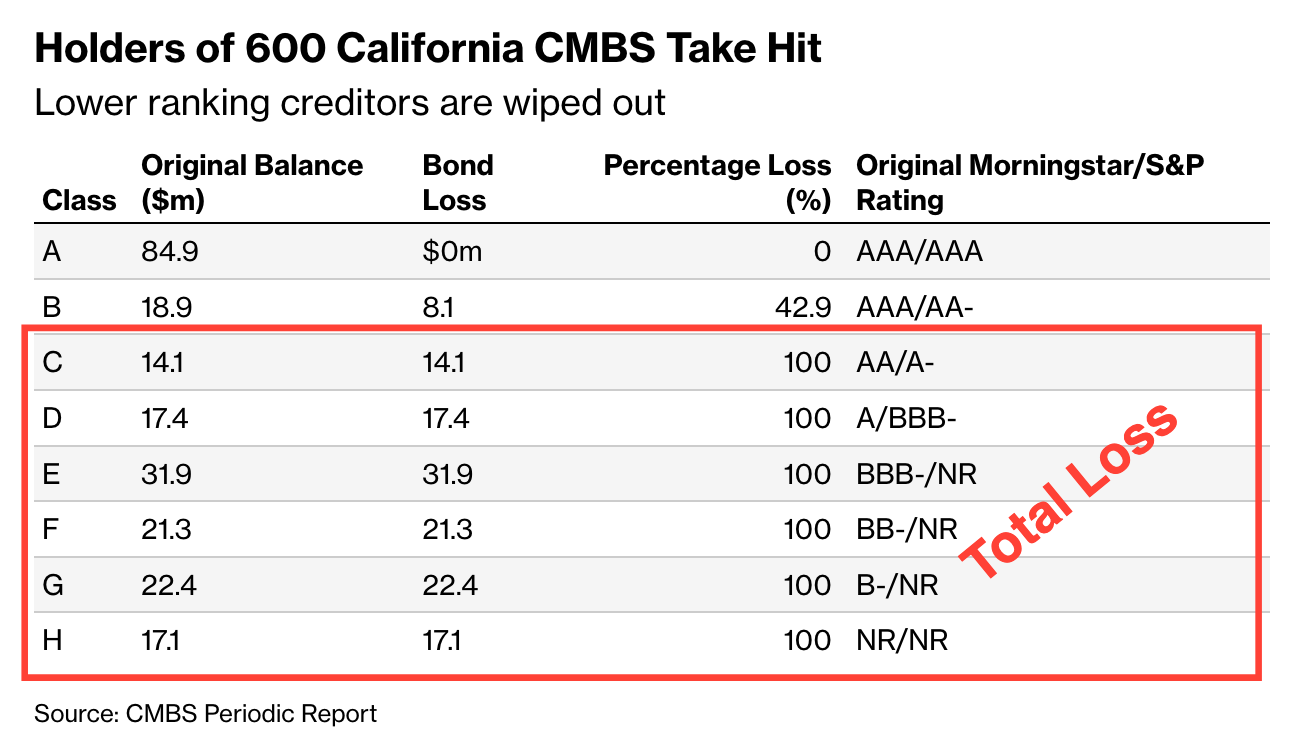

How to Lose Money in a AAA-rated Security, a Short Tutorial

A $240 million single-asset, single-borrower (SASB) CMBS tied to 600 California Street in San Francisco just liquidated at roughly 58 cents on the dollar (generating losses of 42 cents). Six junior tranches were wiped out entirely. The second-most senior bonds, originally rated AA- by S&P and AAA by Morningstar, lost more than 40% of principal (Bloomberg).

Back in 2019, the building was appraised at $349 million when WeWork Capital Advisors acquired it. By the time the loan was sold to Lone Star Funds in December for about $123 million, the property was only 26% leased 🤕

This is not a one-off, either. Bloomberg flagged that top-ranked SASB tranches tied to Peachtree Center (Atlanta), EY Plaza (Los Angeles), and River North Point (Chicago) all trade below 80 cents on the dollar. Lower tranches at far steeper discounts.

Why should LPs care? If you’re in a fund that holds SASB paper, the rating on the bond you bought may have very little relationship to the recovery you’ll actually receive. (58 cent recovery on a bond rated AAA is quite something, isn’t it?)

P.S. New here?

Check out some of our popular topics to get started: on private credit, private equity, and commercial real estate.

Thanks for reading! As always, if you have any suggestions, reply to this email, leave a comment, or find me on socials (unhinged me on X and an increasingly unbothered me on LinkedIn)

-Leyla

Did you mean 58 cents?

Eyes on the ground 40 years in credit. Commercial credit quality has only progressively worsened.