PE's Groundhog Day | Private Credit Queue Gets Longer | CRE Cap Rates Found a Floor?

🗞️ Sunday digest: private markets insights 6/28

Happy Sunday!

Every other week, we send a quick digest on what’s catching our eye across private markets.

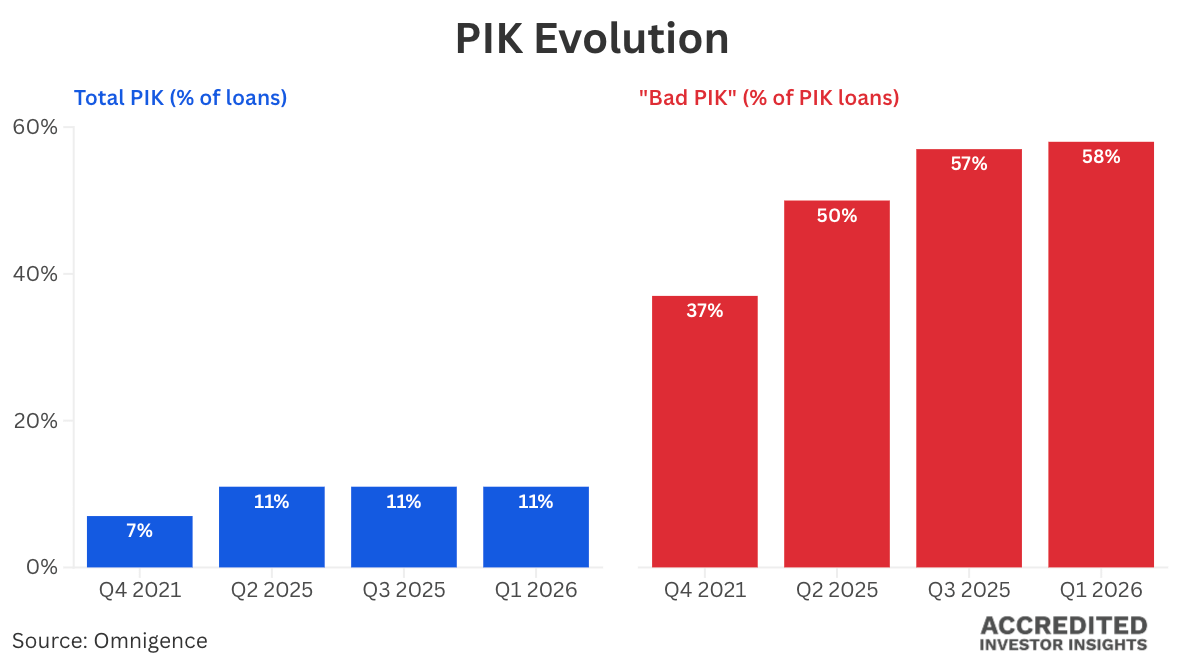

Before we get into it, chart of the day:

The chart shows you the evolution of PIK usage as the cycle progressed. Total PIK usage is up since 2021, but what's more interesting is "bad PIK" rising as a proportion of PIK loans. This, folks, is mostly distressed borrowers kicking the can. In theory, when more borrowers become distressed, markdowns should follow.

In Q1 2026, we saw the other shoe drop: broad-scale markdowns across the traded and non-traded BDC universe. If you missed that post, you'll find it here.

Accredited Insight delivers the LP’s perspective on private credit, private equity, and CRE, drawing on hundreds of deals, and thousands of conversations. Paid subscribers gain access to our database of over 40 case studies and articles on everything from evergreen funds to due diligence (the kind of analysis that tells you what the GP pitch deck left out).

Today’s lineup:

1️⃣ Private equity is living its version of Groundhog day

2️⃣ Private credit: redemptions are up (but not for all funds)

3️⃣ Commercial real estate: cap rates are stabilizing (two cheers for that!)

Private Equity

1. Groundhog Day

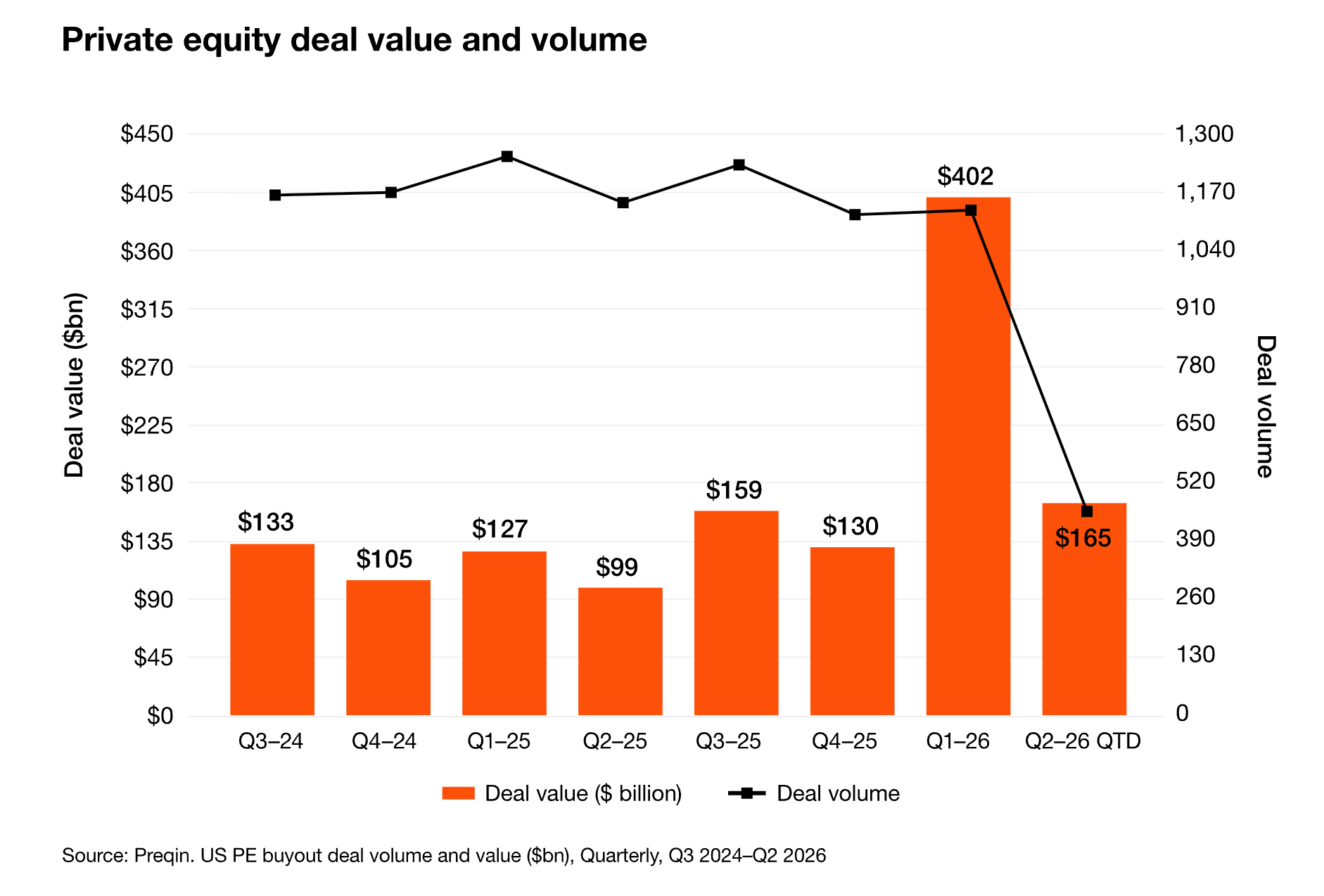

Private equity entered 2026 feeling surprisingly optimistic: tariff fears had faded, the IPO window looked cracked open, deal activity was picking up. For a brief moment, it seemed like the industry might finally escape the liquidity drought that has defined the last three years.

Then came “SaaSpocalypse”, redemption stress across private credit, and a war.

Bid-ask spreads widened and exit momentum stalled yet again. PwC data shows H1 deal volume down 34% year-over-year while total deal value rose nearly 10%. In other words, fewer deals are getting done, but the ones that do happen are attracting a disproportionate share of capital.

Bain calls this the Groundhog Day scenario: another year where recovery is always six months away.

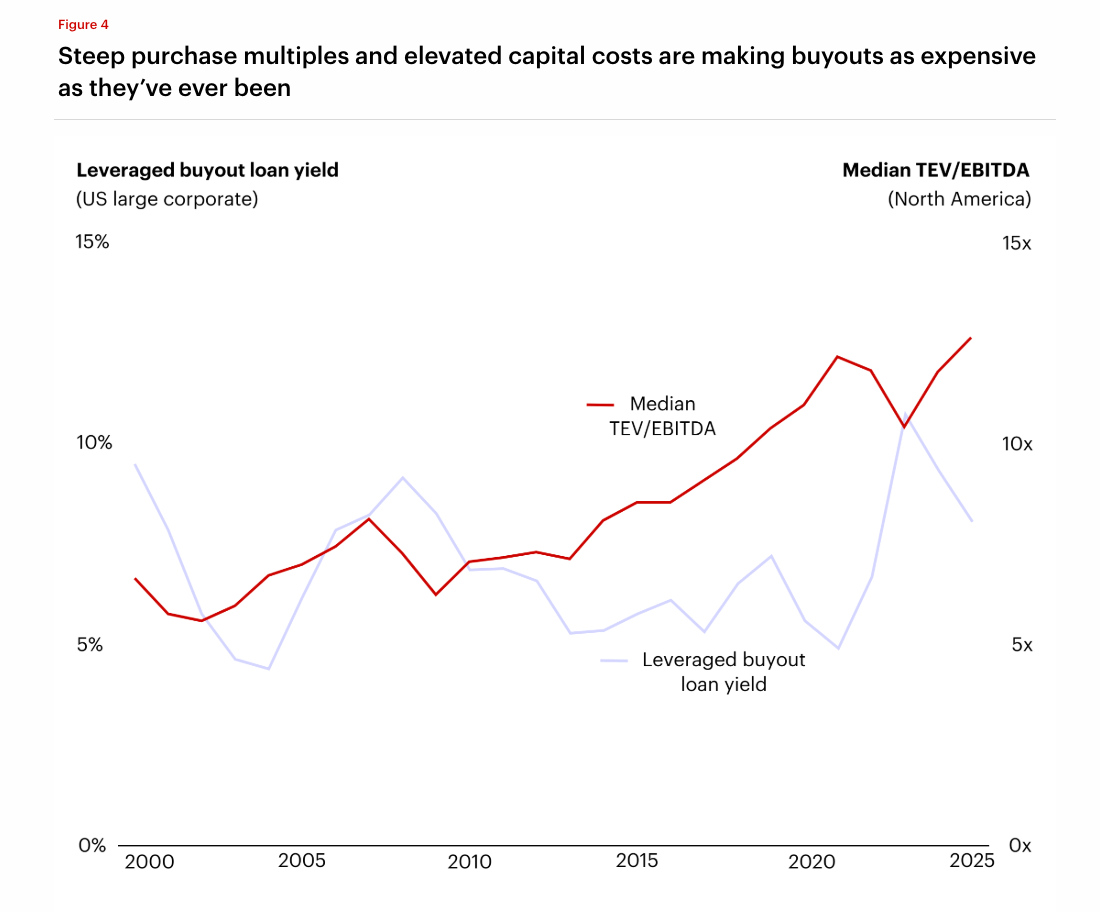

The math became harder: a decade ago, a buyout deal could generate a 2.5x return with roughly 5% annual EBITDA growth. Leverage was cheap, entry multiple were reasonable, and multiple expansion did a lot of lifting.

Today, with entry multiples for larger buyouts running around 11–12x EBITDA and debt costs at 8–9%, that same 2.5x outcome requires closer to 10–12% annual EBITDA growth. Bain's shorthand: "12 is the new 5."

Tech was hit particularly hard. Deal value in the sector fell roughly 70% from Q4 2025 to Q1 2026. Private equity software portfolios also took marks lower, though nowhere near the public market bloodbath. Most reported declines were in the high-single-digit range.

Side note: I recently joined the Hedgeye podcast to discuss private markets, and the conversation touched on what made PE and the Swensen model so successful back in the day, give it a listen :)

☝️I wrote this a year ago, my opinion has not changed.

2. Fundraising

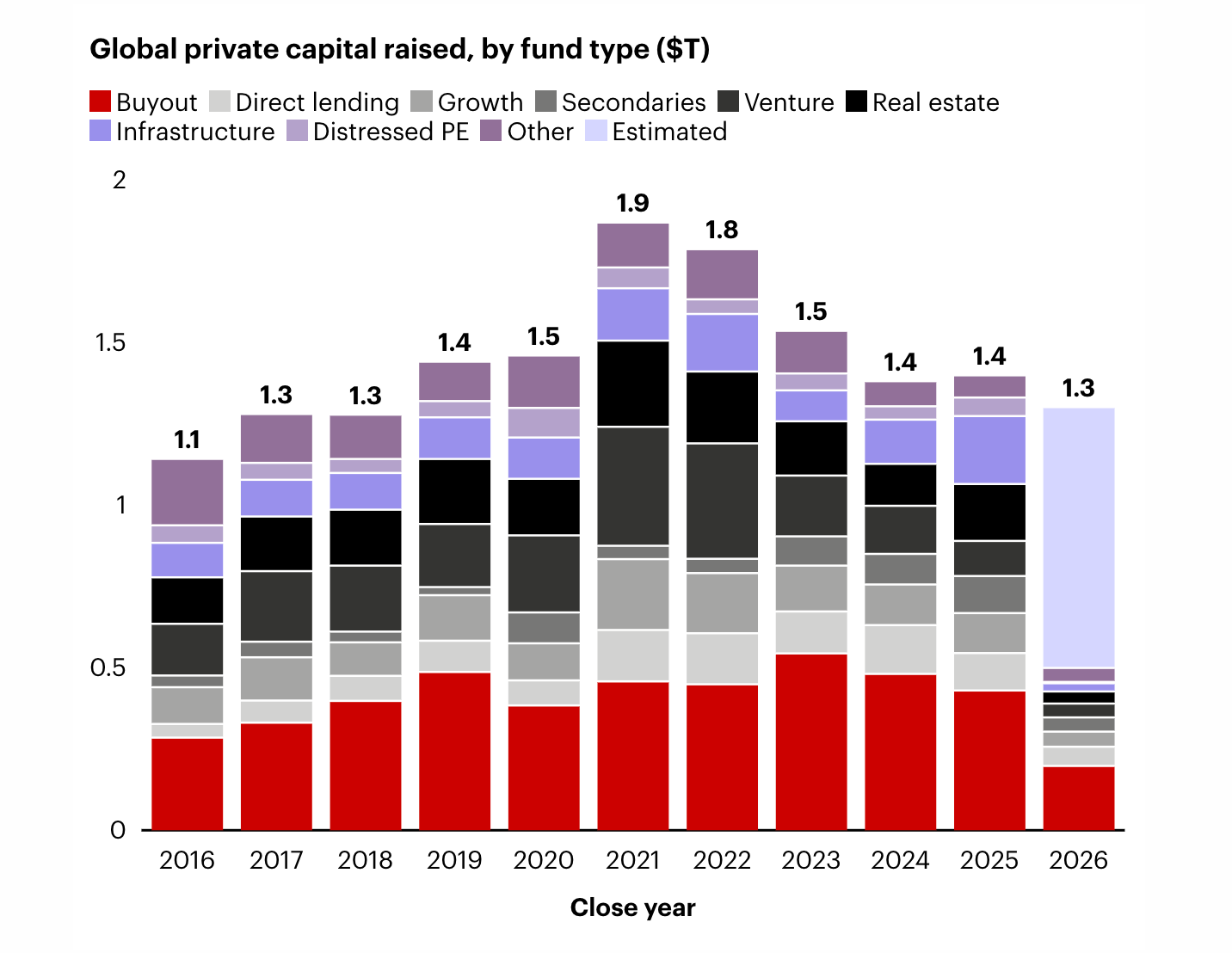

Global private capital fundraising is on pace for roughly $1.3 trillion in 2026, the weakest year since 2016. Buyout’s share of total fundraising is hovering near multi-year lows.

The problem is simple: exits haven’t recovered. Bain estimates it takes 12-18 months of sustained exit activity before fundraising meaningfully improves.

3. What Institutional LPs Think

From the latest ILPA survey:

47% of LPs expect to reduce exposure to large-cap PE managers over the next 12 months

‼️ 84% are less likely to invest with managers that raise significant amounts of retail capital

Only 21% view continuation vehicles as a preferred source of liquidity (no surprises here)

CVs are a fun topic. Here’s your primer:

And they are starting to show up in evergreen funds:

Private Credit

1. Redemptions Are Up

Q2 redemption data is coming in, and the queue isn’t getting shorter:

Apollo Debt Solutions capped withdrawals at 5% after investors requested redemptions equal to 16.8% of NAV, up from 11.2% in Q1.

Morgan Stanley’s North Haven Private Income Fund saw redemption requests reach 11.6% of NAV and fulfilled just 43% of them.

Ares Strategic Income Fund said it had received redemption requests worth 14.4% of the vehicle (up from 11.6% in Q1). The list goes on…

The notable exception was Oaktree Strategic Credit Fund, which reported redemption demand of just 4.5% and honored all requests in full.

None of this should come as a surprise, of course: there is no penalty for requesting a redemption, and for advisers, it’s a classic prisoner’s dilemma with only one rational solution:

What's more concerning is the portfolio markdowns. When a fund marks assets down, NAV per share drops. Lower returns beget more redemption requests. I don't expect redemptions to slow materially in Q3, but time will tell.

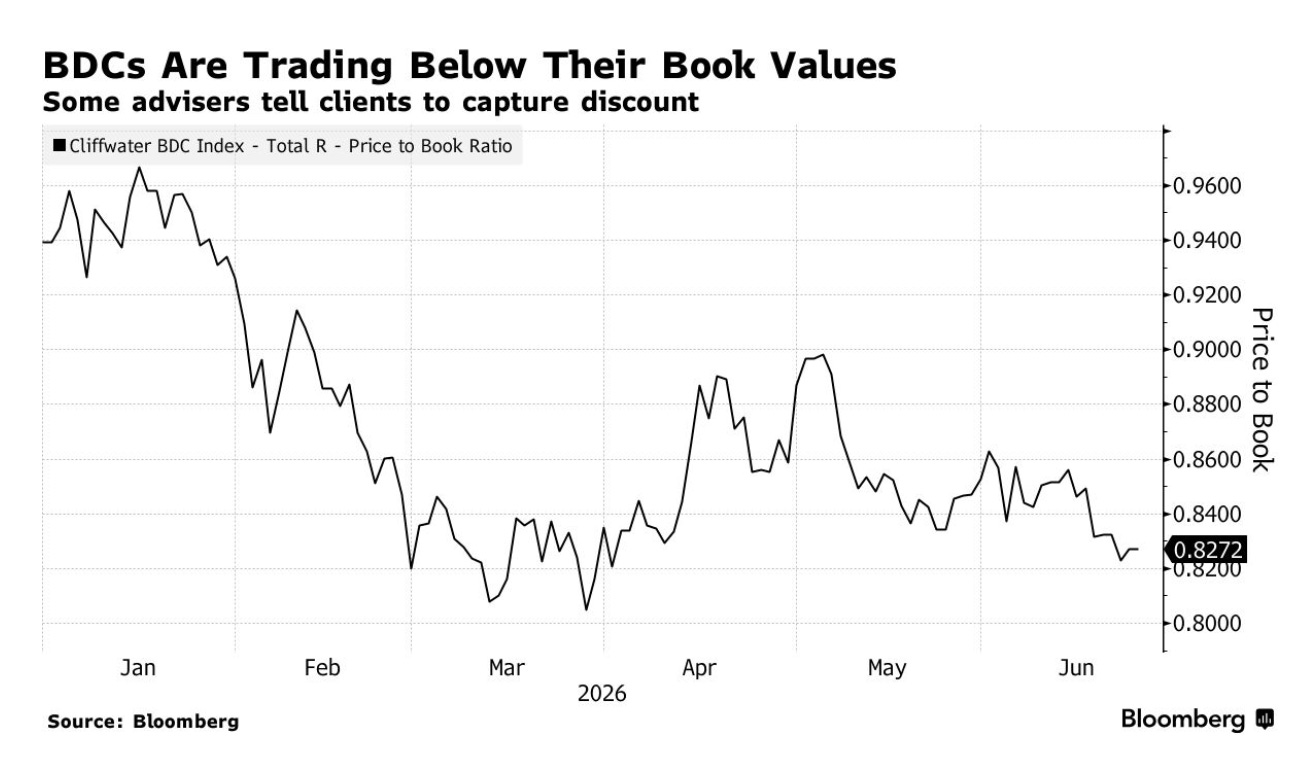

2. The Obvious Trade

Mainstream media is catching on to the most obvious trade under the sun: listed BDCs currently trade at a median discount to NAV of roughly 25%, arguably reflecting concerns that private credit valuations have further to fall. Meanwhile, many non-traded vehicles continue to offer liquidity at stated NAV (Bloomberg).

The trade is straightforward in theory: redeem from the non-traded vehicle at NAV and rotate into the publicly traded equivalent at a substantial discount. The only trouble is, the article is about six months late.

I wrote about this back in October (hehe):

The catch, of course, is that “redeem at NAV” only works if you can actually redeem. If your request is prorated to 43% this quarter, the trade may take considerably longer to execute.

(Yes, there are meaningful differences in fees, leverage, and portfolio construction between listed and non-traded vehicles, but not meaningful enough to ignore the obvious)

3. Insurance and Private Credit

Away from the redemption headlines, a new report from Clearwater Analytics highlighted a less obvious risk lurking in insurance company portfolios.

Median allocations to private credit among U.S. life insurers have more than doubled since 2021, reaching roughly 9% of total assets.

More interesting was Clearwater’s finding that an estimated 10-20% of insurers with LP stakes in private credit funds also hold debt issued by those same funds. In other words, they’re investing in the fund and lending to the fund at the same time (“cross-contamination” is what Clearwater calls it). WSJ’s article on the subject is here.

3️⃣ Commercial Real Estate

From Yardi’s latest data:

Multifamily remains oversupplied. National rents posted modest growth in the first half of 2026, but nearly 1.3 million units remain in lease-up.

The recovery is highly market-dependent. Gateway cities and lower-cost Midwest markets are outperforming, while many Sun Belt markets are still digesting a wave of recent deliveries.

Supply relief is coming, but slowly. New apartment starts fell more than one-third from their 2022 peak, yet developers are still expected to deliver roughly 450,000 units annually through 2027, extending the supply overhang.

Debt markets are open. Fannie Mae, Freddie Mac, banks, insurance companies, debt funds, and CMBS lenders are all actively lending.

The bottleneck is pricing. There is plenty of debt capital available, but not enough sellers willing to transact at current market-clearing prices.

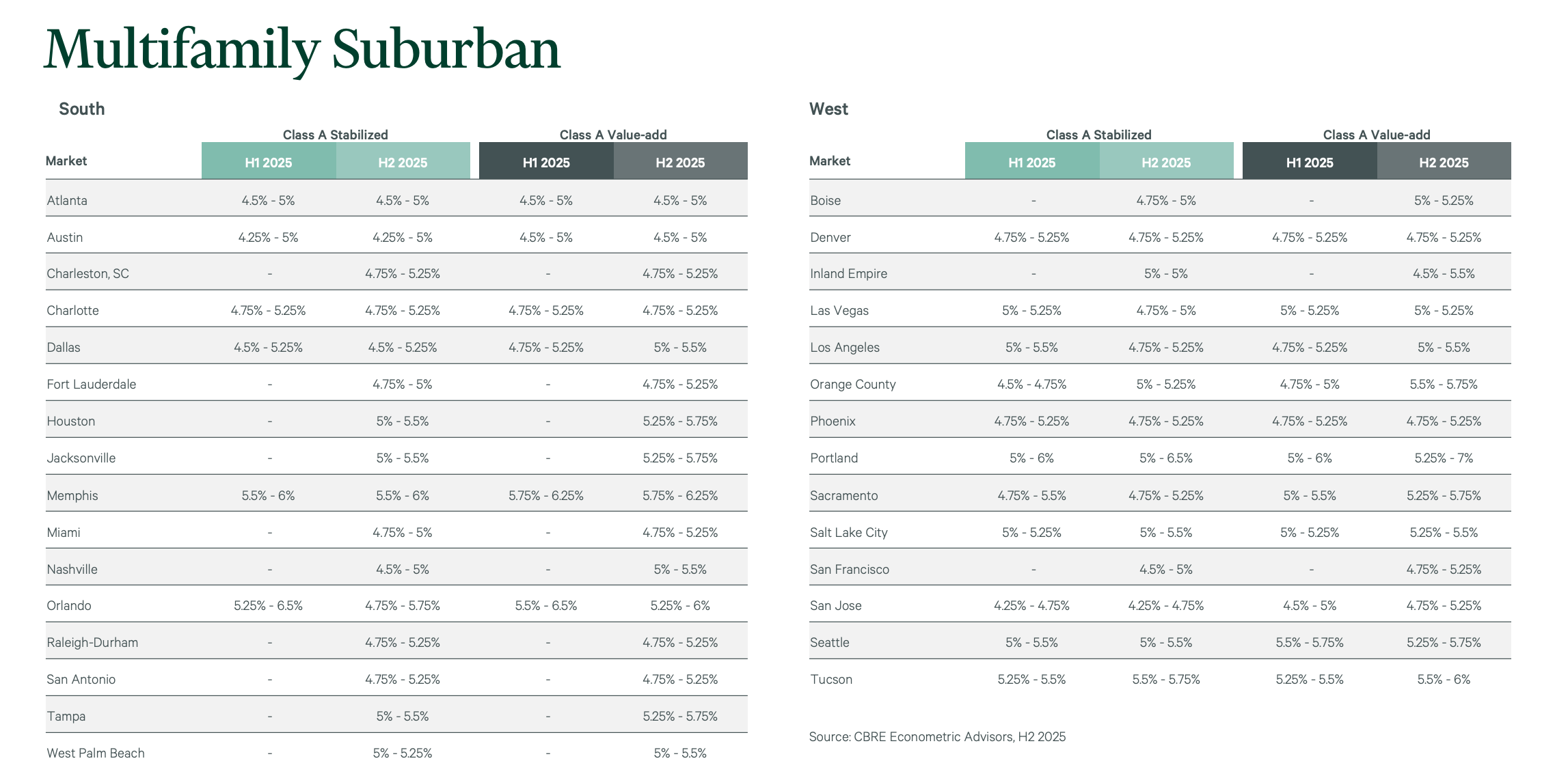

Last (but not least): CBRE cap rate survey

Cap rates are stabilizing, total CRE transaction volume was up 19% in 2025, and nearly all respondents believe that cap rates have peaked (you’ll find data on cap rates for other asset classes and geographic locations here)

If you invest in real estate deals or funds, you’ll find this helpful:

And finally, this SEC panel on the retailization of alternatives is worth a listen (discussion starts around 22:00). Mark Higgins, CFA, CFP (you should subscribe to his newsletter), Jason Zweig (whose column you undoubtedly read), Stephen Deane, Joseph Sheirer, and Kevin Gannon discuss whether retail investors truly understand the risks, liquidity constraints, and valuation challenges associated with semi-liquid private market investments.

Thanks for reading! As always, if you have any suggestions, reply to this email, leave a comment, or hit me up on socials (unhinged me on X, slightly more filtered me on LinkedIn). Have a great week!

-Leyla

P.S. New here?

Here’s where you’ll find the full archive (somewhat organized):

P.P.S. Meme of the day