The Prisoner's Dilemma: Semi-Liquid Edition

There is only one rational move

The headlines are not pretty: this week alone, both Ares and Apollo have reported capping redemptions. And it’s only Wednesday…

For years, redemption requests in semi-liquid vehicles ran well below the 5% threshold and were met comfortably, quarter after quarter, because inflows dwarfed outflows, because it was the "golden age of private credit," and because it was cool to brag about your private credit exposure to your golf buddies.

Then we heard about some "cockroaches," rapidly followed by "AI will eat software companies" and how those SaaS borrowers won't be able to repay the debt. And all of a sudden, direct lending is not so cool anymore.

I mean, when you have John Zito, co-president of Apollo's asset management arm, arguing that many private market participants are overly confident and stating "I literally think all the marks are wrong", — you should probably listen. (WSJ)

And listen investors did. (Turns out, many of them listened by requesting redemptions)

This quarter, the structural mismatch between illiquid assets and the “semi-liquid” nature of evergreen vehicles stopped being theoretical, as investors rushed for the exits.

Thousands of wealth advisors faced the same decision independently:

submit a redemption request for their clients’ interval fund holdings,

or hold.

If only I hadn’t warned you…

Next quarter, advisers who didn't face this decision will certainly hear from more of their clients, and will face it again. But therein lies a problem: if everyone holds, the fund operates smoothly. If everyone wants to redeem, gates slam shut.

👉 Here’s how that works:

To add a complication: advisers don’t know what others are doing, while at the same time being bound by a fiduciary duty to their client (not to the fund's stability, and certainly not to the other advisers' clients).

Welcome to the prisoner’s dilemma. Semi-liquid edition.

(Please note: this dynamic is a whole separate issue from asset quality. It’s driven by the structure of the vehicle and investor behavior. For now, there’s little evidence of broad deterioration of underlying loans, but if asset quality does weaken, it will only accelerate the dynamic)

First, some context

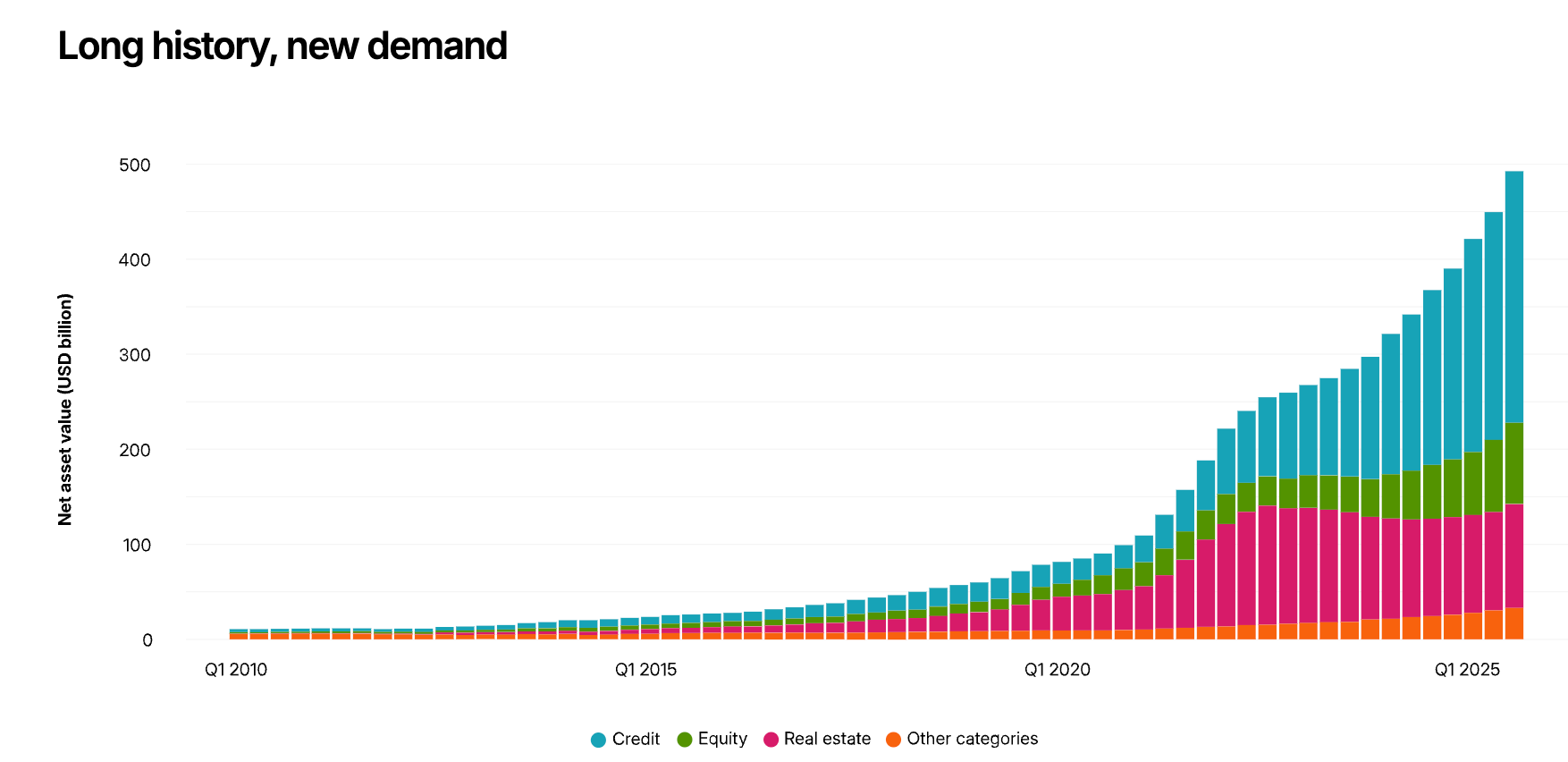

Semi-liquid private market funds (interval funds, tender offer funds, non-traded BDCs and REITs) have gone from niche to nearly $500 billion in AUM, with assets growing over 30% in the twelve months through September 2025 alone. The private wealth channel now represents roughly one-fifth of total evergreen fund AUM.

The pitch is compelling: access to inherently illiquid assets through structures that offer periodic liquidity in the form of quarterly redemptions, typically at NAV.

For advisers managing client portfolios, these are dramatically simpler than traditional drawdown funds. No capital calls. No J-curve. Full allocation from day one, and option to compound via reinvesting distributions.

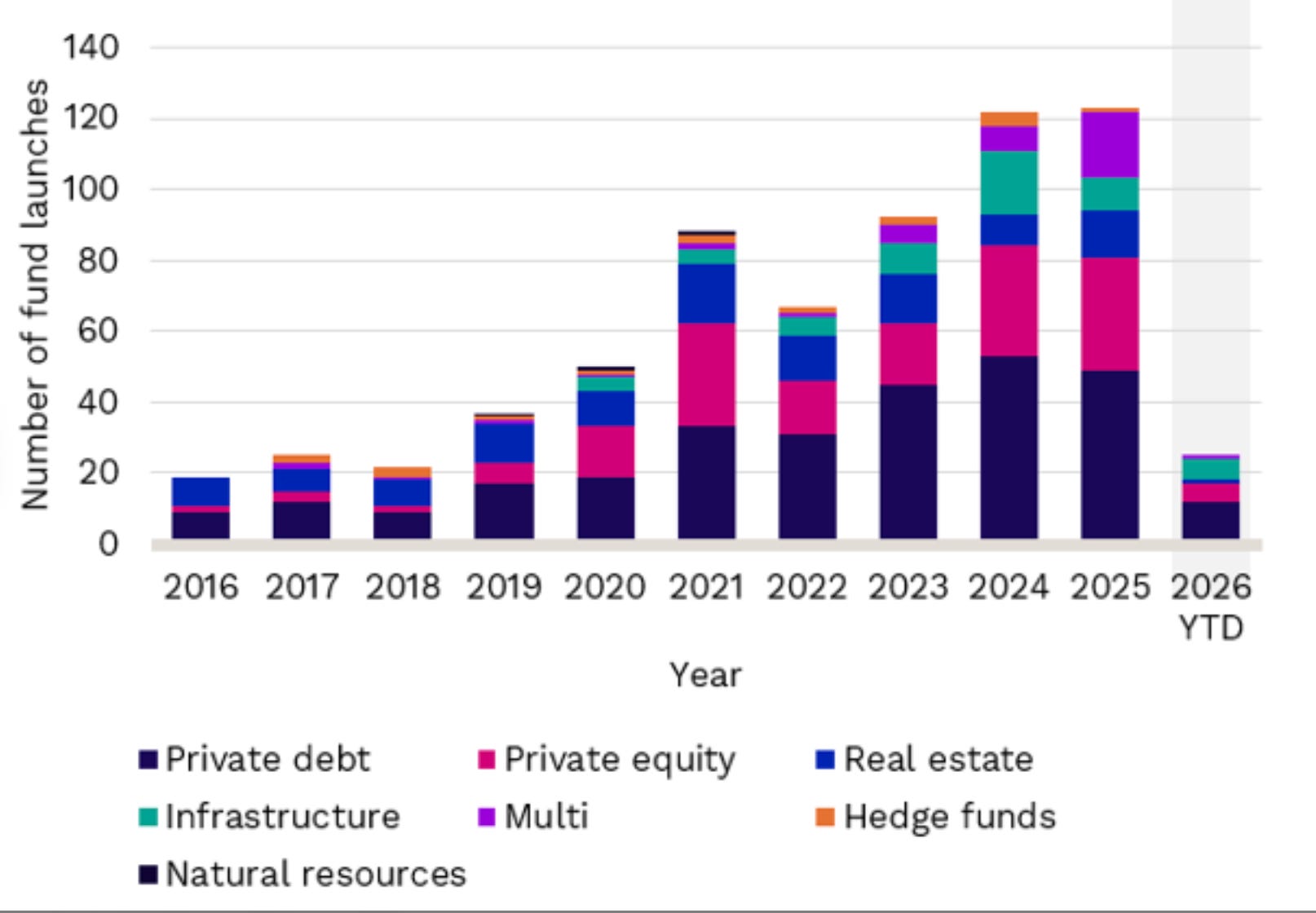

The industry responded with gusto: more than 120 evergreen funds were launched in 2025, and 30 so far this year:

The problem is that the “periodic liquidity” part is somewhat reliant on collective cooperation.

Today we’re talking about private credit semi-liquid funds (specifically, direct lending PC), since this is the topic du jour.

❗️And I’ll say this: of the universe of options, private credit is the asset class best suited for the semi-liquid structure:

high yield,

high portfolio turnover (20–30% organically pays off every year),

relatively short tenor on assets (loans are typically originated with 5–7 year terms, and many pay off before maturity).

Compare that to, say, a fund-of-funds investing in secondary PE stakes: virtually no yield, minimal organic portfolio turnover. The asset-liability mismatch is far worse.

Compare to this fund, for example:

Or this one:

And yet even in the best case, the structure has a game theory problem.

The game

Every quarter, each adviser independently chooses: hold or redeem.

The outcomes depend on what everyone else does, but there is only one rational course of action: