When the Denominator Wins

UNREAL Gains, Part 2: how mature evergreen secondaries funds slowly outgrow the mechanism that built their track records

In Part 1, we looked at how evergreen secondaries funds generate enormous early-stage returns through a surprisingly simple mechanism:

Buy secondary interests at a discount

Mark them immediately to sponsor-reported NAV under ASC 820’s practical expedient (Day One mark-ups)

Report the unrealized gain before a single company exits

(Collect fees on it too, in some cases).

Here’s Part 1, ICYMI:

The economics in the early years can be extraordinary. When a fund has only a few hundred million in assets, every new secondary purchase meaningfully moves the NAV.

But there is a problem embedded in the structure itself: eventually, the denominator gets too large.

The same $7.5 million instant mark-up that once generated a multi-percentage-point return barely moves the needle once the fund grows past a billion dollars in assets.

So what happens then?

Well, the logical place to look is mature evergreen secondaries funds. The trouble is, our pickings are slim (which made my job easy: there are only a handful of such funds older than 6 years). I picked one early vintage secondary fund with over $1B in assets:

Pomona Investment Fund, launched May 2015, and now ~$1.9B in assets (88% allocation to secondaries as of December 2025).

“Leyla, what in the world are you talking about?” Here’s your primer on evergreen secondaries:

👉 Want some case studies on secondaries evergreens? Here’s Coller Private Credit Secondaries (LINK), Carlyle AlpInvest (LINK) and Partners Group Next Generation Infrastructure (LINK).

The machine still runs

To isolate the effect, I separated all new acquisitions in each reporting period from the performance of the existing portfolio and calculated Day One mark-ups on entry (and by “on entry” I mean in the same reporting period).

Average same-period mark-up on all new secondaries purchased during 2024–2025: ~28%.

Yes, this is an unnecessarily tedious exercise, even if you outsource the tedium to an LLM. And yes, the estimate is derived by comparing initial cost basis to reported fair value in the first filing period for each position, and I ignore some nuances. It is imperfect, but gets us in the ballpark. (If you object, I’ll beat you over the head with a Warren Buffett quote about decimal points).

No, Pomona didn’t make it easier by reporting cost basis neatly. I had to reconcile it from footnotes. This is how it’s reported (I’m going to call out every fund that does it like this. There is no excuse):

Pomona itself reports an average purchase discount of ~21% since inception. If anything, there is an argument for wider discounts in recent periods (rates are higher, more sellers seeking liquidity, etc).

Nothing surprising here, of course: a decade into the life of the fund, newly acquired secondary interests are still being marked up meaningfully and almost immediately after acquisition. And ASC 820 continues to allow that mark-up to flow directly into reported performance.

Here’s a case study on a newer secondaries fund:

But there is a structural difference between a $300M evergreen fund and a $1.9B evergreen fund:

the mark-up may be the same. The denominator is not.

When the fund was small, a single discounted secondary purchase could meaningfully move reported returns. At scale, the exact same economics become diluted across a much larger asset base.

And meanwhile, the existing portfolio keeps aging.

Those older positions are no longer generating fresh Day One mark-ups. They are gradually transitioning into harvest mode: underlying PE funds sell companies, distribute cash, and convert prior unrealized appreciation into realized returns.

Before we get too far in the weeds, I need to remind you that assets in these funds are very illiquid, but the structure allows for periodic redemptions. Read this:

The denominator problem

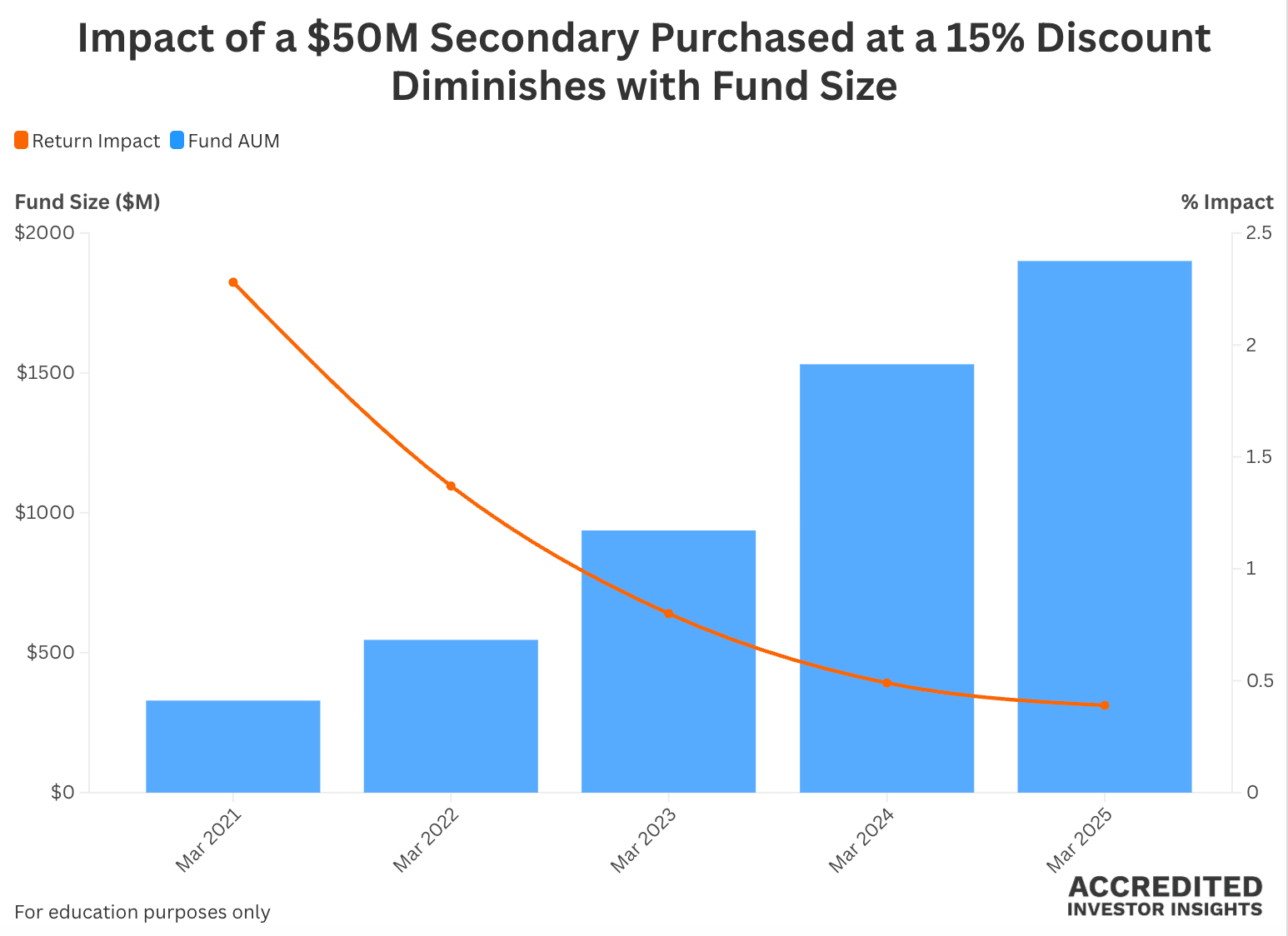

Let me first illustrate the denominator effect broadly.

Take a $50M secondary purchase at 15% discount (it’ll generate $7.5M in Day One unrealized gains). Here is what that same transaction contributes to Pomona's reported return at different fund sizes:

This is the denominator problem in its simplest form: as fund assets grow, each new mark-up contributes a smaller percentage of total NAV.

The rational response?