Private Equity Won't Sell | Private Credit Won't Sit Still | Data Centers Won't Slow Down

🗞️ Sunday digest: private markets insights 7/12

Happy Sunday!

Every other week, we send a quick digest on what’s catching our eye across private markets.

Today’s lineup:

1️⃣ Private equity: valuations vs exits

2️⃣ Private credit: retail wants out, institutions want more

3️⃣ Commercial real estate: data centers

🎁 Bonus: a report on evergreens and secondaries

Before we dive in:

Accredited Insight delivers the LP’s perspective on private credit, private equity, and CRE, drawing on hundreds of deals, and thousands of conversations. Paid subscribers gain access to our database of over 40 case studies and articles on everything from evergreen funds to due diligence (the kind of analysis that tells you what the GP pitch deck left out).

1️⃣ Private Equity

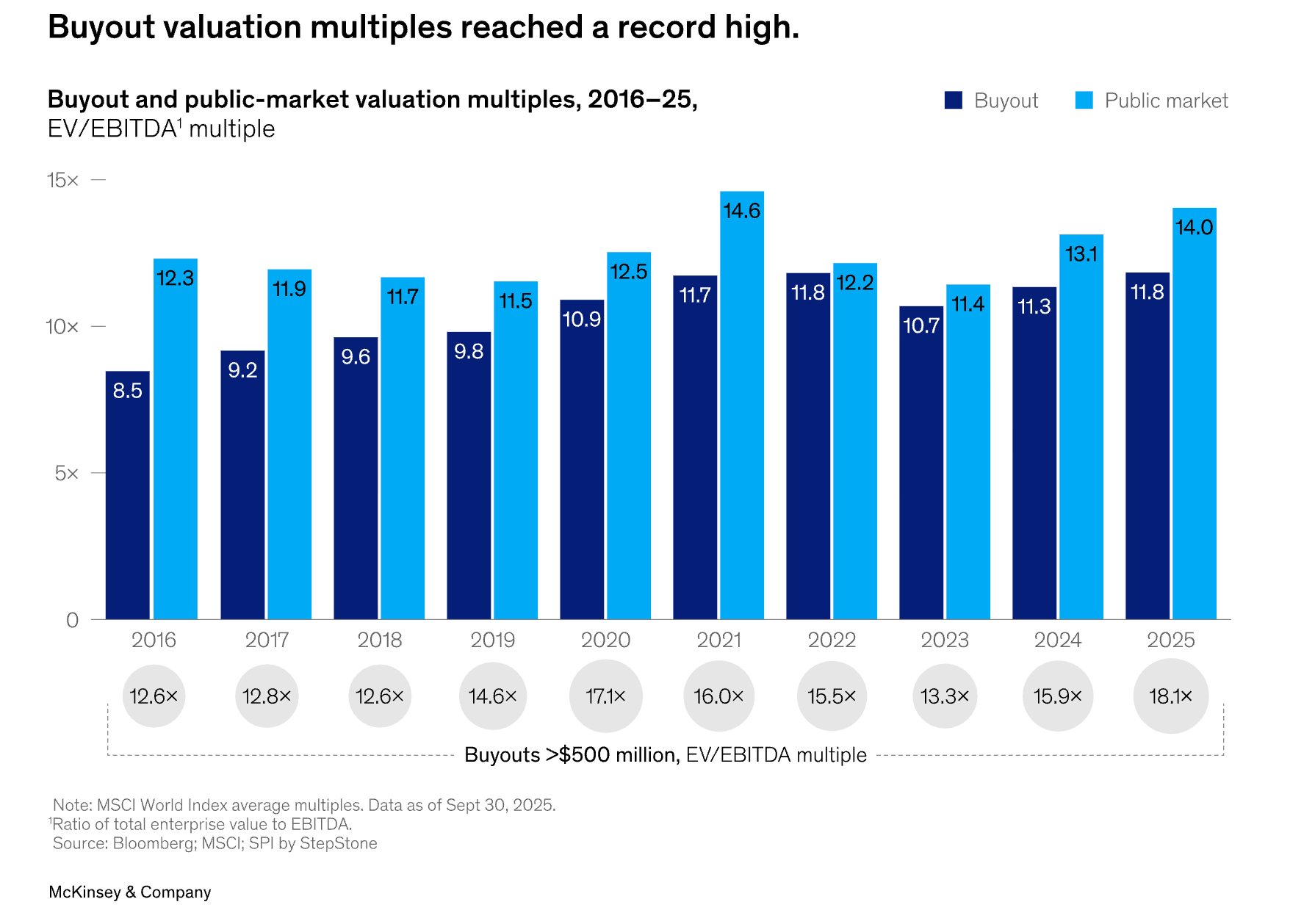

Chart of the week, right here:

You are looking at buyout valuation multiples (the multiple of EBITDA private equity sponsors pay to acquire a business). The multiples are near the 2021 record high. What has happened since 2021? Rates have gone up substantially, which makes leveraged buyouts more expensive to buy. And yet, entry multiples keep climbing.

What separates great sponsors? Operational acumen:

And here’s Part 2:

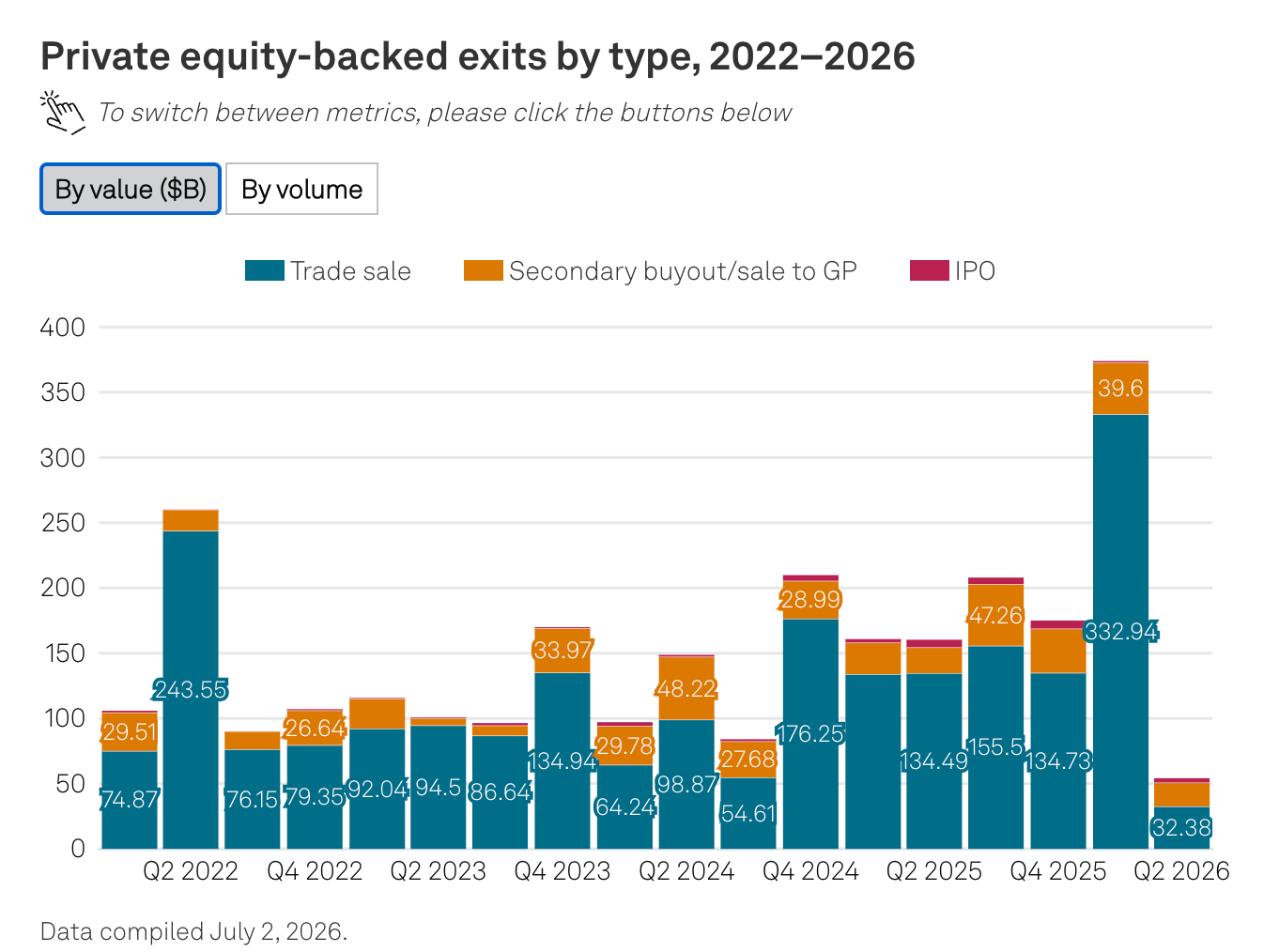

The other side of the ledger tells a different story: more than 16,000 companies globally have now been held for over four years (also a record!) That’s 52% of all buyout inventory.

Exits were up by volume in 2025, but largely due to gigantic IPOs. Smaller portfolio companies are being held on to and maturing like … (A. fine wine; B. milk?)

And here’s why you probably don’t want exposure to earlier vintage assets (unless you get them at a sizable discount):

2️⃣ Private Credit

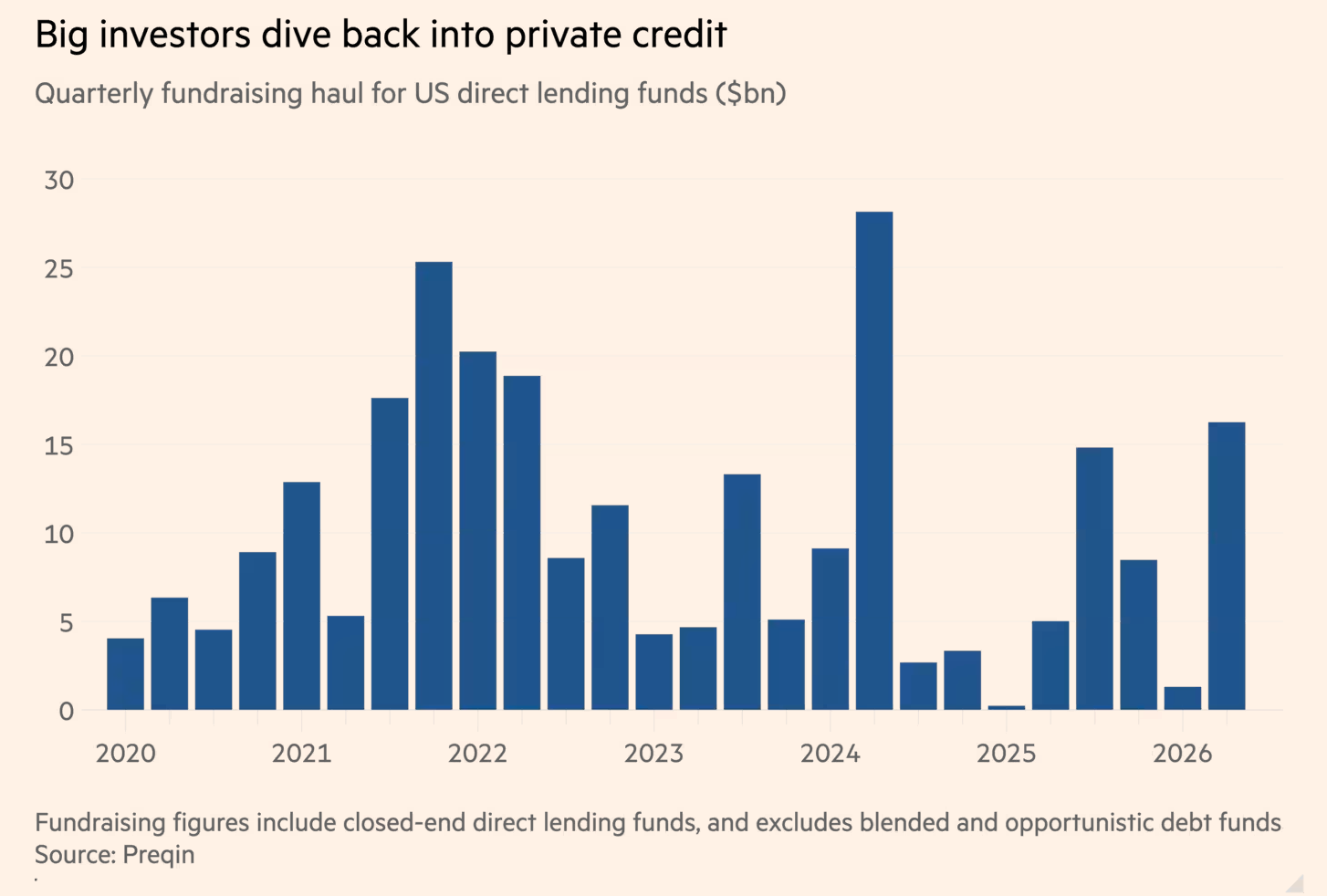

1. Institutions are doubling down

While retail clients head for the exits (here’s a great article on the subject of redemption queues and how the math works), institutions are doubling down. North American direct lending funds raised ~$16B in Q2 (the second-strongest quarter in four years).

What’s attracting investors? Wider spreads, tighter docs, and higher rates. Keep in mind, most of this capital was committed to drawdown funds, meaning it won’t deploy immediately. How much of the sales pitch centered on expected distress, folks?

2. On investor concentration

Speaking of retail investors heading for the exits, in late 2025, UBS advised clients to reduce private credit exposure. Turns out, 60% of Blue Owl Technology Income Corp. (OTIC) had reportedly been raised through UBS clients (FT).

When a single distributor represents that much of your investor base, a change in allocation guidance turns into a redemption problem.

Guess what? As an outside investor, you usually have no way of knowing how concentrated a fund's distribution channels really are. Something to ponder for your next allocation…

And here’s how this is playing out:

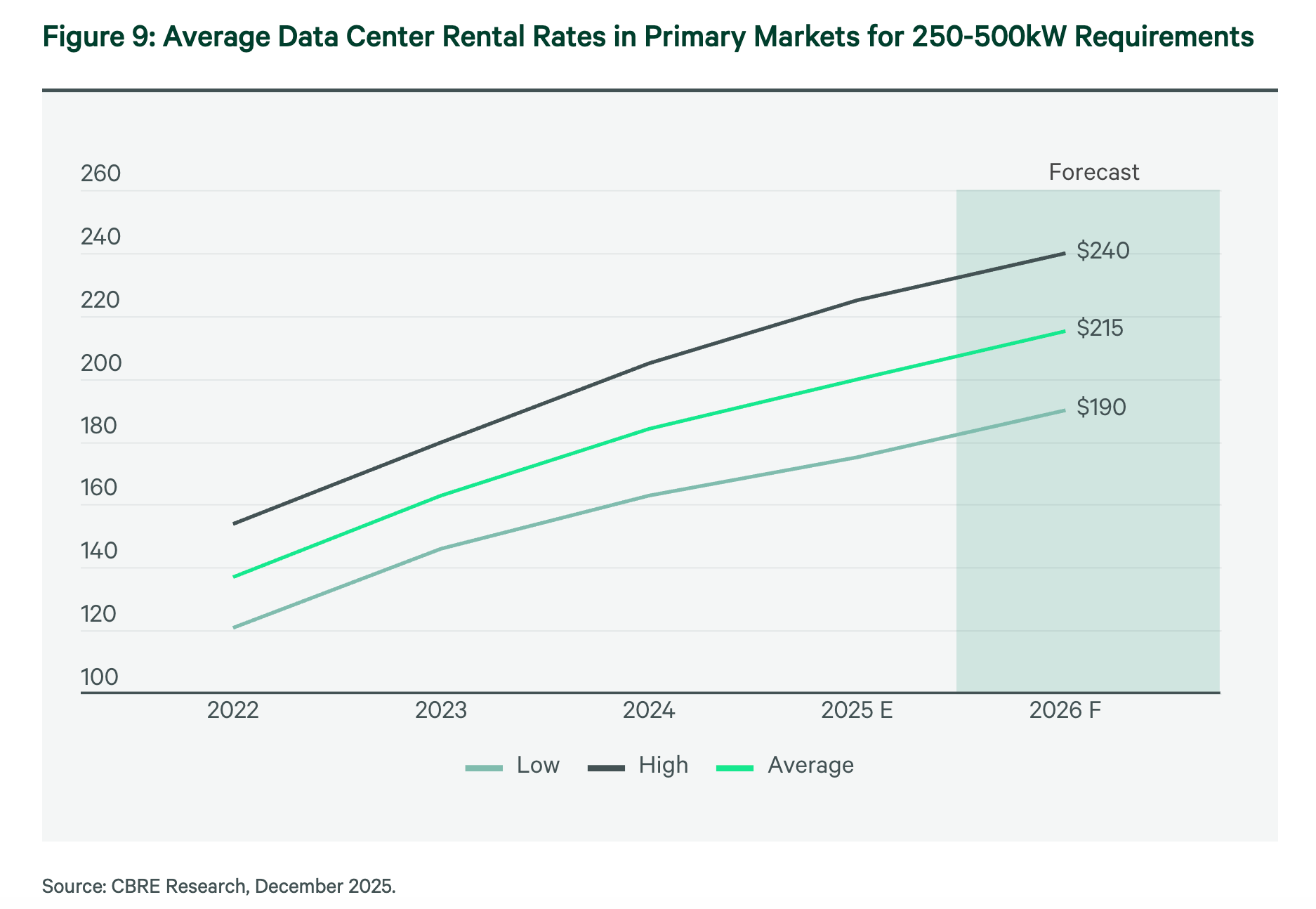

3️⃣ Commercial Real Estate

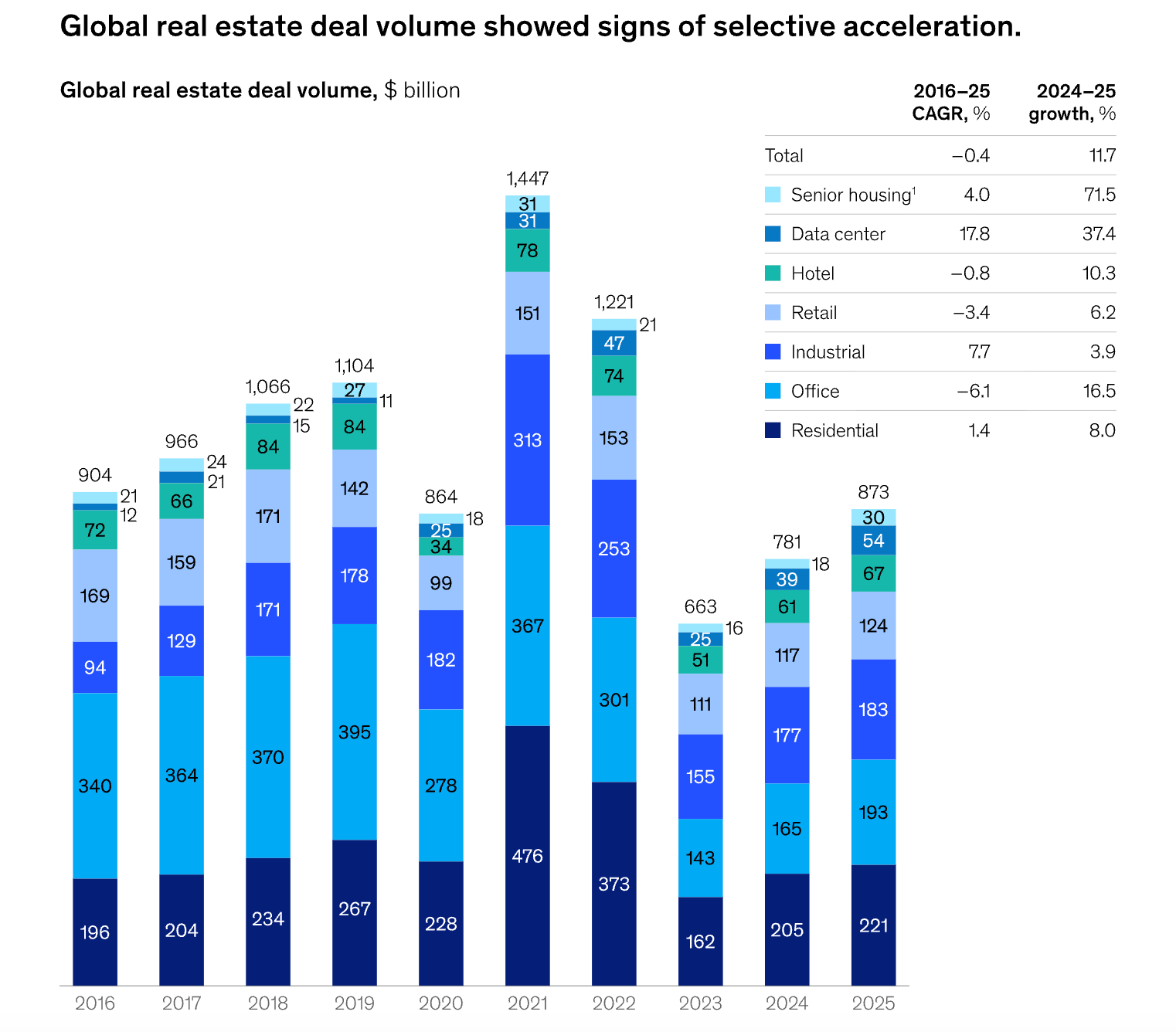

Data centres are the new darlings (“Duh, Leyla”)

Data center deal volumes surged 37% in 2025 (McKinsey). It is now the fastest-growing segment globally. The capex story is massive: $3T in infrastructure needed by 2030, 100 GW of new capacity, $1.2T in real estate value creation.

👉 Here’s a fund that’s deploying into this space:

The constraint is power. Sites that can deliver 300+ MW in under 36 months now outrank pure connectivity plays. As a side note, regulatory and community delays have killed $64B in US projects since 2023.

I’m not nearly smart enough to call the top in data centers, but here’s what happened to a fund that bought a bunch of CRE at the peak:

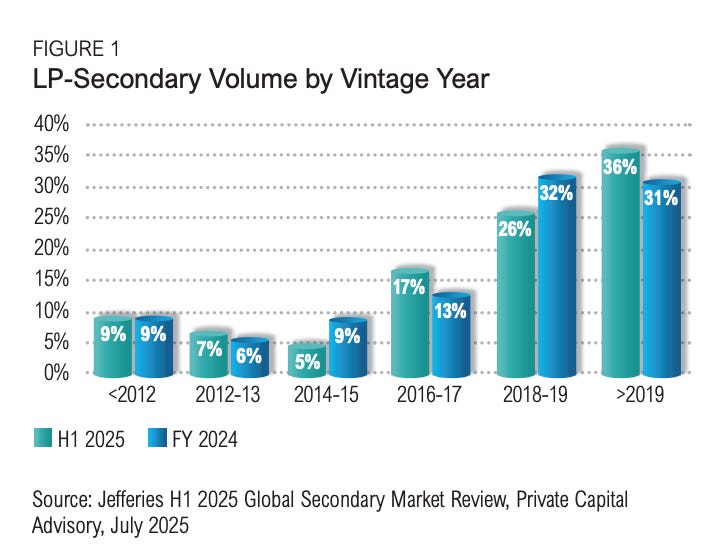

Secondaries

Meketa's latest paper on secondaries highlights many issues we've flagged: NAV-squeezing, inflow-driven returns, and evergreen fund misuse of secondaries as a liquidity crutch.

Here’s how that works in the early years:

And what happens when a fund matures:

Interesting chart from the paper: in H1 2025, over 20% of secondaries volume was vintage 2015 and older. Stale assets, trading at a discount, being stored in fresh vehicles.

Thanks for reading! As always, if you have any suggestions, reply to this email, leave a comment, or find me on socials (unhinged me on X, slightly more filtered me on LinkedIn)

-Leyla

P.S. New here?

Here’s where you’ll find the full archive (somewhat organized):

It seems clear to me that those projections for data center growth are overly optimistic and highly uncertain. There is a lot of FOMO by the hyperscalers and others going on; they seem to me to be unlikely to miss out on the crash.

The PE chart and the exit gridlock tell the same story from opposite sides. Multiples stay near 2021 highs because nobody is selling. Nobody is selling because transacting at a lower multiple would crystallise a loss the quarterly NAV hasn't acknowledged yet. The 16,000 companies held for 4+ years aren't maturing. They're waiting. And the longer they wait, the wider the gap grows between the mark on the books and the price a buyer would actually pay.

The UBS/Blue Owl concentration stat is the quieter bomb. 60% of a fund raised through one distributor, and that distributor changed its allocation guidance. When a single channel controls that much of your capital base, a portfolio rebalancing memo becomes a redemption crisis. And as an outside investor, you can't see the concentration until it's already a problem. That's the opacity that makes private markets private.