Don't Buy Yesterday's Portfolio

In private markets, the question isn't whether an asset is good or bad. It's whether it was acquired in 2022 or 2026.

The number one question I get is: “Leyla, what are compelling investment opportunities right now?”

Before I launch into my thoughts, the usual reminder: my mission is to make you a better investor by telling you how the sausage is made (teach the man how to fish, and all that). It’s not to tell you which funds to put your money into (you have an adviser for that, share this article with them).

What follows is emphatically NOT investment advice, and like Vincent Vega in Pulp Fiction, I won’t show you exactly what’s in the suitcase. But I hope you are happy (you can make me happy by subscribing below).

Personally, I don't see many obvious bargains today. The opportunities I do see generally fall into two buckets: assets that have already repriced and managers deploying fresh capital into today's market rather than managing yesterday's mistakes.

I'll show you what that looks like across private equity, private credit, and real estate.

If you want some case studies on actual funds, here are a couple to get you started (one private credit, one private equity):

Nothing contained in this newsletter constitutes investment advice, a solicitation, or an offer to buy or sell any security or investment product. The views expressed are those of the author alone and are for informational and educational purposes only. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal. Please consult a qualified financial adviser before making any investment decisions.

Private Equity

Quick recap of our prior episodes:

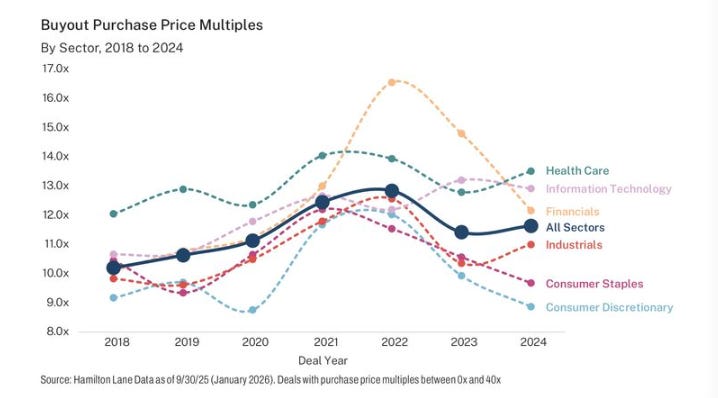

Over the past decade PE funds raised enormous amounts of capital and rapidly deployed it. A lot of that capital went into software, healthcare, and fintech at double-digit EBITDA multiples.

The problem is that those multiples haven’t come down much (while rates increased). Across most industries, things are still expensive and marks on existing investments have barely moved. PE in general is not cheap.

👉 A hill I will die on: basis is the best predictor of future outcomes. Buy something cheap, and you have more upside. Buy something expensive, and you’re depending on multiple expansion or operational miracles to bail you out.

So where does that leave you?

Primary funds

If you're allocating to a new primary fund, you want a specialist GP: someone who knows one industry deeply and buys deals only in that industry.

And here’s why: generalist GPs are competing with everyone else for the same assets, and they're still paying peak multiples to win. Specialist GPs in less-trafficked sectors are likely seeing less competition and possibly buying at meaningfully lower entry points (goes without saying, do your DD).

📌 You want fresh deployment, and a GP with extensive experience in one sector. These managers exist, but they're harder to find than the marketing decks suggest.

Secondaries (drawdown funds):

Well-capitalized secondaries buyers are going to have real opportunities to acquire good assets at a discount. The supply of motivated sellers is growing: LPs who over-allocated in 2021-2022 need liquidity, distributions are near historic lows, and the exit environment has been slow. Find the GPs with capital ready to deploy into that dislocation.

⭐️ Secondaries (evergreens):

I’ve written extensively about how evergreen secondaries funds work, so I’ll be brief. The game here is simple once you see it: you want to be the first dollar in, ideally in a fund that will deploy a significant portion of its NAV in the period immediately following your investment.

Here’s how the mechanics work:

A simple example: say a fund has deployed $3B between 2021 and 2023. The underlying assets haven’t been marked down much (private valuations are a work of art). You invest today at stated NAV. But stated NAV reflects assets that were acquired at peak multiples, and the discount on acquisition is already reflected in the NAV you paid.

And guess what? If there is a markdown, you’ll ride it down despite not being there to bask in the glory of unrealized gains.

More on the topic here:

By contrast, if you’re among the early investors in a newer vehicle that’s actively deploying fresh capital into today’s deals, you get to participate in what’s affectionately known as “NAV-squeezing”. The math is straightforward. Be dollar number 1. Don’t be dollar number $2,389,098,357.

Here’s a case study on a mature PE fund (according to FT, redemptions are likely to be capped):

‼️ Again, not investment advice, but "In-N-Out" appears to be quite a strategy with new evergreen secondaries: be the first dollar in, and among the first dollars out, while the fund is rapidly deploying fresh capital and marking positions up. The window between early deployment and portfolio maturity is where outsized returns are.

Private Credit

The golden child of alts has handed the baton to infrastructure, but it is throwing a fit on the way out (like a toddler).

A quick note: “private credit” is a broad term. It means loans originated outside the banking and public markets ecosystem. This is anything from commercial mortgages to BNPL burrito loans. The vast majority of what’s available to individual investors is middle-market direct lending: loans to privately held companies, typically originated by PE sponsors to finance acquisitions. That’s our focus (if you ask nicely, I’ll write a primer on all the different flavors of private credit).

On prior episodes:

Boatloads of capital were raised between 2020 and 2025 and got deployed.

The borrowers look a lot like the PE darlings above (software, healthcare, fintech). That’s because PE bought those companies and saddled their balance sheets with acquisition debt.

The official default numbers are still low, and loan valuations are holding. But the cracks are showing: PIK income is up as a percentage of total income, some funds are quietly taking markdowns, and several interval funds have hit their redemption caps.

It’s still TBD whether the losses ultimately materialize. Public investors, however, are clearly demanding compensation for the possibility:

Here’s a case study on how markdowns work in financial statements:

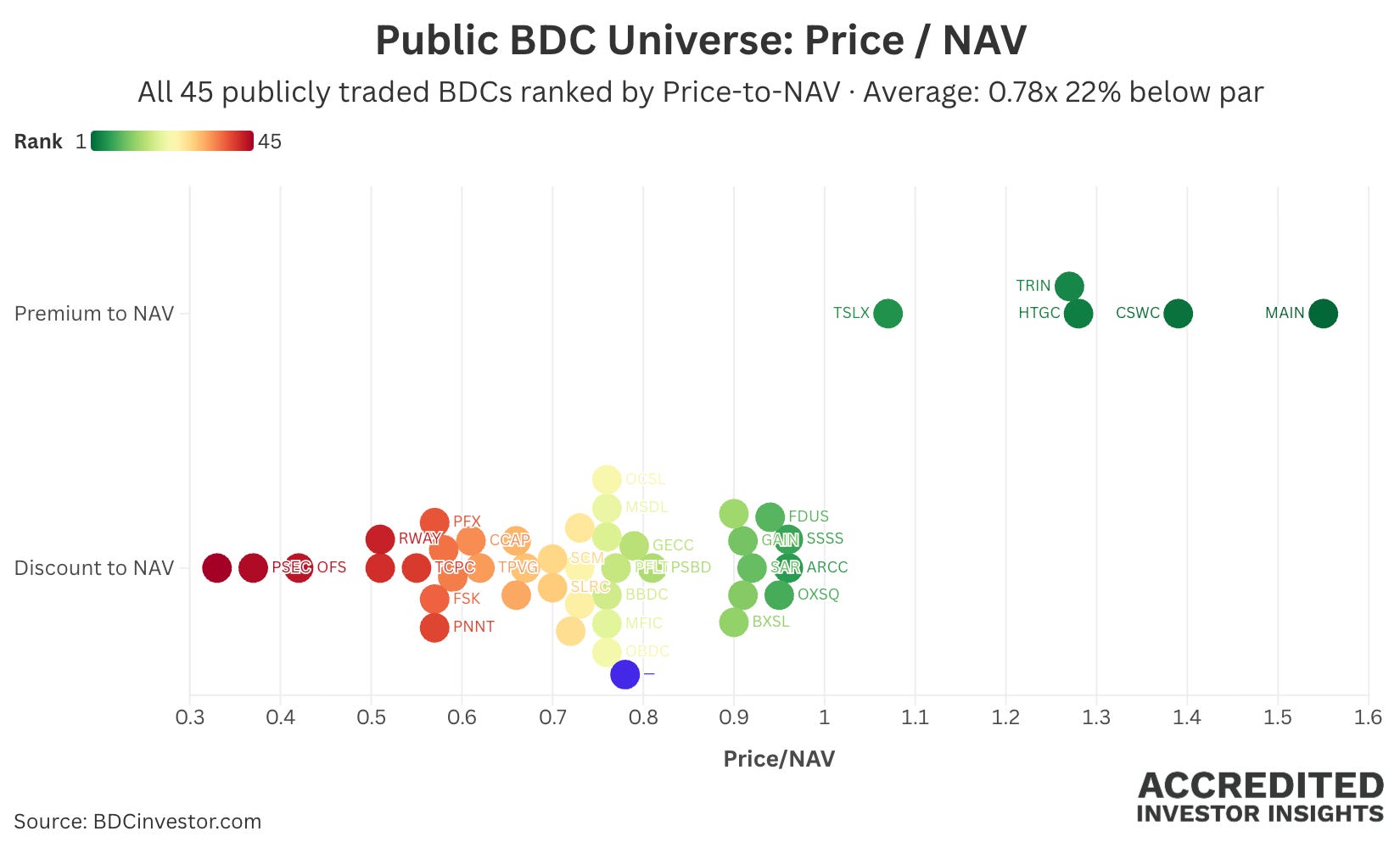

👉 Which brings us to the trade. Most public BDCs now trade at a meaningful discount to NAV (the sector average is around 0.78x, meaning you’re buying a dollar of private loans for roughly 78 cents). Non-traded private credit vehicles are still redeeming at NAV. Well, the ones that are still redeeming, that is...

So the trade is: redeem at NAV from the non-traded vehicle, and buy the same underlying exposure in the public market at a discount.

⚠️ BUT (you knew it was coming, didn’t you?) you want to make sure the discount is sufficient for the 2021-2023 vintage exposure. Those portfolios were underwritten at peak, to borrowers carrying heavy leverage, in sectors that are now under pressure. The discount might look attractive, but you could be buying into a NAV that hasn’t finished correcting.

What you want instead is a public BDC with: post-2023 vintage originations, a first-lien heavy portfolio, low non-accruals, and ideally an internally managed structure (which better aligns manager incentives than the externally managed alternative). Think of the discount as your margin of safety, not necessarily upside.

A second option worth watching: drawdown distressed debt funds. Several are actively raising right now, and they’re positioned to buy portfolios of good-quality loans at a discount (potentially from the same evergreen vehicles that are currently working through redemption caps).

Real Estate

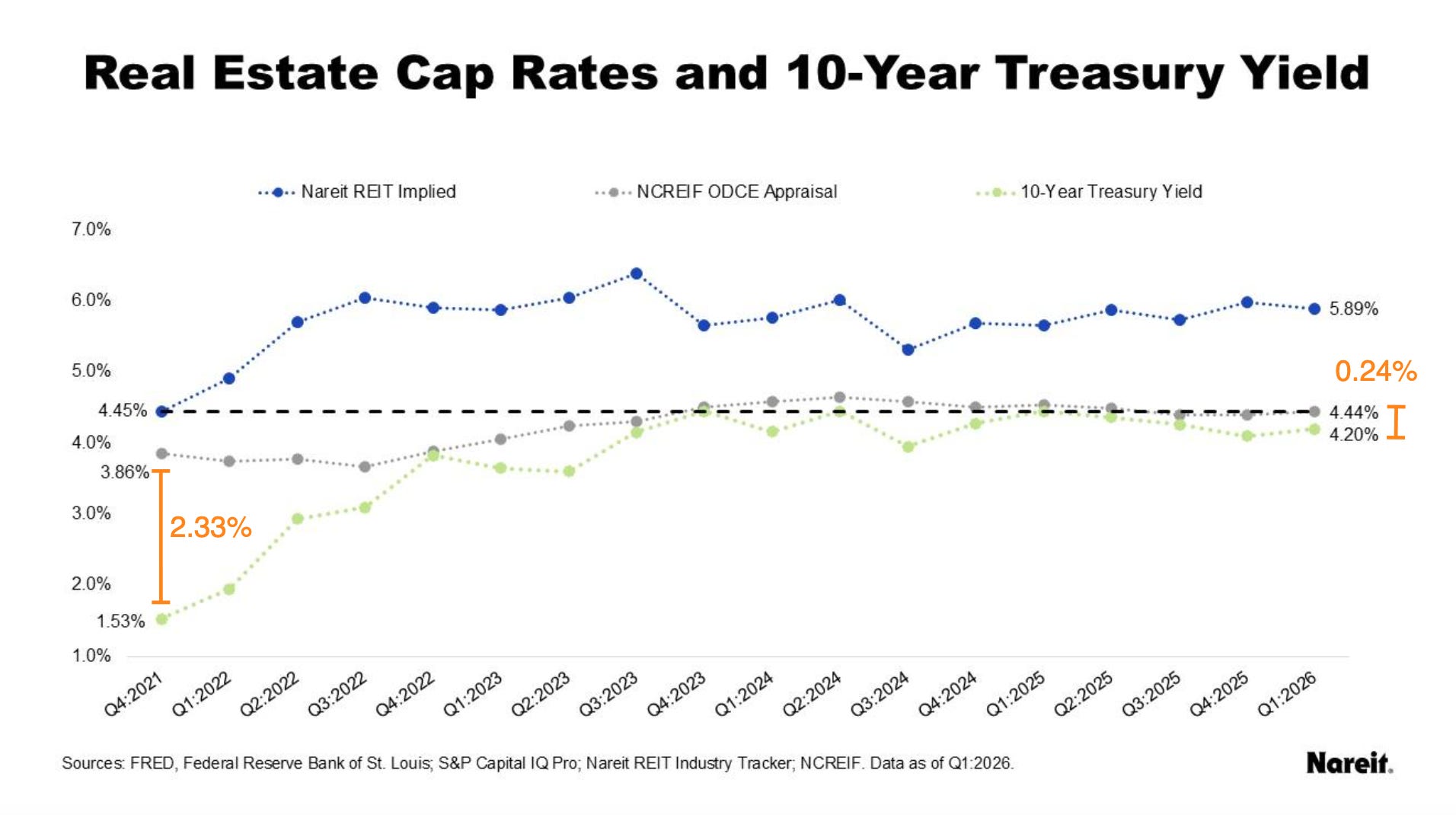

Look at the chart below and focus on the two ends: Q4 2021 and Q1 2026.

Q4 2021: peak FOMO (=fear of missing out). Multifamily deals traded at 4% cap rates, deals attracted 45 bids, and long-term financing rates were low enough that the math still penciled (for those who elected long-term financing). Many of those deals were financed with floating-rate bridge debt, which at the time seemed fine.

Between then and Q1 2026, the 10-year Treasury yield rose by nearly 3%, but core private real estate cap rates, as tracked by NCREIF’s ODCE index, rose by less than 1%.

Put differently: the cost of financing real estate went up sharply, but the price of real estate barely moved.

Public REITs, by contrast, repriced in real time. Implied cap rates on listed REITs rose from around 4.45% to nearly 6% over the same period (blue line in the same chart). And public REITs, importantly, carry lower leverage and lower cost of capital than most private deals.

Don’t know what a cap rate is? Read this:

What to avoid: existing private real estate fund portfolios, particularly non-traded REITs with large legacy 2021-era acquisitions on the books. Those assets are still marked near peak. Did you see my point above about the cost basis? With redemption queues, some of those vehicles don’t have the luxury of deploying new capital.

What’s more interesting:

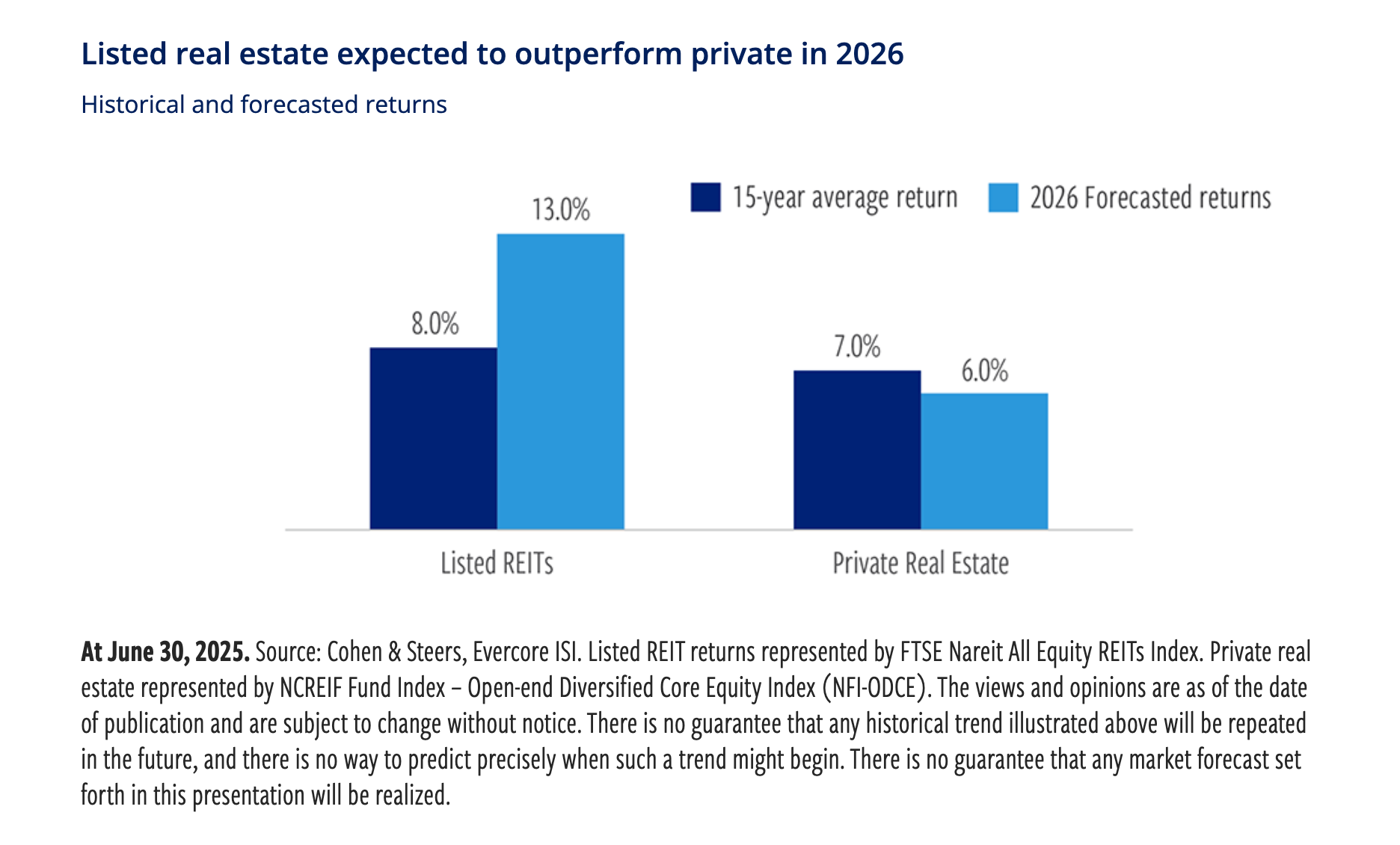

Listed REITs: you can enter at meaningfully higher implied cap rates than the private market is offering for comparable assets. Yes, there is little love for listed REITs; there should be even less for their non-traded counterparts.

What else is interesting:

Private value-add deals: good value-add opportunities are few and far between, but they exist. There will be some forced sellers: for example, some over-levered 2022 deal with the lender finally throwing in the towel. (The ones we’ve seen so far were not screaming bargains). Either way, don’t expect high current cash flow. You’re buying for basis and exit multiple, not yield.

Off-the-beaten-path locations and asset classes: higher on the risk spectrum, but should offer higher expected returns. Again, experienced specialist GPs will likely outdo generalist GPs.

If you are dead-set on allocating to core CRE, new drawdown funds is where I’d focus.

Here’s a case study on a newer secondaries fund:

TL;DR

The common thread is the vintage.

Today, I think vintage selection matters almost as much as manager selection (this, obviously, only applies to evergreen vehicles). In many corners of private markets, the question isn’t whether an asset is good or bad. It’s whether it was acquired in 2022 or 2026.

That’s an oversimplification, of course. But if I had to summarize what I’m paying attention to today, that’s probably the closest thing to a north star.

Thank you for reading!

As always, feel free to share your ideas in comments (feel free to argue, too! I like a lively discussion)

— Leyla

Also, it seems that the whole world looks at that cap rate plot and concludes that listed REITs are undervalued. To my mind the correct argument runs the other way. It is PE that needs to correct. Plus, if you look at the 75 year record, you can make a good case that the listed REITs are still overvalued.

RE: PE bought those companies (software, healthcare, fintech) saddled their balance sheets with acquisition debt.

This is what PE did with retail chains through the Great Recession. That worked out for a few years, but by the late 2010s those debts pushed many of them into Ch. 11 or worse. The incorrect media narrative was that retail was devastated by e-commerce. That was never correct. Retail was devastated by PE.