Private Equity Wants Your Financial Advisor, Private Credit Wants More Time, and CRE Wants a Miracle

🗞️ Sunday digest: private markets insights 5/17

Happy Sunday!

Every other week, we send a quick digest on what’s catching our eye across private markets.

Today’s lineup:

1️⃣ Private equity: PE firms are now buying the firms that sell you PE; meanwhile, retail appetite for their evergreen vehicles is quietly cratering

2️⃣ Private credit: valuations being investigated by regulators; BDC redemptions exceed new capital raised for the first time in history

3️⃣ Commercial real estate: fundraising returned (just not to the funds that need it most); and the era of "extend and pretend" is officially over, with lenders finally eating the loss.

Before we dive in:

Accredited Insight delivers the LP’s perspective on private credit, private equity, and CRE, drawing on hundreds of deals, and thousands of conversations. Paid subscribers gain access to our database of over 40 case studies and articles on everything from evergreen funds to due diligence (the kind of analysis that tells you what the GP pitch deck left out).

1️⃣ Private Equity

1. PE Eats Wealth Management Firms

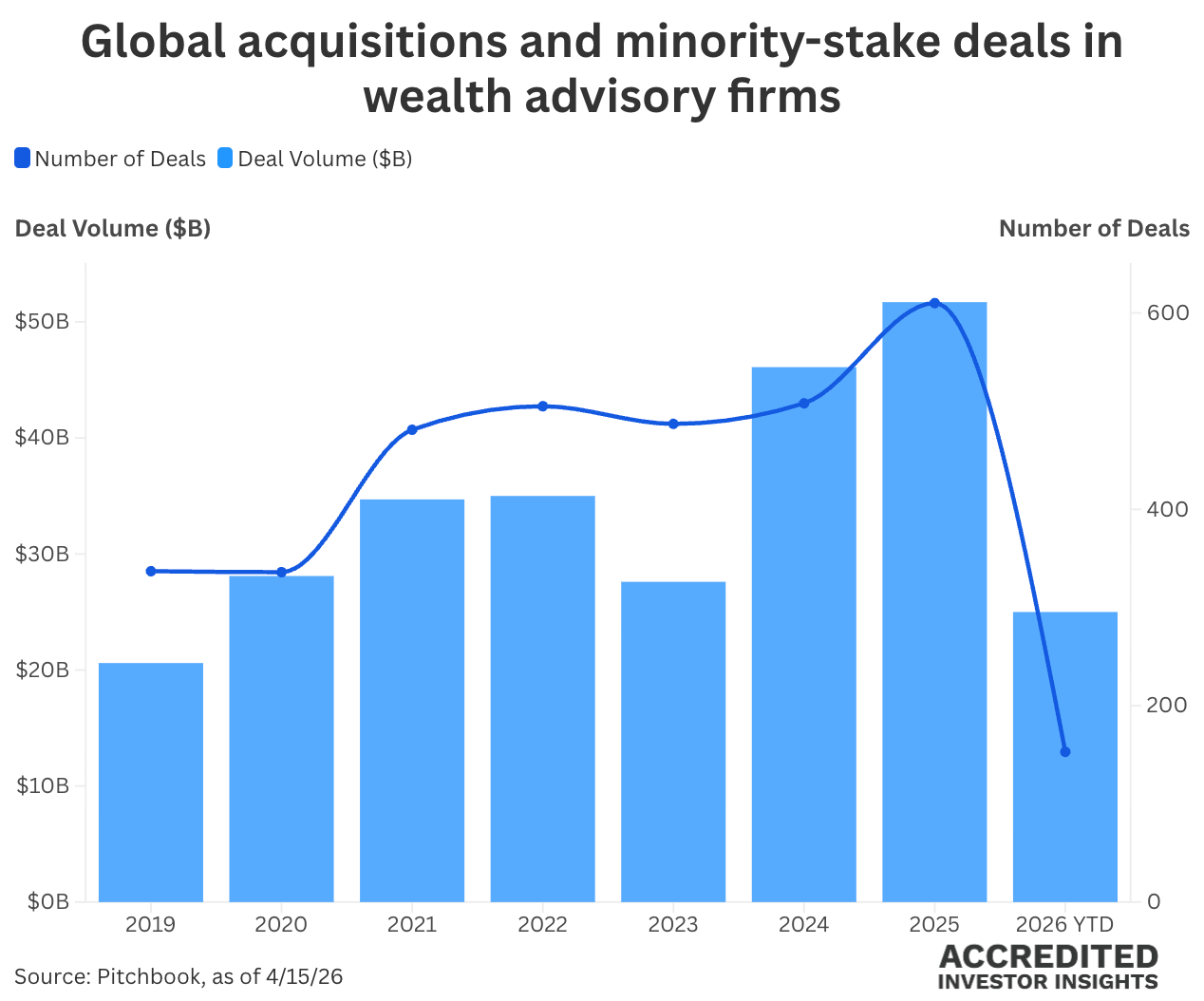

The natural progression of “democratization of alts”: wealth management firms are being acquired at breakneck pace by (you guessed it) private equity firms. The people selling you access to private equity now belong to private equity. Fees all the way down.

Carlyle’s deal to take majority control of MAI Capital at a $2.8 billion valuation is the latest example of private equity moving deeper into the RIA channel. The trend is driven by:

a massive wealth transfer,

institutional fundraising fatigue (side note: if institutions are fatigued, how good is it for retail, but I digress),

soaring demand for alts from high-net-worth investors.

According to Pitchbook, deal activity hit record levels in 2025, with RIAs, private equity firms, and sovereign wealth funds all competing to build scaled wealth platforms tied to private market distribution.

And what exactly are these retail investors being sold? Evergreen funds.

2. Evergreen Fundraising is Slowing Down

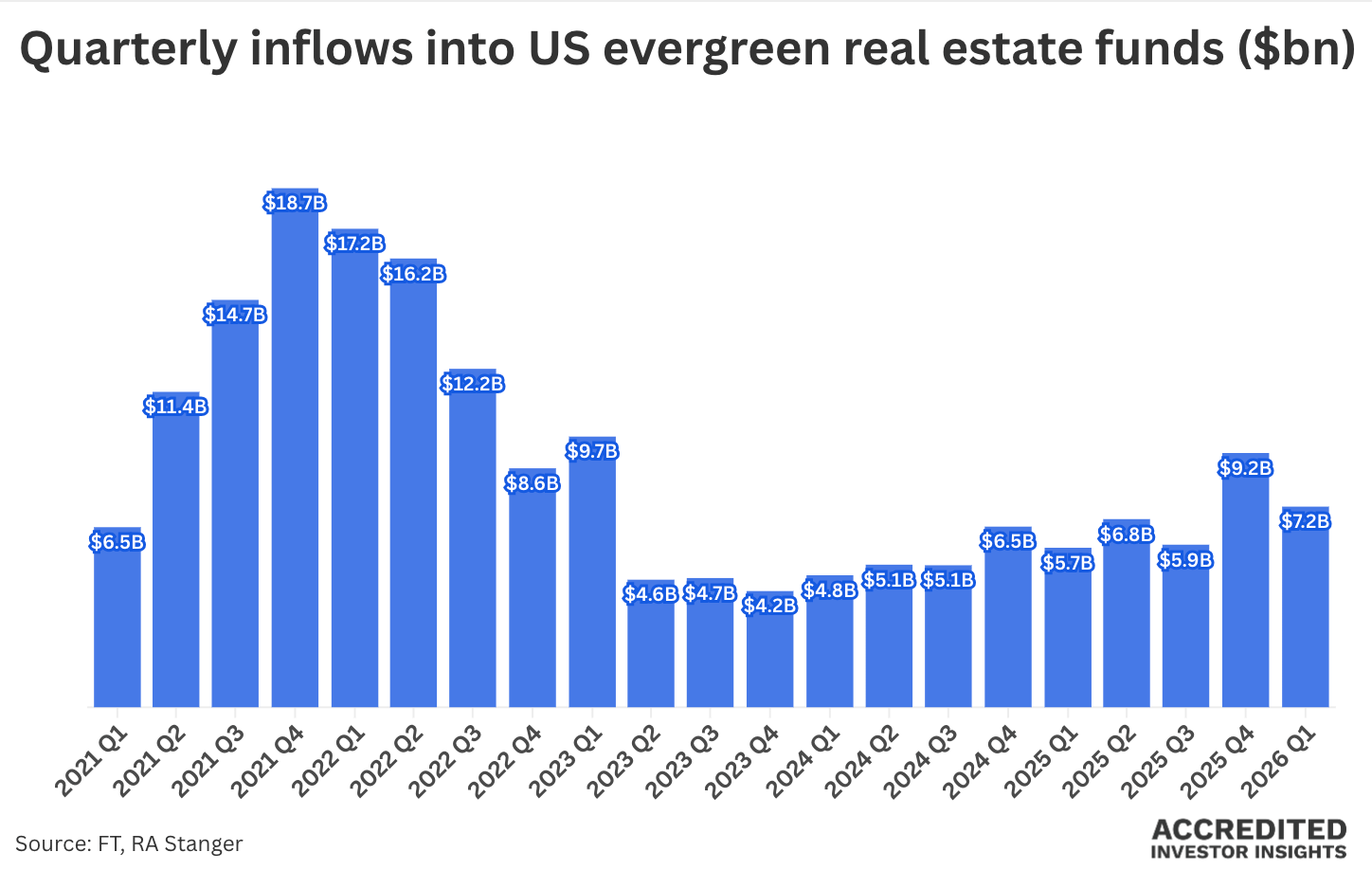

And speaking of evergreens, retail appetite for private equity evergreen vehicles is rapidly cooling (FT). The headlines have focused on private credit (more on that below, at length), but private equity has not been spared.

Quarterly inflows into U.S. PE evergreen funds have stalled after a sharp run-up through mid-2025.

👉 If retail sentiment on PE evergreens continues to sour, the liquidity mismatch in PE vehicles could make the BDC drama look like a Sunday picnic. Here’s why:

📌 Leyla’s notes:

Personally, I’d want my advisor’s ownership structure to be clearly disclosed. PE ownership is not a red flag in and of itself, but there are unquestionable conflicts of interest.

Watch liquidity in evergreen vehicles, especially when the underlying assets don’t generate enough cash flow to meet redemptions. You want to be early in the queue, if liquidity is of concern (and if it’s not, you might be better off in a traditional drawdown vehicle).

2️⃣ Private Credit

1. Valuations Under Fire

Federal prosecutors are reportedly investigating valuation practices at BlackRock’s TCPC private credit BDC, according to Bloomberg. This follows a disclosure earlier this year where the fund warned it would mark down its net asset value by roughly 19% (this sent shares down 13% in a day and triggered investor lawsuits over alleged misstatements around loan valuations).

👉 We covered TCPC's deteriorating fundamentals back in April (before the DOJ news broke). Here’s the non-accrual story:

Let me get back on my soapbox about valuations in private credit: when 100% of your portfolio is Level 3 (meaning zero observable market prices), an "independent valuation" simply means independent people making educated guesses based on assumptions you gave them.

Here’s a great WSJ article on the subject, with some examples from OBDC’s schedule of investments.

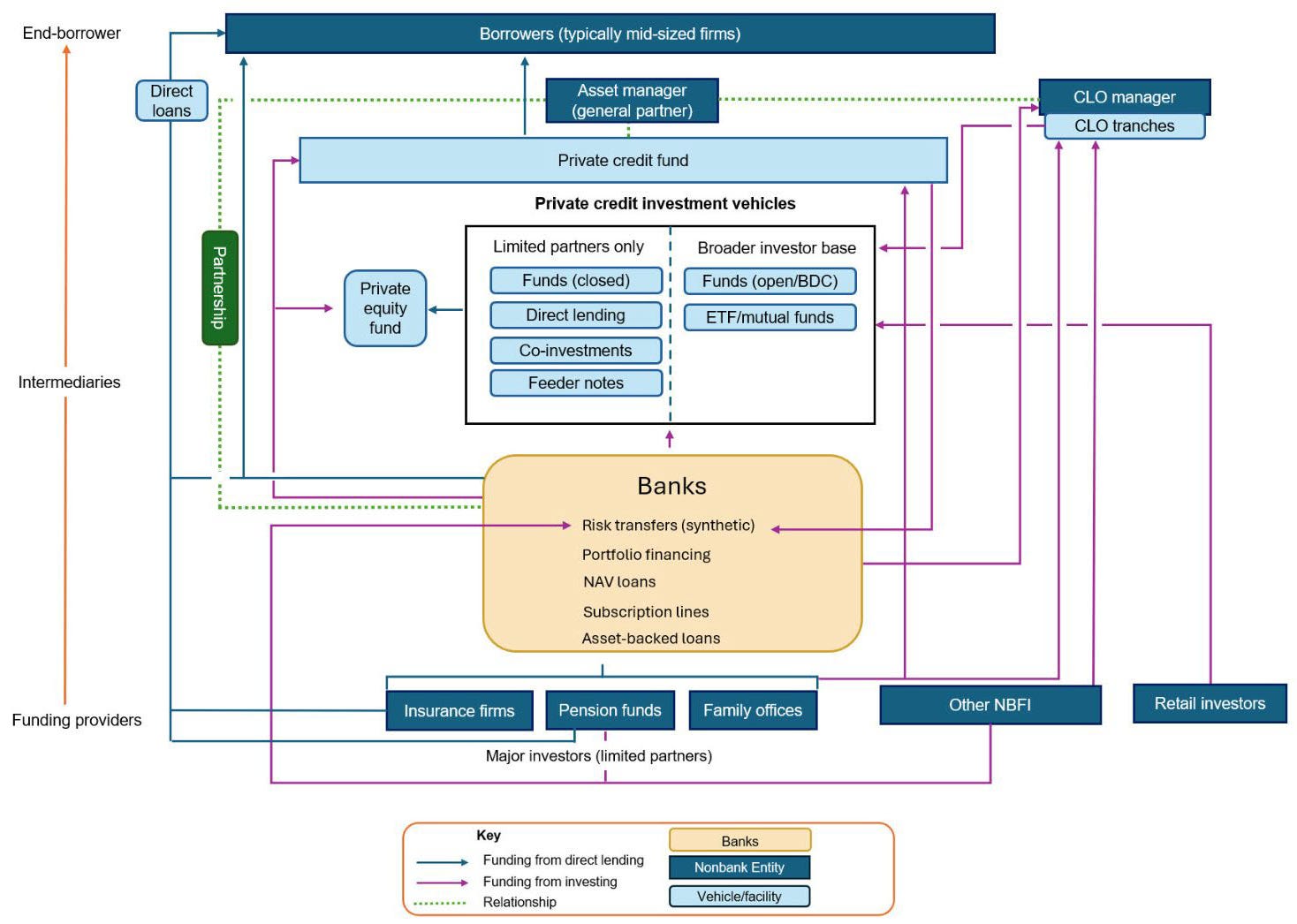

The Financial Stability Board published a report on private credit vulnerabilities. Their key concerns include:

Deepening bank-to-non-bank connections (estimated exposure: $220B – $500B).

Deteriorating borrower credit quality.

Heavy sector concentration (especially in tech and healthcare).

Severe structural liquidity mismatches.

Look at this beautiful, interconnected ecosystem:

Outflows

Non-traded BDCs handed back more capital than they raised in Q1 2026, the first time in recorded history outflows exceeded inflows in the structure (Bloomberg).

Non-listed BDCs fulfilled ~$7B in redemption requests while raising only ~$5B in new capital, a $2B net outflow. But the $7B number is only part of the story: total Q1 redemption requests across U.S. private credit semi-liquid vehicles reached ~$15B, with several flagship platforms capping redemptions.

Here’s a look at one of the largest funds, with 14% of fund’s shares requesting redemptions:

BofA thinks the worst of the redemption wave may have hit in Q1, but Q2 could still be rough for several non-traded private credit vehicles (Pitchbook):

Apollo Debt Solutions is projected to see redemption requests climb to 15% of shares outstanding in Q2 (vs. 11.2% in Q1),

while Ares Strategic Income Fund could rise to 14% (vs. 11.6%).

BCRED continues to look relatively stronger than peers: it had the lowest Q1 redemption requests among the major private BDCs tracked by the bank at 7.9%, and was the only large vehicle that did not gate withdrawals in Q1. Even so, BofA expects BCRED redemption requests to rise to 12% in Q2 and believes withdrawal limits may follow.

👉 And here’s the most recent post on BCRED:

Meanwhile, Blue Owl is firmly in the hot seat. BofA forecasts Q2 redemption requests of 28.5% for OCIC and 52.9% for OTIC 😱, both sharply above already-elevated Q1 levels.

HPS’ HLEND is also expected to see an increase, with projected Q2 redemption requests of 13% versus 9.3% in Q1.

👉 If you are new here, here’s a primer on how liquidity in semi-liquid funds works:

📌 Leyla’s notes:

Non-accrual rates trending up, and dividend coverage below 1.0x are flashing red. If your BDC can’t cover its distribution from actual income, it’s returning your own capital.

Valuations are a big story: if we start seeing write-downs across the board, redemptions from non-traded semi-liquid vehicles will accelerate.

Finally, FSK reported a brutal Q1 2026:

NAV down 9.9% to $18.83

non-accruals jumping to 8.1% at cost

dividend coverage slipping to 0.6x).

A KKR affiliate came in with a $300M strategic backstop (a $150M convertible preferred piece plus a $150M tender at $11/share), in addition to an incentive fee waiver and a hard pivot to deleveraging. Octus published a great breakdown.

3️⃣ Commercial Real Estate

On Fundraising

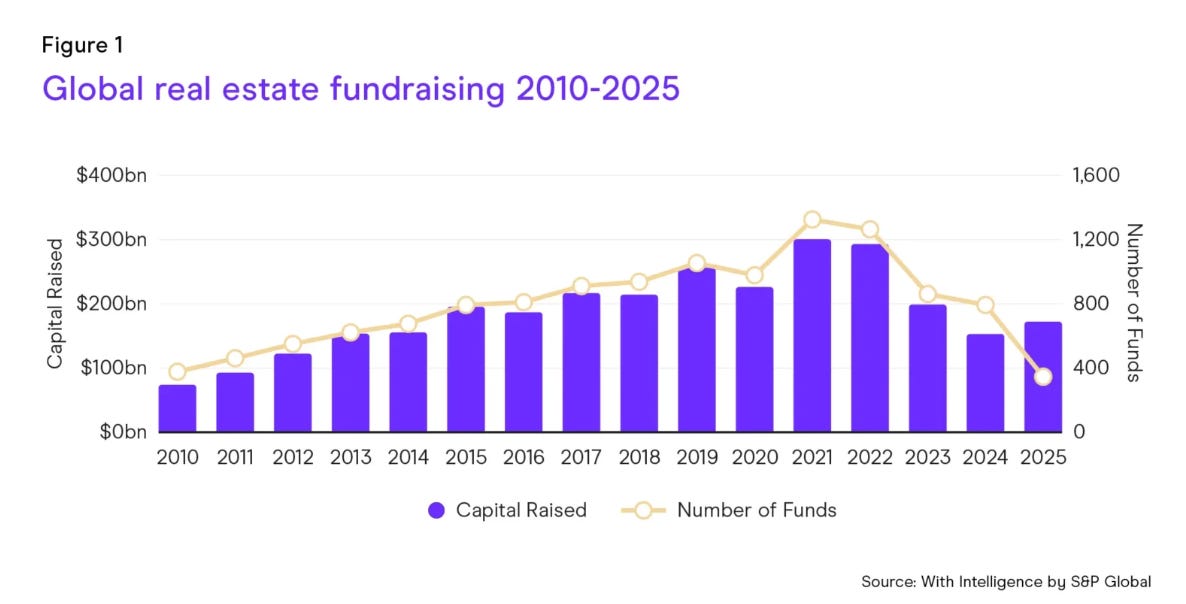

Private real estate fundraising rose 13% to $172 billion in 2025, the first year-over-year increase since 2021, driven primarily by opportunistic, value-add, and debt strategies capitalizing on falling asset prices and available debt:

But take a closer look at the right Y-axis. Total capital raised is recovering, but the number of funds doing the raising has collapsed. Capital is concentrating with larger fund managers. According to S&P’s With Intelligence, fundraising is unlikely to return to 2021-22 highs.

Speaking of mega-funds, BREIT raised $1.2B in Q1 (its highest quarterly raise in three years) and posted net inflows of roughly $1B. Sector-wide backlog of redemption requests has dropped to ~$1B (under 2% of total requests), but SREIT now accounts for nearly all of it.

We covered SREIT's situation in detail last week. Here’s what happens when you buy at the top of the market:

“Extend and Pretend” is Coming to an End

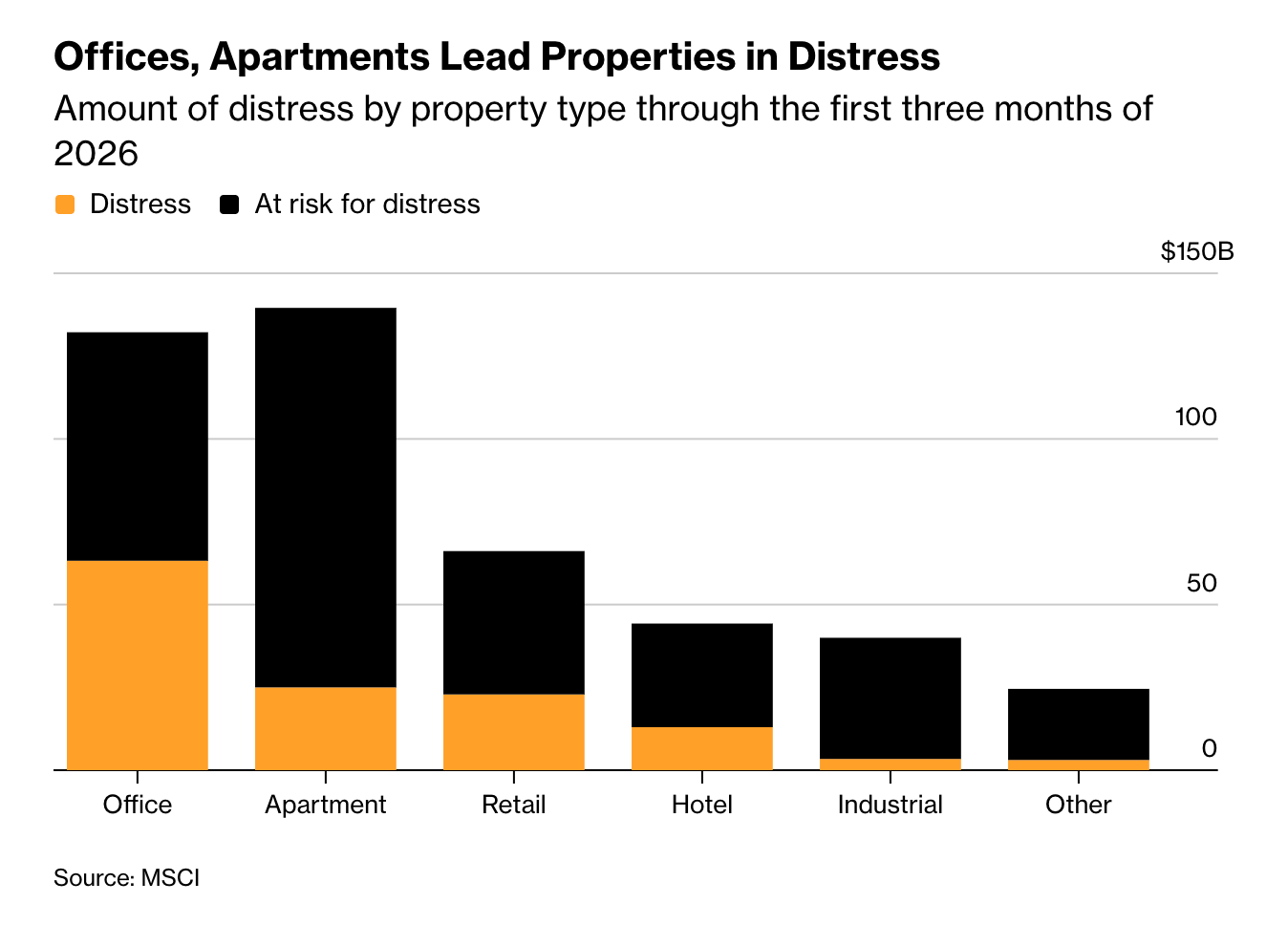

The "extend and pretend" era is officially over: Goldman, Deutsche Bank, and smaller lenders like Ready Capital are now selling distressed CRE loans at discounts as steep as 85% or foreclosing outright, with CMBS loans in foreclosure hitting $17B in March (up from $7B in 2024).

MSCI clocked $132B in total CRE distress, and Q1 marked the first quarter since 2022 where workouts exceeded new additions to the distressed pile. This means the backlog is finally getting worked through, mostly by lenders eating the loss rather than rolling the loan. We have reached the end of the road.

📌 Leyla’s notes:

The end of “extend and pretend” means we’re finally getting real price discovery. There will be some attractive buying opportunities for well-capitalized operators.

We are already seeing flight to quality: size and track record will matter. I've spoken with multiple GPs who were sitting on the sidelines in the first half of the decade. We might see them deploy meaningfully in the second half.

Question for the readers: are mortgage REITs already played out? Not something I’ve been watching closely of late, wondering if it’s worth taking another look?

Thanks for reading! As always, if you have any suggestions, reply to this email, leave a comment, or hit me up on socials (unhinged me on X, slightly more filtered me on LinkedIn)

-Leyla

P.S. New here?

Here’s where you’ll find the full archive (somewhat organized):

Hey Leyla,

I'd be interested to know your thoughts on publicly-traded BDC debt, particularly as it relates to large sponsors acting to backstop that debt, if in distress.

I took a deep look at FS KKR debentures when they gapped out prior to the junk downgrade this spring. My thought was that, while clearly bankruptcy remote from KKR the sponsor, that is would be a market-brand catastrophe for KKR to let the debt of the BDC go down. And thus KKR would step up to support. Which, of course, they recently did.

Bank regulators have made it very clear that this is a no-no for regulated bank (sponsors of CLO's CMBS, etc). But it's less of an issue in the private debt space.

And the fuzzy, imperfect, caveated conclusion to jump to, is that BDC debt has the implied guarantee of the sponsor, and shouldn't trade too wide of them.

Comments ?

Hey Leyla - interesting question on mortgage REITs.

One firm/fund that seems like it could be interesting to me is the Lending Fund run by DLP Capital which has a great 10+ year track record (absolute and relative). It’s all multifamily (so not as diversified as the public m-REITs though that has been alpha by avoidance for DLP with no office pain taken since COVID) but that’s one I’d be curious to get your view on if you ever get a chance.