Record Multiples; Bird Watching 🦉; and $77B in Hard Maturities

🗞️ Sunday digest: private markets insights 2/22

Happy Sunday.

Every other week, we send a quick digest on what’s catching our eye across private markets (the data, the drama, and the stuff LPs should actually care about).

Today’s lineup:

1️⃣ Private equity: record buyout multiples, surging continuation vehicles, and a steady push into 401(k)s

2️⃣ Private credit: good grief, where do I begin?? OBDC II eliminates redemptions just as semi-liquid credit vehicles boom (Defaults look contained, kind of)

3️⃣ Commercial real estate: the 2026 maturity tsunami looms, refinancing math is tight, but core funds are stabilizing… while capital still walks out the door.

Before we dive in:

Accredited Insight delivers the LP’s perspective on private credit, private equity, and CRE, drawing on hundreds of deals, and thousands of conversations. Paid subscribers gain access to our database of over 40 case studies and articles on everything from evergreen funds to due diligence.

1️⃣ Private Equity

TL;DR:

Buyout multiples are at record highs (margin for error is getting thinner)

Secondaries (especially continuation vehicles) are surging

Private equity is moving into your retirement account

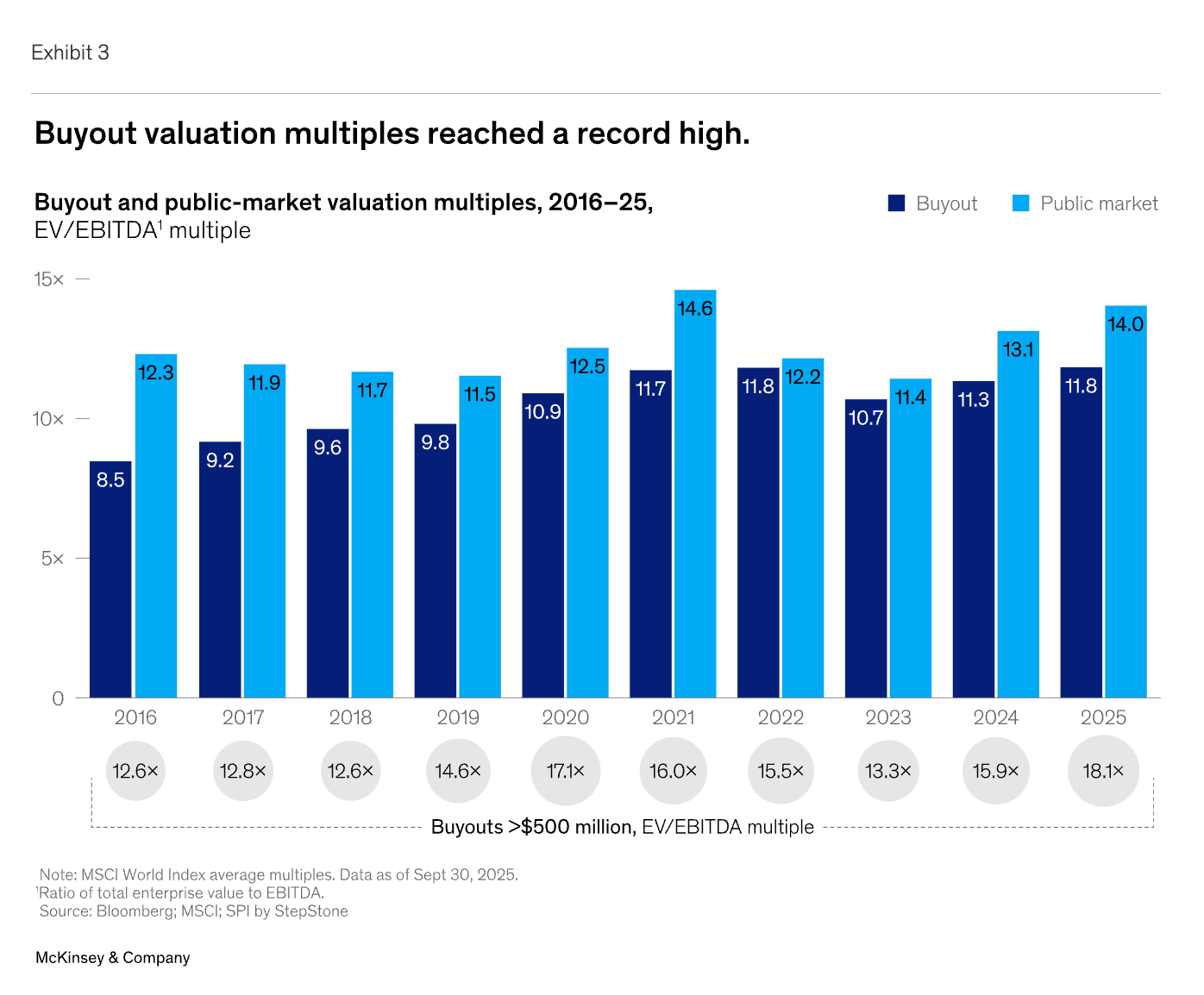

McKinsey & Company’s 2026 Global Private Equity Report

Buyout valuation multiples are at record highs. ❗️This is the single most important chart for anyone evaluating new PE commitments (am I dramatic enough?)

High entry prices = razor-thin margin for error. Sponsors need revenue growth, margin expansion, and cooperative exit multiples just to land in “acceptable returns” territory.

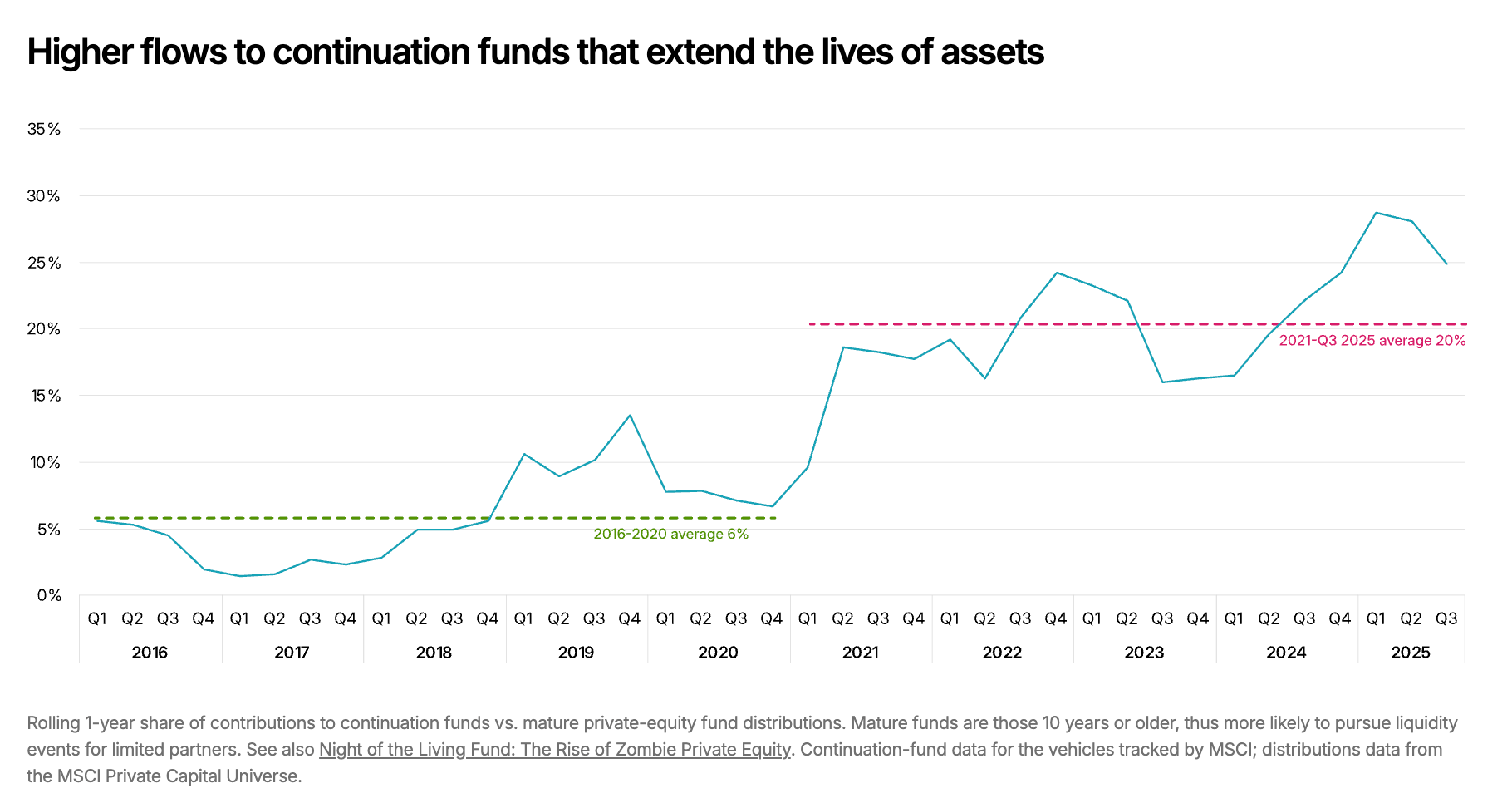

2. MSCI: Secondaries are on a Tear

And speaking of liquidity, in 2025, GP-led secondary volume hit $115 billion, with CVs accounting for roughly 43% of total secondary market volume.

❗️Nearly 75% of the largest global PE firms have now executed at least one continuation transaction.

None of this is inherently bad. But the pace and scale of CV activity is now large enough that it's starting to make its way to a variety of funds. If you're a secondaries investor, your exposure to CVs is growing whether you planned for it or not.

👉 Here’s your primer on CVs:

👉And here’s a fund with CVs on its books:

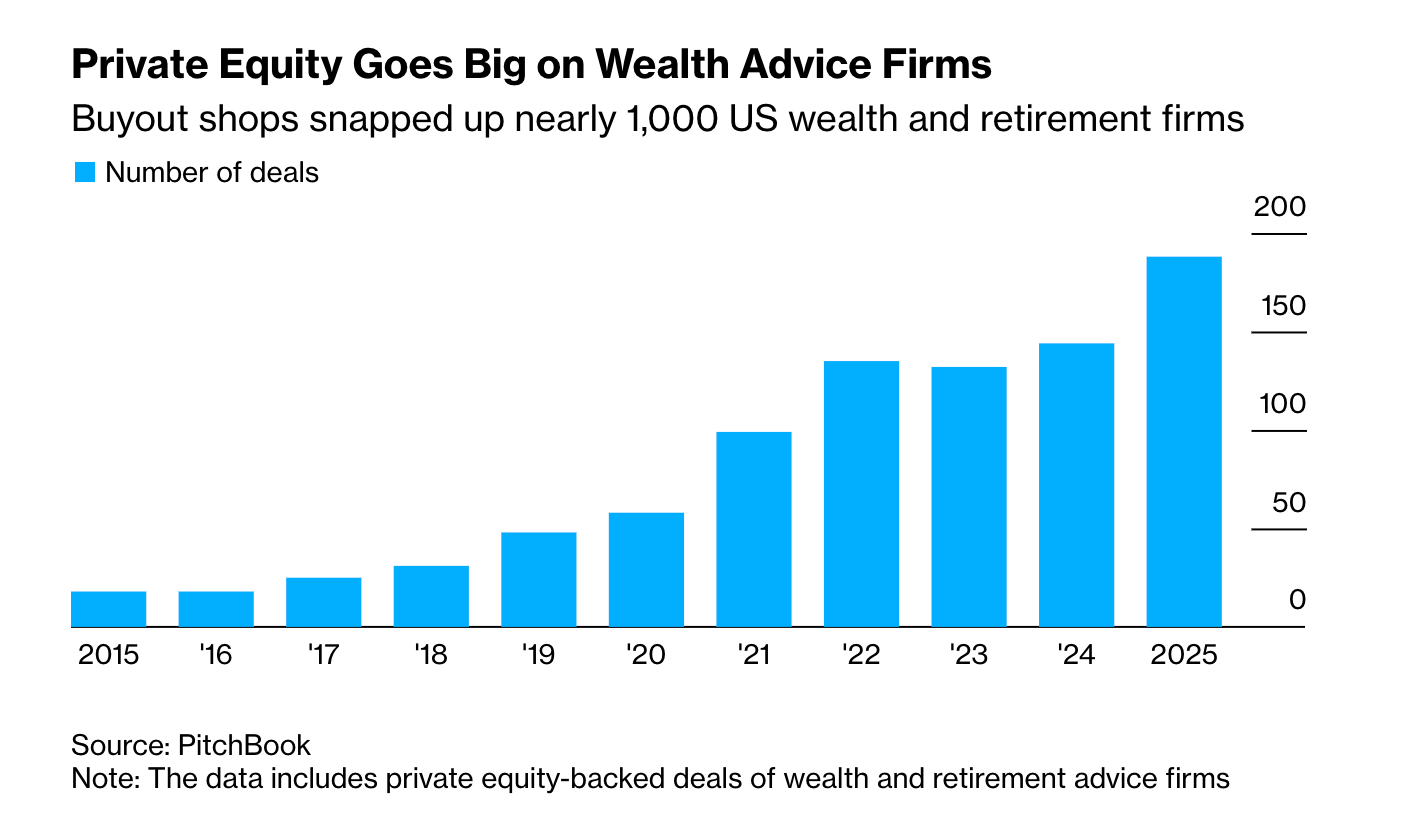

3. PE Is Coming for Your 401(k)

The battle for your retirement dollars is heating up.

Bloomberg reported this week that PE firms have acquired more than 900 independent financial advisory firms over the past decade:

Then in August 2025, Donald Trump signed an executive order directing the DOL, SEC, and Treasury to ease restrictions on alternative assets in retirement plans.

Asset managers are not sitting on their hands. According to EY, 90% of GPs are at least “somewhat interested” in developing defined contribution products, and 24% are already designing offerings.

👉 Thinking about PE exposure? Start here

2️⃣ Private Credit

TL;DR:

OBDC II eliminated redemptions (semi-liquid met real stress)

Defaults look contained, but PIK, LMEs, and 2026 maturities tell a more complex story

Semi-liquids are on a tear

1. Blue Owl’s OBDC II: The Saga Continues

On February 18, Blue Owl announced it had sold $1.4 billion of direct lending loans across three of its BDCs to four North American pension and insurance buyers — at 99.7% of par.

OBDC II’s share: $600 million, roughly 34% of the fund’s portfolio.

👉 If you missed the deep dive, read that first. We walk through what remains in the portfolio, estimate which assets were sold, and get into the mechanics of how return of capital will actually work.

Now the kicker:

OBDC II is permanently replacing its quarterly tender offers with return-of-capital distributions.

Translation: investors can no longer request redemptions. Instead, everyone receives pro-rata distributions as the fund winds down.

This comes just three months after the failed merger with publicly traded OBDC:

OWL stock dropped ~10% on the news. Mohamed El-Erian asked publicly whether this was a "canary in the coalmine" moment. Blue Owl responded that they were "accelerating the return of capital, not halting redemptions." Technically, accurate, but not the same thing to investors…

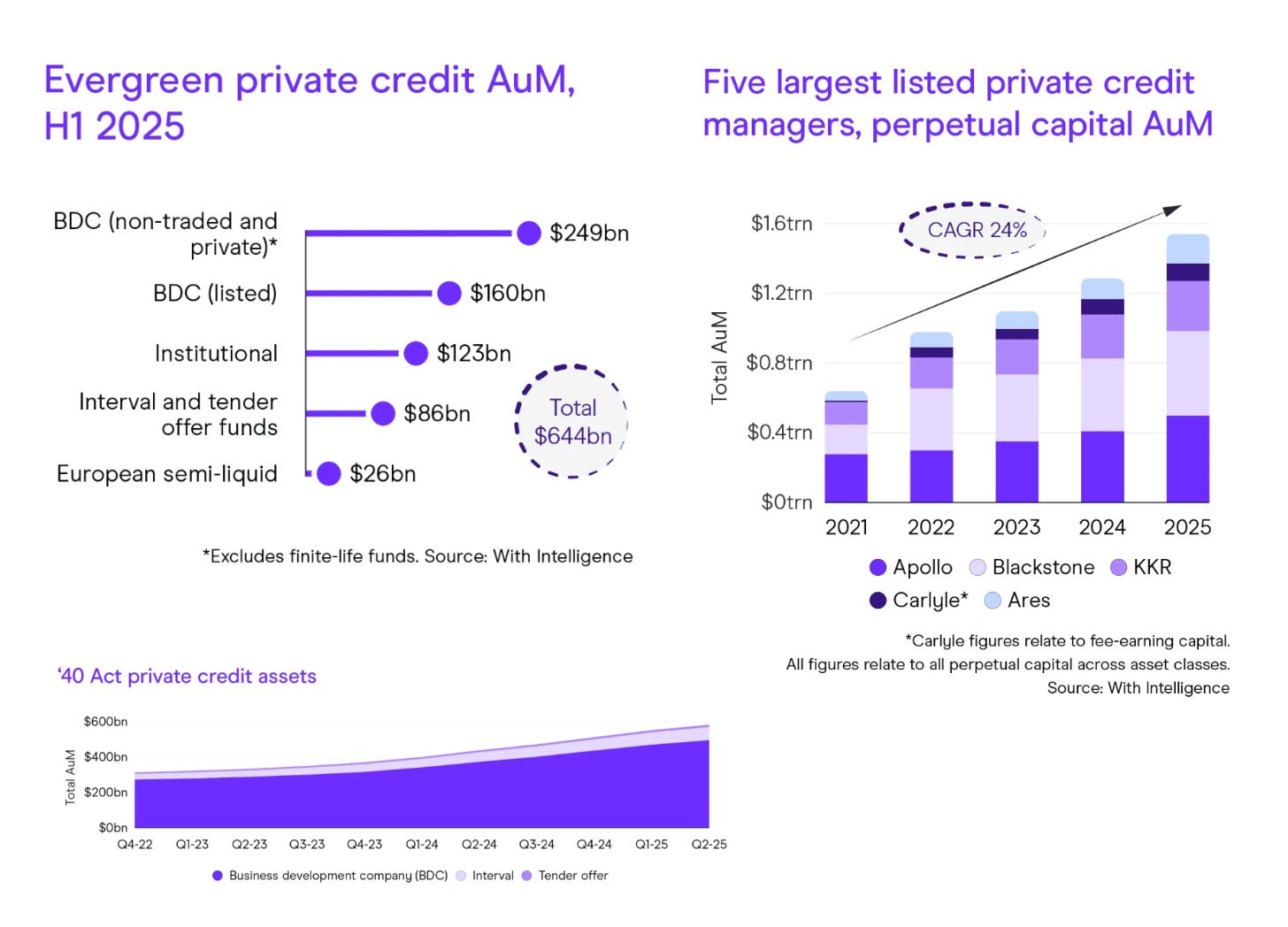

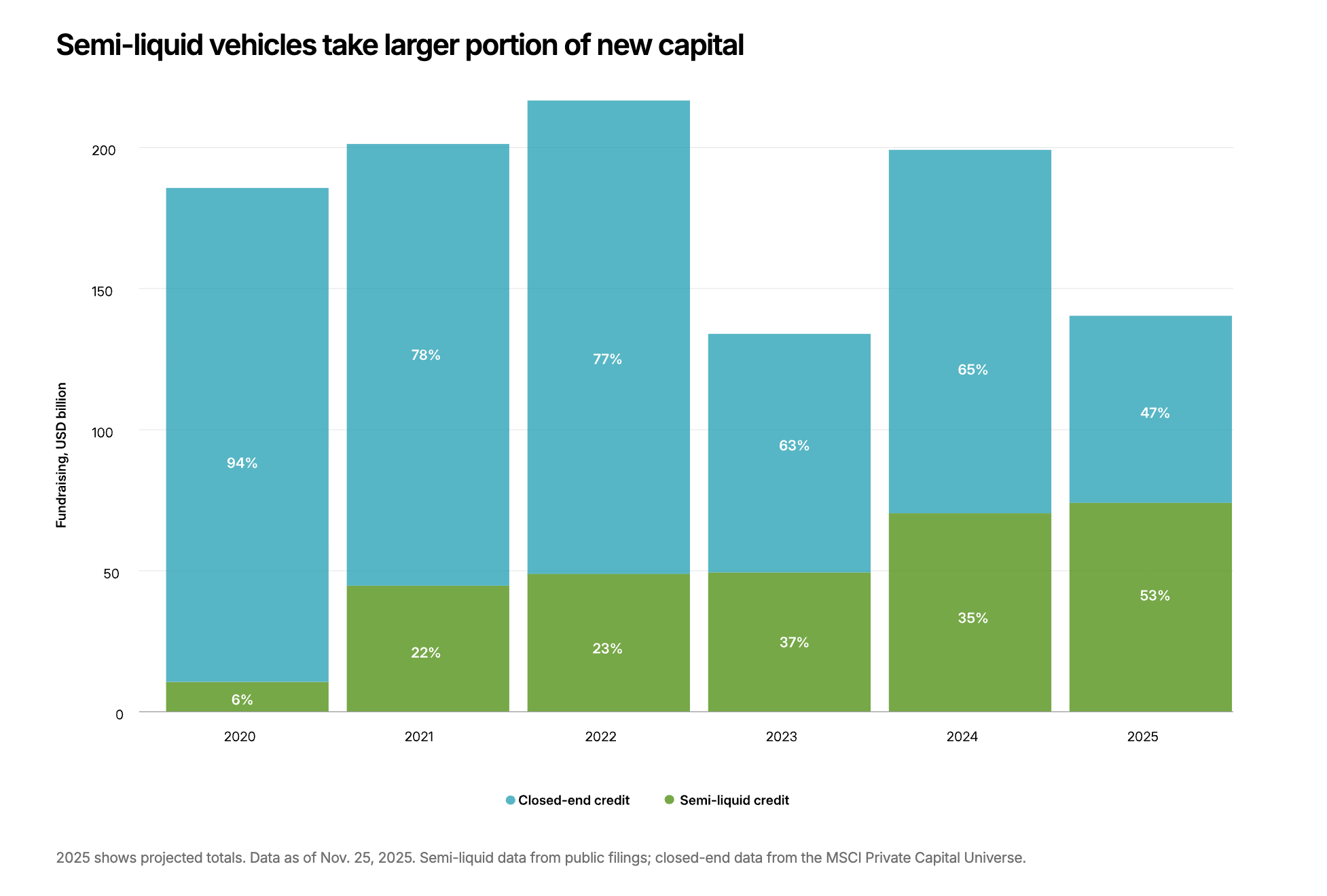

2. Private Credit’s First Big Test: The Numbers Behind the Boom

S&P’s Within Intelligence published its 2026 private credit outlook, and the charts tell the whole story:

Semi-liquid private credit vehicles are capturing a larger share of new capital flowing into private markets. (Old news for long-time readers, but our subscriber base is up 43% in 90 days, so worth repeating for the recently arrived)

Here’s your primer on evergreen vehicles:

The earlier-mentioned MSCI report showed the same thing: look at the fund mix. The growth is concentrated in semi-liquid structures:

The appeal is obvious: lower minimums, simplified access, the promise of periodic liquidity. But let me remind you: the liquidity feature is wrapped around fundamentally illiquid loans.

When markets are calm and fundraising is smooth, gates stay open. When things go sideways - well, see the OBDC II story above.

A few data points from the report and elsewhere:

The headline default rate in private credit has stayed below 2%. But once you include selective defaults and liability management exercises, the “true” default rate approaches 5%.

Public BDCs now receive an average of 8% of investment income via PIK 👀

23 of 32 rated BDCs have unsecured debt maturing in 2026, totaling $12.7 billion — a 73% increase over 2025.

Record credit secondaries fundraising in the first 3 quarters of 2025: $16 billion, including $5 billion+ raises from Coller Capital and Pantheon Ventures.

Speaking of the Coller fund, here’s the deep dive on it:

👉 New here? Want to learn more about private credit secondaries? Read this:

🐥 None of this means the sky is falling, btw. But the evergreen structure is new, and has not really been tested. OBDC II is the first high-profile case where the semi-liquid model met real redemption pressure in private credit. It probably won't be the last.

👉 In the real estate world, we had a well documented case with BlueRock:

👉 Invest in private credit? Here’s how you can learn to read the statements:

3️⃣ Commercial Real Estate

1. The Maturity Wall Isn’t a Wall Anymore (it’s a tunnel, with no light at the end just yet)

You’ve heard about the CRE maturity wall (are you sick of it yet?) Here’s where it actually stands.

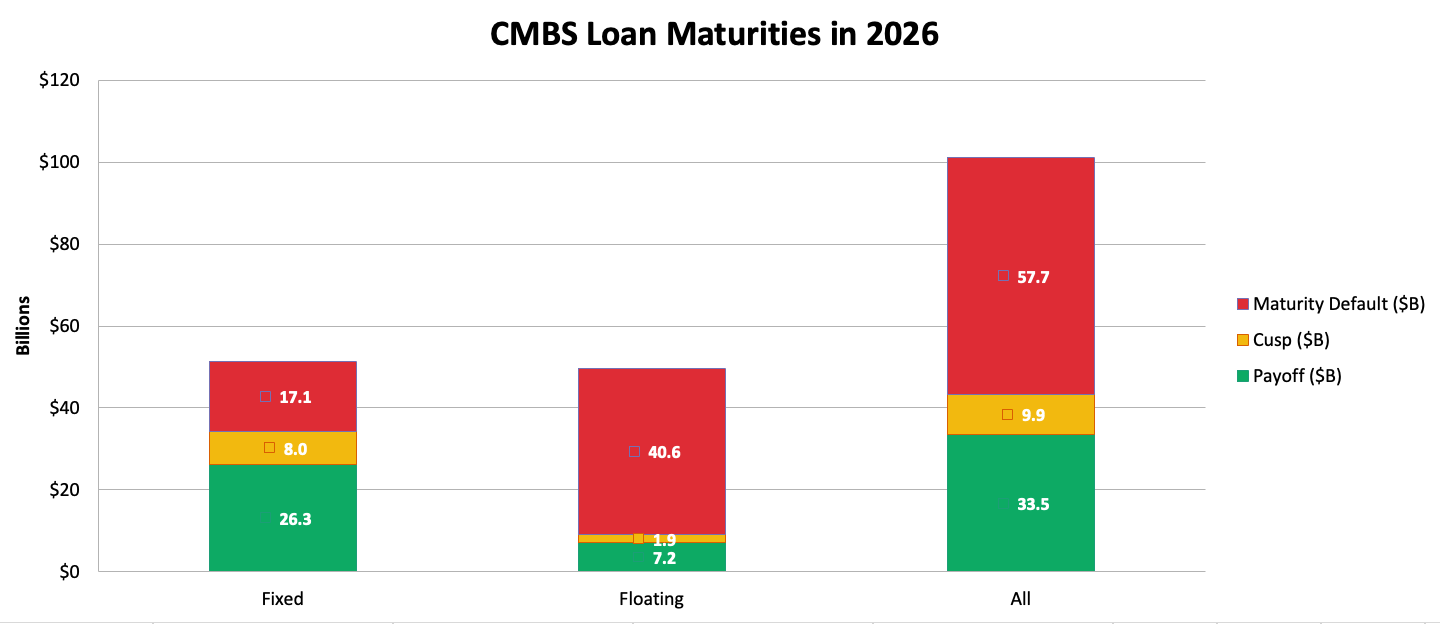

$76.6 billion in CMBS loans are hitting hard maturity in 2026 (Trepp). These are loans where borrowers have already used up all extension options.

The broader picture: Morningstar estimates over $100 billion in total CMBS maturities in 2026, with roughly $57.7 billion likely to default at maturity.

Why? The math doesn’t pencil.

The average rate on new CRE loans is 6.24%, vs 4.76% on the maturing debt. A property that was financed at 65% LTV five years ago may now appraise for 20–30% less, meaning new loan proceeds don’t cover the old balance. The gap has to come from somewhere (like fresh equity, mezz, or a discounted payoff).

👉 CRE investing 101: the relationship between cap rate and pricing:

By sector:

Lodging now edges out office as the largest share of hard maturities at 20.5% (office: 20.1%).

Office remains the deepest hole. Values have dropped 55.8% since issuance on CMBS-appraised properties. Among office loans that matured before 2026 and are still outstanding: 83.7% are delinquent and 92.7% are in special servicing (CoStar).

Multifamily maturities surge 56% to $162.1 billion in 2026. But the distress here is vintage-specific: two-thirds of apartment foreclosures in H1 2025 involved 2021–2022 vintage loans with aggressive leverage.

2. NCREIF ODCE: Returns Up, But Capital Still Walking Out

Some green shoots in the institutional core real estate data.

The NFI-ODCE (the benchmark for open-end diversified core equity funds) posted a 3.54% gross total return for the year ended June 30, 2025: its best annual performance since Q4 2022.

Income return: 4.15%

Appreciation: -0.59%

In other words: you’re getting paid to hold, but values aren’t rising yet.

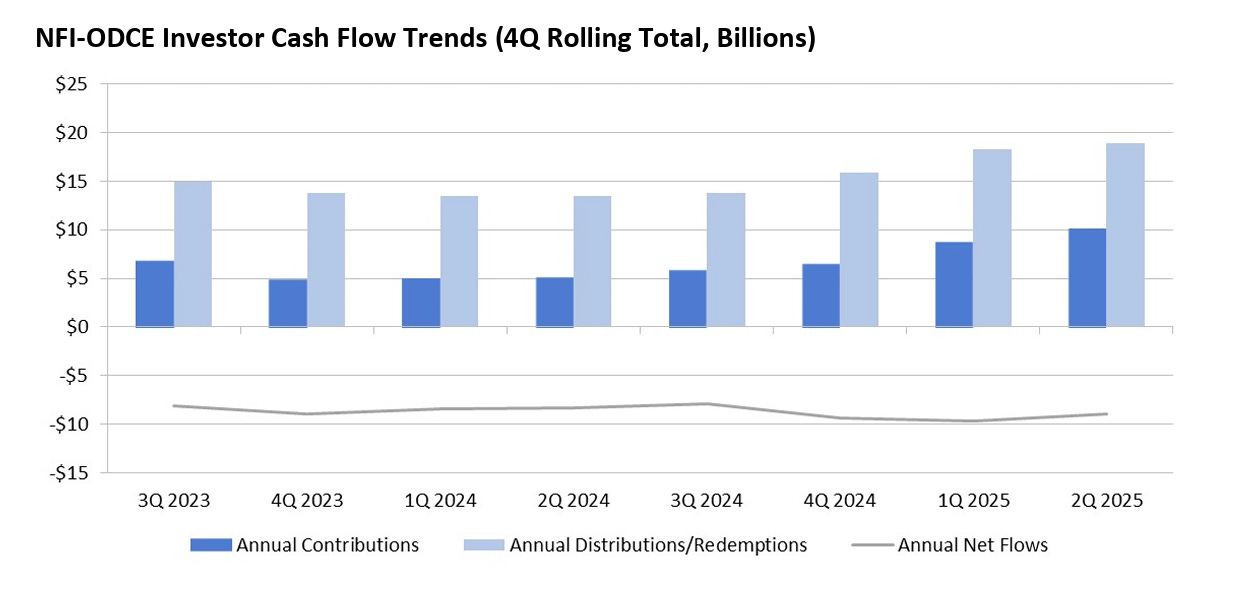

➡️ Now the capital flows:

Net investor cash flows remain negative: -$1.7 billion in Q2 2025, roughly flat quarter-over-quarter.

Over the trailing year:

Contributions: $10.0B

Distributions + redemptions: $19.0B

Net outflow: $9.0B

The good news? The bleeding is slowing. Contributions are up 93.8% year-over-year. Redemption queues, which peaked at ~$41 billion in Q1 2024, have fallen to roughly $25 billion.

(Just in time for new redemption queues in private credit… am I right?)

On this bright note, I’ll sign off. Have a great week!

P.S. New here?

Check out some of our popular topics to get started: on private credit, private equity, and commercial real estate.

Thanks for reading! As always, if you have any suggestions, reply to this email, leave a comment, or find me on socials (unhinged me on X and a more tame me on LinkedIn)

-Leyla

P.P.S. If you made it this far (and missed this meme earlier), enjoy:

Leyla, I think you are too nice to OWL, with "Blue Owl responded that they were 'accelerating the return of capital, not halting redemptions.'" In this context a redemption is an investor-initiated event and they are stopping that. Yes they are initiating distributions, which investors may like. But to my eyes they are telling half truths.